Subscribe to 0slippage

Receive the latest updates directly to your inbox.

Service Denial, Order Bombing, & The Living Dead: TWAMM Arb Oddities

A theoretical attack on Time-Weighted Average Market Maker (TWAMM) pools is introduced and empirically shown to be of negligible concern to arbitrageurs herein. The effect is mitigated further in practice by the practical settings of a TWAMM pool’s order interval, be it block or time based, collating order expiries at fixed intervals for increased gas efficiencies. Additionally, it is shown that in implementation, the attack is largely circumvented by the Ethereum Virtual Machine’s accounting of gas use for SSTORE operations related to the attack.

Great Artists Steal. And Optimize: TWAMM Gas 💰⬇️

Previous articles in this series focused on Time-Weighted Average Market Maker (TWAMM) gas usage relating to operational parameters \[1] and an efficient algorithmic approximation \[2].

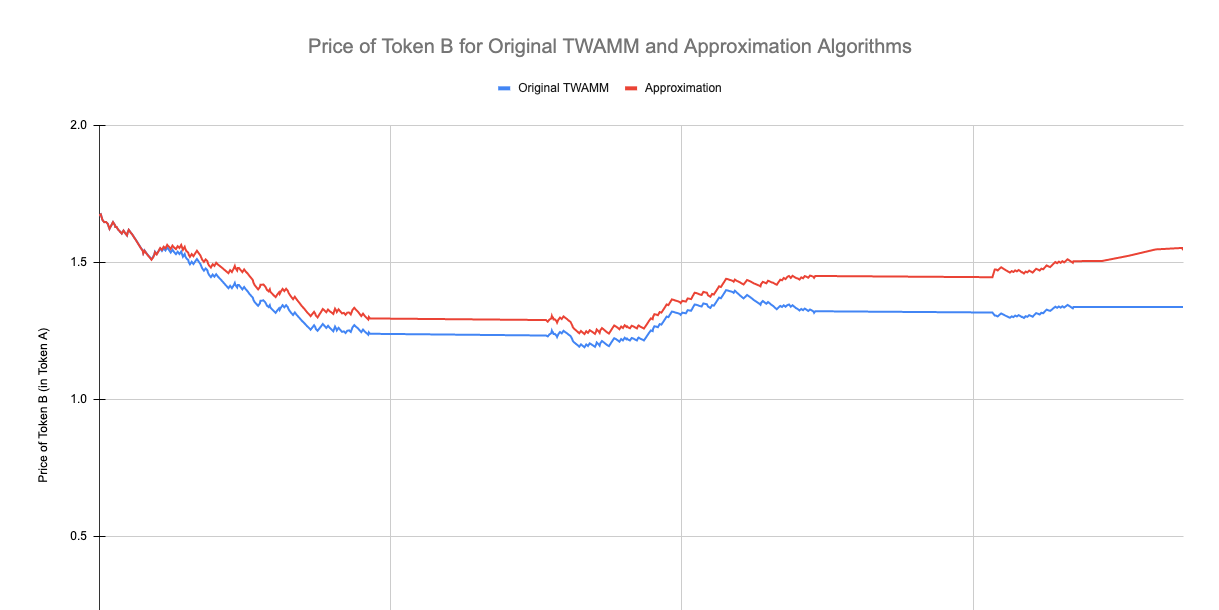

TWAMM Algorithm Optimization & Approximation Analysis

Unfortunately a measurement error methodology was discovered for the non-isolating gas measurement in this article (approval and transfer figures were mixed in with contract function data). Please refer only to the isolating methodology measurements in this article. For more information consult Appendix A of the article Great Artists Steal. And Optimize: TWAMM Gas 💰⬇️, which addresses the issue and presents an improved methodology. The incorrect data is labelled “Ignore, consult update 5/7/2022” below.

Time Weighted Average Market Maker Operational Parameters vs. Gas Usage Analysis

Time-Weighted Average Market Makers \[1] (TWAMM) uniquely enable large trades by distributing them in time, potentially freeing market participants from slippage woes of the Constant Product Automated Market Maker (CPAMM) bonding curve. TWAMMs also simultaneously provide benefits to other market makers, like arbitrageurs in a unique symbiotic relationship.