Lately, DeFi 1.0 tokens have been jeered and scoffed at by the community. With most assets having a lower beta compared to other categories, and a never ending bleed against ETH, the complaints are understandable.

While this could be attributed to the overall macro weakness in the market, there may be other factors that play a part into this.

Reasons:

New methods of getting higher beta

With the explosion of popularity for NFTs in 2021, investors found new methods of generating returns against ETH. NFTs gave a new avenue for investors to speculate their ETH, and was able to attract a much wider audience due to the simplicity and more entertaining aspect over DeFi.

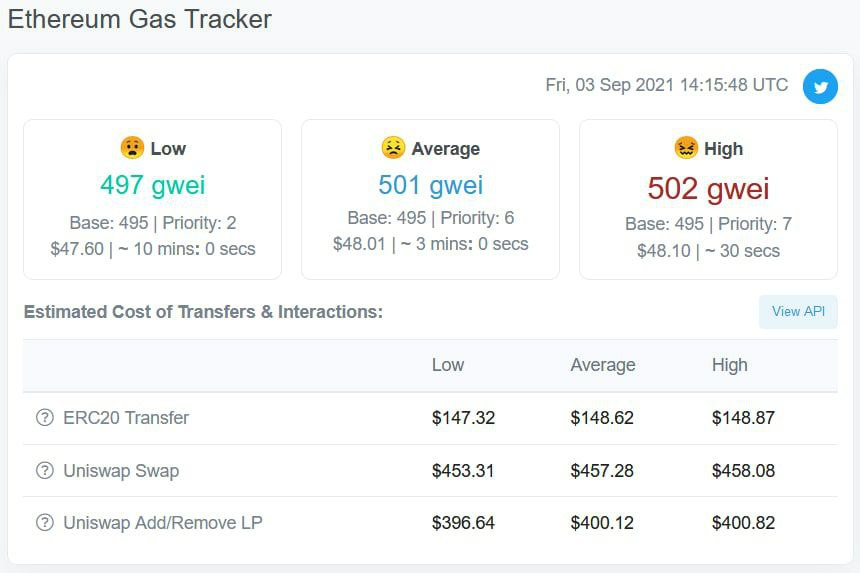

High gas fees:

Ethereum gas fees were consistently high the whole of 2021. Everyday came a new NFT mint, where hundreds of bots tried to snipe mint by directly interacting with the contracts. This usually caused the ETH network to be congested, which directly affected DeFi users. Swapping tokens or reorganizing positions took hundreds of dollars which could not be sustained.

A Diversion of Liquidity:

Liquidity is never loyal in DeFi. In a space where moving capital takes mere seconds, billions of TVL come as easy as they go.

Due to the high gas fees on Ethereum mainnet, most investors who cannot stomach 3 digit transaction fees flew to alternative ecosystems. Many forks of protocols like Aave and Yearn sprung up on chains like Polygon and Fantom, with increased yield to attract earlier users to deposit liquidity into their project instead.

Regulatory concerns:

In my opinion, regulatory concerns are one of the more serious issues hindering DeFi’s future. Due to the regulatory concerns, it is almost impossible for DeFi protocols to share fee revenue with token holders without being considered a security in the United States. I list a few examples of the increasing pressure against DeFi protocols below.

The Road Back Up:

Tokenomics Revamp:

While price action has been disappointing, delving deeper into governance forums and discord calls gives a better understanding to what developers have been trying to do to help counteract this.

Balancer (BAL) recently released veBAL which is modeled against the successful veCRV tokenomics, which will help reduce selling pressure as holders are incentivized to lock their tokens.

Yearn Finance (YFI) and Perpetual Protocol (PERP) have also announced their venture into ve-tokenomics, with veYFI and vePERP coming soon.

While this may not be the perfect answer in reviving price action, I think this is the right step towards better tokenomics.

A shift in market narrative:

Sometimes, less noise means more. In 2021, more than 2 billion dollars were lost due to DeFi exploits. When managing billions in TVL, the Lindy Effect may come into play as more investors start to realize that DeFi 1.0 protocols are safe to deposit their money into. I am also of the belief that market cycles have a hand in the current price action, and that we are in the accumulation phase right now.

Building never stops:

Unlike ICOs in 2018 which were P&D schemes, defi developers are still continually working behind the scenes at making the future of finance better.

Warchests have also been accumulated by protocols over the last year, either by increasing their Convex holdings to participate in the Curve Wars, or other non native assets to tide over ‘bear markets’. As market conditions improve and metrics like TVL/Mcap and P/E P/S ratios gain more significance, we might see a revival of prices soon.

I hope this gave a brief high level overview of what has impacted the DeFi markets over the last year. I think it would be cool to look back in the future on some of these issues and how we overcome them.