TL;DR All of crypto is accepting and suffering from an association with toxic financial speculation, but not all of crypto needs to be.

Crypto has birthed the latest reincarnation of populist speculation, following tulip mania, the South Sea bubble, and bucket shops among others. Glancing backward in time, the pattern seems to be:

- new financial tools bring speculation to a mass market →

- massive popularity as an opportunity for easy money →

- series of volatile market swings and brutal fraud cases →

- moral uproar and new regulation, re-limiting speculation to the privileged.

Crypto is already at the last step: moral uproar over crypto is flooding the internet. Regulators are coming, though the decentralized nature of blockchains presents them with a unique challenge.

Some of the so-called web3 movement is about fighting the battle for populist speculation. Maybe that’s a battle worth fighting, and maybe not—again, look to history, or maybe to Devil Take The Hindmost and Speculative Communities (both of which I’ve only read some of).

A huge portion of the crypto design space, though—coops, art, mutual aid, crowdfunding, grants, international payments, and more—doesn’t require speculation and so suffers its downsides needlessly. We, people working in these areas, shouldn’t take this lying down. We should consciously limit or remove speculation from our systems whenever possible, and we should make sure the world knows it. This blog proposes some steps towards doing that.

What’s speculation?

I’m sure you can find a million definitions of financial speculation, but here’s what I mean in this piece:

Speculation is buying or selling something based on its perceived future value, rather than its perceived present value.

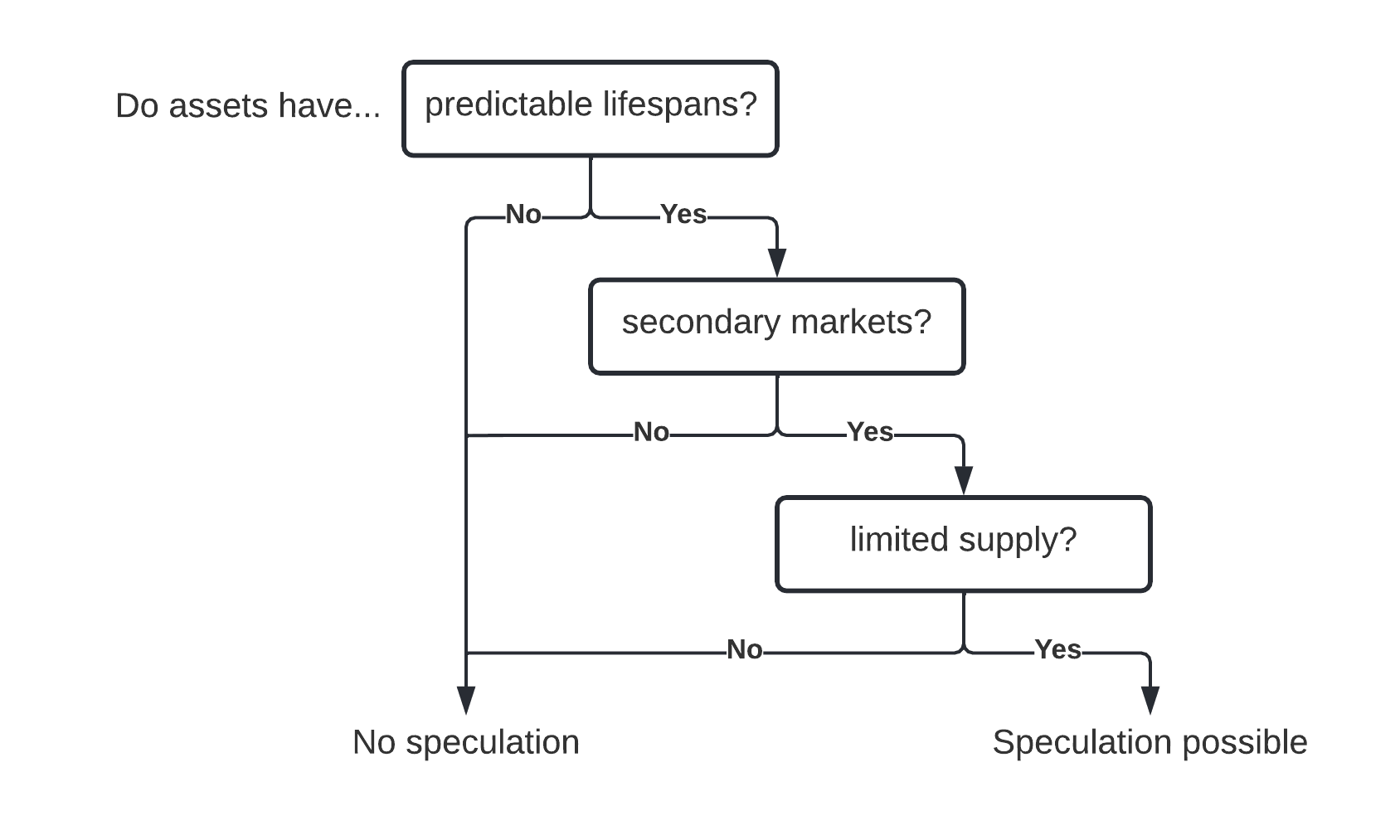

An asset can be speculated on if it has:

- A predictable lifespan — it’s easy to predict how long it will exist or “stay fresh.” The more predictable the lifespan, the easier speculation is.

- Secondary markets — it can be bought and sold readily and repeatedly. The larger and more available secondary markets are, the easier speculation is.

- Limited supply — there is some limitation on the circulating supply of the asset, like a limited addition set of 100 or a limited time window of availability, like a fashion pop up. The more limited the supply, the easier speculation is.

The creator of an asset can profit from speculation if:

- They sell the asset based on its speculative value (e.g. a securities offering)

- They receive a royalty based on secondary sales of the asset

- They retain a large supply of the asset, which they can sell later if the price appreciates

Speculation on an asset can also be encouraged if the asset is concretely connected to future growth, i.e. it grants governance rights or profit-sharing in a project.

Why speculation is good

It’s a powerful fund-raising tool

Without speculation, people fund things because they value their utility: I contribute to a graphic novel Kickstarter only because I want the graphic novel.

With speculation, people fund things for both utility AND financial upside: I invest in a publishing company because I want to see certain books published and because I will gain financially if the publisher succeeds.

The unreasonable effectiveness of speculation as a fund-raising tool is perhaps the main reason speculation is so popular in crypto (and crypto’s questionably legal lowering of the barrier to it may be the main reason crypto is popular at all).

It allocates capital efficiently

Speculation creates an incentive to invest in things that will succeed: things that will create lots of good for society in the future. Speculators have a financial interest in discovering and accelerating such projects, and so, in theory, speculation leads to more good things created more quickly.

It’s a powerful wealth-building tool that should be available to all

This one is arguable. Many people become wealthy speculating, but lots lose money, too.

It’s possible this point has become more relevant today, because of the internet and other new technologies globalizing markets while lowering barriers to entry. If, in today’s environment, odds of a new venture’s success are lower than ever—but successful ventures are more profitable—then speculation is more important than ever, and it should not be restricted to the already wealthy.

Why speculation is bad

It compromise values

Adding speculation into a system creates a powerful extrinsic incentive that can override intrinsic incentives.

In other words, start with a community that cares about art or stories or games, add a speculative asset representing membership in that community, and suddenly people start caring about the market price of the asset. They may start viewing everything the community does in terms of its effect on the price of membership. Too much of that and the essence of the community is destroyed. So:

- Artistic community + speculation = Profit-seeking community

Similarly, speculation can corrupt social curation and recommendation:

- People can’t speculate on things they like = People promote things because they like them = good, honest recommendations

- People can speculate on things they like = People promote things because of their own financial interest in them = bad, dishonest recommendations

It enables fraud

In a non-speculative venture, the steps to success are generally:

- Invent crazy idea

- Actually do the idea

- People pay for it: profit

Speculation, cynically, lets you skip step 2:

- Invent crazy idea

- People speculate on it: profit

And indeed, we see way too many crypto projects doing just this. Building the idea is how businesses are supposed to do good for society. Skip that step and you have at best a waste of time and money, at worst an outright pre-meditated fraud.

It encourages degenerate spending

Speculation adds an extra reason to buy things — it’s a little like adding a free lottery ticket into every purchase. If you liked golf already, how can you resist buying new clubs when you’ll get to play with them AND there’s a chance you could resell them in a few years for 10x returns? It’s very easy to convince yourself to make that purchase, and much of the moral outrage surrounding populist speculation revolves around speculation as anti-social gambling, enticing people to spend irresponsibly.

When bubbles pop, sure there are a few Ivar Kreugers, but there are a lot more Jane Doe’s that lose their retirement savings because they, or their pensions, fell for this trap.

Controlling speculation in systems design

To design a system with little or no speculation, simply don’t do all the things from the definition above.

Use assets that have at least one of:

- Unpredictable lifespans: it’s hard to speculate if you don’t know when an asset will disappear.

- No secondary sales: if you can’t sell it, you can’t speculate on it.

- Unlimited supply: if I can always buy another identical golf club for $100, resold golf clubs will probably never go for more.

Have no skin in the speculation game:

- Don’t promise future value: sell things based only on what they are today, not on what they might be tomorrow.

- Don’t retain any assets that may be speculated on

- Take no royalties on secondary asset sales

Do not encourage speculation by connecting an asset’s value to future growth, such as by granting governance power or profit-sharing rights to asset holders.

These design principles are all gradients: secondary markets vary widely in who can access them and their liquidity; asset lifespans can be more or less unpredictable; more or fewer assets can be retained by creators; and so on. Despite that complexity, I think this is a decent checklist to help systems designers think comprehensively about speculation.

Example Systems

Highly speculative:

- Limited supply NFT where creator takes royalties, keeps some initial supply, and promises future collaborations with high profile celebrities (speculative assets, creator gains from speculation, and speculation is encouraged by promising future collaborations)

- Standard ERC20 governance token for a DeFi protocol, where the initial team gets a large pre-allocation of the token (speculative assets, creators gain from speculation, and speculation is encouraged by connecting the tokens value to the growth of the protocol)

Limited speculation:

- Limited supply NFT with free minting where creator retains some initial supply but takes no royalties and promises no roadmap (speculative assets, creators games some from speculation, no extra encouragement via roadmap)

- A governance token that is sold in an AMM crowdfund (meaning no upper limit for funds raised) but is non-transferable (initial speculation during crowdfund, after which assets are not speculative)

- Juicebox project with a >0% discount rate (discount rate means later funders get fewer tokens, so even though Juicebox project tokens only grant a kind of “refund” right, with a >0% discount rate, early funders can get a >100% “refund” if many people fund after them — the asset becomes speculative)

Little to no speculation:

- NFT that gets randomly burned on transfer and can be minted in unlimited supply for a immutable price (non-speculative assets)

- Non-transferable reputation ERC20 that can be minted only by group vote and is never sold (non-speculative assets)

- Juicebox project with no revenue model and a 0% discount rate (with a 0% discount rate, Juicebox tokens can at most give a funder their contributions back 1:1)

Recommendations

It seems likely that regulation will eventually change the speculative landscape of crypto soon enough: it has often happened that way. But in the mean time:

In my humble opinion, crypto builders should:

- Make a conscious choice around the level of speculation you want in your system, and design around speculation methodically, using thinking like the framework in this post.

- Explain the role of speculation in your project in your marketing, especially if you are limiting or eliminating speculation.

Sometimes, we all want to do something that’s just for fun or just about art and isn’t about making money. Designing speculation out of projects that don’t need it and communicating that will help people find their fun and avoid fraud. It’s good for the space.

For everyone else: before you use a crypto product, first try to understand the role speculation plays in it, using this framework or another. Crypto, for better or worse is pretty radically transparent: if you don’t like what speculation does to projects, you should be able to avoid it.

P.S. To make this stuff more pro-user, we could even consider creating a third party certification body or DAO that evaluates the level of speculation in a project’s token designs and gives it a rating for “speculatability.”