*Chinese Version:

*The article was written on Dec.31, 2021, and the data is as of Dec.31, 2021.

The history of DEX — ride the waves of the DeFi

They say that 2021 was the golden age of the crypto world.

In 2021, Bitcoin and Ethereum repeatedly set new highs, and the total market value of cryptocurrencies once reached three trillion dollars. The primary market boomed, mainstream capital entered, the Bitcoin futures ETF became a reality, and Bitcoin became legal tender in El Salvador. The carnival of Meme coin, the booming of GameFi, the success of DAO, everything can be NFT, the rise of the new public chain ecology, and DeFi came to 2.0. Players inside and outside the industry have always contested Metaverse and Web3.

Things come and go, but Crypto is never short of good stories. The Inclusive Finance ideals that DeFi points to continue to energize the industry. Decentralized exchange (DEX), one of the most important infrastructures, is still the focus. Before describing the future of DEX, let’s look at how DEX has evolved throughout history.

The original DEX dates back to 2014, when Counterparty protocol, a token crowdfunding platform based on the Bitcoin blockchain, was founded. It was possible to successfully ditch the traditional sports betting platform and use Counterparty to place exciting bets on the FIFA Football World Cup Brazil outcome. The innovative Counterparty DEX was even more exciting. All Counterparty tokens were tradable on DEX, a Bitcoin-based network. However, due to the small market environment and ecosystem, Counterparty DEX did not attract significant attention and gradually faded out.

The ICO (Initial Coin Offering) market was chaotic in 2017, but these things would eventually pass. When the bubble of ICO burst, DEX became a popular choice for Ethereum token holders to convert digital assets. But IDEX was the only DEX back then. The first-generation Ethereum DEX, which in part mimicked the Counterparty model on Ethereum, had less than $5 million in annual transactions. In the same year, Vitalik wrote a post about running an up-chain centralized exchange (CEX) in the same way as a predictive market (Uniswap is the story). Five years later, Vitalik is still “proud” of the proposal to build the curves x times y equals k.

Then, in August 2018, Bancor emerged out of nowhere. In a blog post, Bancor mentioned the idea of building an automated market maker that would revolutionize the order-book-style trading market by pairing all tokens with BNT, a practice that continues today. Although Bancor was a pioneer in using the AMM model, its relatively low trading volume affected the income of liquidity providers, and its attraction ability was weak. Low liquidity caused a bigger slippage, and users were less willing to trade on its platform, which was a vicious cycle for a long time.

Uniswap went live in November 2018, but it did not surpass Bancor officially in trading volume until February 2019. The design of Uniswap was more efficient and user-friendly, though both DEX utilizes a 50–50 reserve model. More than that, Uniswap was also designed to support licensure-free crypto assets, giving it great composability with the larger DeFi ecosystem.

The total trading volume of DEX exploded to $2.7 billion in 2018. The transaction volume of DEX shrank slightly in 2019 but exceeded $2.5 billion.

In the first half of 2020, Aave, Curve, Balancer, and Uniswap V2 launched successively. In June, Compound started liquidity mining, and it combined borrowing with DEX. DeFi users began earning rewards for borrowing money on Compound with additional incentives in the form of COMP tokens led to a sharp increase in the supply and borrowing APY(Annual Percentage Yield) of different tokens. It opened the DeFi Summer chapter; Ampleforth followed a market cap of $688 million as the first Rebase token. In July, Yearn Finance went online, Andre Cronje distributed governance token YFI to the Yearn community, which was fully distributed through liquidity mining. This model won strong support from the DeFi community, and the fund locked into the incentive liquidity pool was worth more than $600 million. In August, CRV Token emerged, and Curve, which focused on stablecoin trading, ushered in a significant turning point. Curve War started from then, but at this stage, Yearn still dominated for “the return rate of Yearn Vault.” That same month, SushiSwap forestalled before Uniswap launched its tokens. After SushiSwap’s lead developer ChefNomi sold all his SUSHI tokens to incentivize Uniswap’s liquidity providers, SushiSwap attracted liquidity of up to $1 billion, which forced the Uniswap team to react. The Uniswap team airdropped the UNI token on September 16. DeFi users benefited early from the liquidity battle, and the total market value of the DeFi project soared. In addition to the high-value retroactive airdrop incentive, Uniswap initiated a liquidity mining program in four different liquidity pools and attracted over 2 billion dollars in liquidity, most of which was recovered from SushiSwap.

Since then, one of them moved to refined production, while the other moved to rapid iteration. SushiSwap, which had been stealing liquidity from Uniswap, had been exploring laterals in more areas (such as lending, crowdfunding, and issuance), while Uniswap had been exploring in-depth AMM and composition. Uniswap focused on optimizing systems and digging deep into AMM, with little caution in its roadmap. SushiSwap shifted to the community, community initiative, community feedback, and voting, which led to strong momentum.

In the first half of 2020, a serious “liquidity dries up “ event occurred in the whole digital asset, and the market plunged. After experiencing the explosion of market capacity, market stress test, and the second reshuffle of pattern, in continuous improvement, DEX under AMM model represented by Uniswap, SushiSwap, and Curve accelerated operation. The market trading volume and user number both experienced exponential growth. By the end of December, trading volumes in the top nine DEX projects rose 17,989% to $29 billion.

However, in 2020 DEX faced a new challenger: the rising cost of Ethereum gas. As a result, decentralized financial protocols focused on multi-chain solutions, as they were better suited to handle high trading volumes. Therefore, we saw the new public chain ecosystem outbreak and Layer 2 in 2021, the market scale of DEX overgrew, and the market competition pattern became increasingly fierce. Despite the apparent head effect of DEX, a few platforms accumulated the volume (Uniswap, SushiSwap, and Curve, for example, account for more than 80% of the trading volume in the whole Ethereum DEX market). But due to the congestion and high gas charges of Ethereum itself, as a result, these DEX projects faced competition from non-Ethereum DEX. In recent years, DEX projects run by CEX have sprung up. Represented by MDEX on the HECO chain, PancakeSwap on BSC, Serum on Solana chain, and Kyber DMM on the Fantom chain, trading volume and locked volume are extraordinarily brisk.

**

DEX evolution: Start with AMM**

Turn back the clock to the end of 2021.

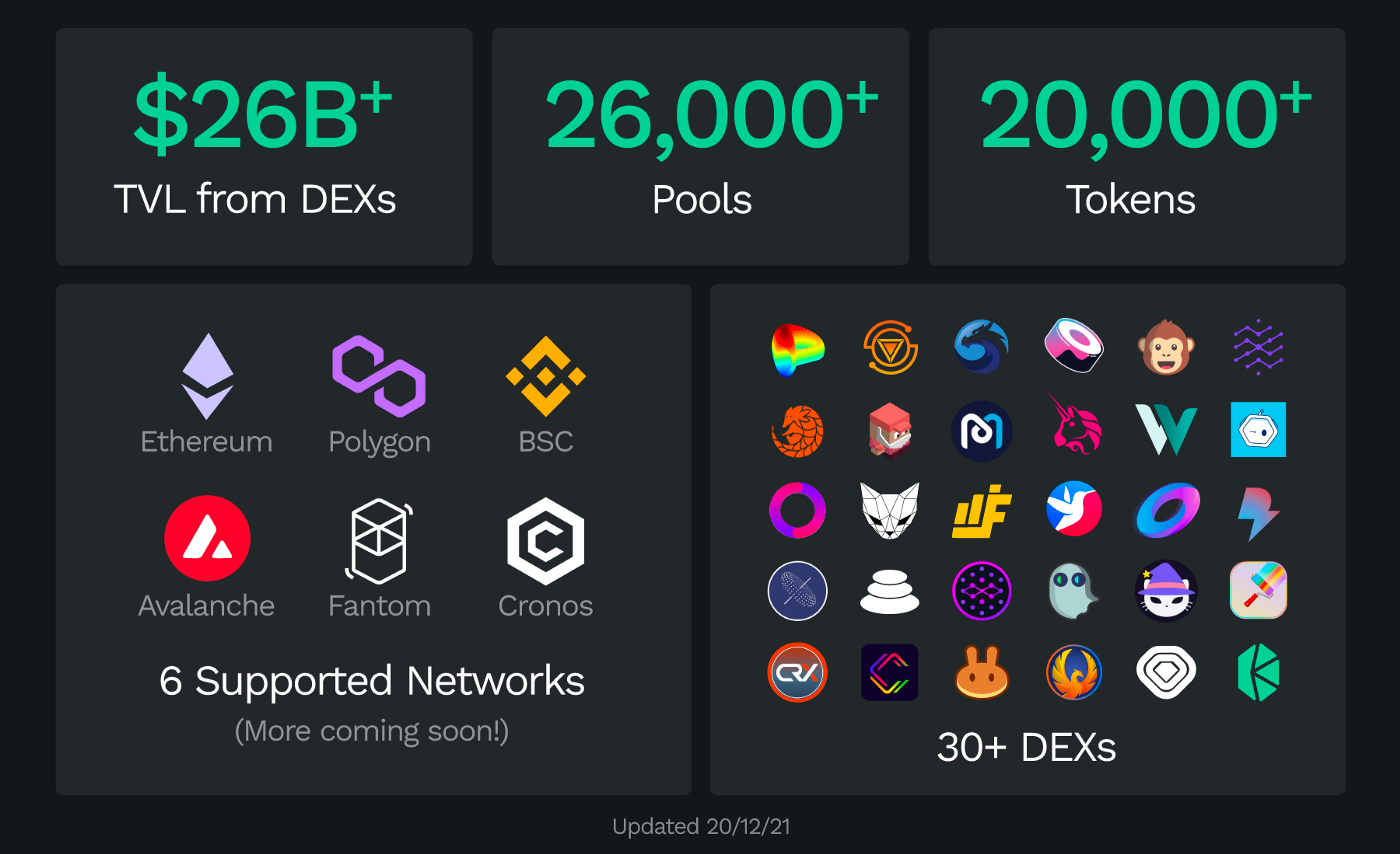

There are currently 433 cryptocurrency exchanges, according to CoinMarketCap. From traditional financial exchanges, CEX to DEX, this number undoubtedly condensed the evolution of the whole process. The crypto market grew, DeFi flourished, and DEX, the ecological backbone of DeFi, on a meteoric rise since the summer of 2020.

Of course, it’s more than that.

In terms of value locked, DefiLlama showed that Defi’s total value locked (TVL) reached $233.59 billion, among which DEX accounted for $71.22 billion, and DEX TVL accounted for 30.4% of Defi’s total TVL.

According to statistics from Dune Analysis, DEX’s trading volume reached more than $1 trillion in the past year, up 858% from 2020, and the number of trading addresses reached 4,492,331. In the last three years, monthly trading volume increased dramatically in 2021.

Now, regardless of the numbers, let’s re-understand what DEX has brought us. In the current design of DEX, there are mainly AMM (Automated Market Maker) and order books. The order book model is similar to the order matching model of CEX, and more protocols currently adopt the AMM model. There are several types at present: Constant sum market makers (CSMM), constant mean market makers (CMMM), and advanced mixed constant function market makers (CFMM).

AMM refers to an algorithm that simulates human market-making behavior in traditional financial terms. But it has evolved into an engine of violence in DeFi. It uses automated algorithms to balance the supply and demand of tokens in the trading pool, avoiding the situation where a single market can lead to a particular generation of coins being bought out (no buyer/seller listing) in an order book model. In addition, DEX in the AMM model gives part of transaction fees to liquidity providers, encouraging them to inject idle assets into the trading pool to provide liquidity, which solves the problem of insufficient transaction depth in the order book model to a certain extent.

Indeed, when we talk about DeFi and its vision of financial inclusion, it is always through the implementation of AMM-based DEX. It democratizes access to market-making and liquidity provision, allowing investors to trade seamlessly between cryptocurrencies fully decentralized and unmanaged through pre-raised pools of on-chain liquidity. By depositing only funds in these on-chain liquidity pools, liquidity providers can earn passive income on their capital based on their percentage contribution to the pool.

AMM-based DEX has proved to be one of the most influential DeFi innovations. The emergence of AMM breaks the restrictions of the order book and matchmaking. It helps DEX break CEX’s monopoly on the cryptocurrency trading market and makes permission-free and open on-chain trading a reality. But in the process, the other side of the coin has also slowly come to the surface: expensive gas costs from on-chain transactions, speed effects from network congestion, forced multi-currency exposure, impermanent loss, slippage loss, etc.

Problems arise and are always waiting to be solved. For the issues in the AMM model, the corresponding DEX head platform is also constantly explored.

The Balancer has implemented a constant function algorithm to introduce more than two assets with weights other than 50–50. Like AMM’s predecessor Bancor’s update to V2, Balancer’s V2 uses unilateral liquidity to address impermanent loss. Curve modifies Uniswap’s AMM functionality to minimize asset slippage with relatively stable prices; Uniswap also continued version iteration. V2 expanded the trading pair compared to V1 and supported any ERC-20 Token, and Liquidity Provider (LP) Token can automatically compound interest and continue to flow. Uniswap V3 introduced the concept of concentrated liquidity and improved capital utilization through various initiatives and so forth.

So, what is the endpoint of DEX evolution in these improvements to the AMM mechanism?

DEX Attack Ⅰ: from TVL to EV

TVL, as defined by CoinMarketCap: “To get the current market value, you need to multiply the amount of outstanding supply by the current price.” TVL is calculated by multiplying the amount of money locked as collateral in the ecosystem by the assets at the current price.

Market value equals the supply in circulation multiplied by the price of tokens (especially native tokens). TVL equals the asset price of the amount of money pledged or deposited multiplied by the asset prices (not necessarily native tokens).

Undeniably, when comparing DeFi dApps, TVL is a favorite metric, and the higher the value locked in DeFi dApp, the better. There are two reasons for this:

- It shows how fast DeFi is growing: According to DeFi Llama, Ethereum DeFi’s TVL was just $1 billion at the start of 2020, compared with more than $241.88 billion at the end of 2021.

- It creates a nice illusion that there is a lot of liquidity in DeFi pools where investors and others can earn income.

It does show DeFi’s growth rate; So why do we think the “massive liquidity and substantial returns” TVL represents is a “ nice illusion”?

Firstly, it is a potentially skewed indicator because it doesn’t consider the extent to which each unit of locked token is utilized. $1 million locked on Kyber is not the same as $1 million locked on Uniswap or Bancor. For example, Kyber can provide liquidity for multiple tokens from the same ETH pool, i.e., one ETH may meet the liquidity needs of 10 different ERC20 tokens on Kyber. At the same time, each token pair on Uniswap requires its own separate ETH pool. It needs 10 ETH to service these 10 tokens. As a result, Kyber needs to lock up far fewer assets to provide the same level of liquidity.

Secondly, the reasons for the increase are not real. Part of the reason behind the huge growth of DeFi TVL on Ethereum is the outrageous APY offered by many protocols. Due to the blind pursuit of TVL, a protocol is keen to carry out a liquidity mining program competition, essentially liquidity rent for TVL. There is no loyalty in the face of benefits. Once the rewards dried up, these employment liquidity providers withdrew their assets and moved on to the next opportunity, leaving diluted tokens and underutilized protocols.

Thirdly, it does not reflect the utilization rate of funds. A significant number of TVL has the appearance of an obese giant. Although a lot of money is locked up in some protocols but not used at all, it is just a pool of stagnant liquidity. And how can an inefficient protocol deliver substantial long-term and sustainable benefits?

Further, if TVL is the core metric of DeFi, then this is a game rule for Poof of Capital. It is very different from the ideal of inclusive finance that DeFi points out.

It is the context in which we propose EVL; ok, what is EVL?

Effective Value Locked (EVL) means the value in use. It is not a conceptual replacement of TVL but a measurement supplement of one more dimension. It reminds us that we should care about the value of being locked up and pay attention to the value of being used when evaluating a DEX. Just as no matter how amazing the TVL of this DEX is, we should also pay attention to the situation of impermanent loss on it.

If the pursuit of TVL is the logic of capital accumulation, the pursuit of EVL represents a logic of value regression. Because under normal circumstances, most income in DeFi protocol is from the transaction fee, and the key to LP profit is transaction fee income is higher than impermanent loss. On the premise that LP is of the same order of magnitude and platform trading volume, EVL positively correlates with LP turnover rate. The higher EVL is, the higher the LP’s turnover rate and the higher returns are. It will become a more core reference when evaluating protocols and guiding investments in the long run.

So how do we calculate EVL?

Generally speaking, we calculate the capital utilization rate: the daily capital utilization rate equals the 24-hour trading volume divided by the TVL. According to OKLink data, the DEX capital utilization rate on Ethereum was 12.16% on June 29, 2021, down 2.84% from the previous month. The top three DEX of capital utilization rate are DODO, Uniswap V3, and Uniswap V2, respectively, corresponding to 87.18%, 51.68%, and 8.82%. If you take into account fluctuations over time, you might calculate the effective utilization rate as follows:

The EVL equals the 30-day average asset utilization times the 30-day TVL average.

According to our analyzed data, the top three DEX are DODO, Uniswap, and SushiSwap, with an average asset utilization rate of 24.46%, 5.98%, and 3.21%, respectively. The top three DEX in TVL were Curve, Uniswap, and SushiSwap. The top three EVL DEX are Uniswap, SushiSwap, and Curve.

We can see that the capital utilization rate of most DEX is not high. Uniswap, SushiSwap, and Curve, three long-established DEX, have a monopoly advantage in TVL by strong network effect, and their EVL still ranks high.

DEX Attack Ⅱ: Pareto Optimality of capital efficiency

We already understand that the TVL is not the best indicator to pursue, so why do most DeFi projects attract as much liquidity as possible?

Quite simply, people like huge numbers, and the bigger the number, the more eye-catching it is. From a marketing standpoint, this is understandable, as this is clear evidence that there is a huge amount of liquidity in the pool, which attracts more traffic.

Admittedly, high liquidity is not a bad thing in itself. However, it is inappropriate to chase it excessively. The huge increase in TVL of DEXs in the past two years has confirmed part of the validity of this indicator, and it is time to focus on the next frontier direction.

In terms of the evolution of DEXs, we believe that the actual outcome of DEXs (and indeed the entire DeFi world) will depend on another question: Who will achieve a Pareto optimal capital efficiency?

Essentially, improving capital efficiency is a main theme with the previously mentioned EVL because the low capital efficiency reflects the underutilization of liquidity. When the utilization of funds ineffective hedging is high, capital efficiency naturally increases. So why not pursue the highest capital efficiency but optimal? It involves many balancing factors, risk appetite, asset preference, time preference. It means that when an ideal state of resource allocation is reached, the cost of other options can be minimized.

For investors, capital efficiency is the relationship between the amount someone spends to increase their income and return. If capital efficiency is high, it will spend less and earn more. For the project side, the DEX cannot maintain sufficient liquidity. It will collapse under the pressure of traders trying to transfer funds and assets quickly without a high capital efficiency ratio. The more efficient the capital, the more it proves that this protocol is being operated efficiently. The Pareto optimality of capital efficiency that DEX tries to achieve is to provide options that, when investors make a strategy portfolio, each option has a considerable return from one combination to another.

Of course, around the core theme of capital efficiency optimization, many of the protocols updated this year have given their direction of exploration.

1. “Centralized Liquidity” of Uniswap V3

In the original version of Uniswap V1 and previous versions of Uniswap V2, liquidity Providers (LPs), like the rest of the AMM, were required to accept their assets in the liquidity pool at any trading price range. It means that these assets were likely to sit idle instead of putting them into use at a more specific price and getting the benefits.

At the core of the Uniswap V3 upgrade is to provide a way called “concentrated liquidity,” in which LPs will be able to market within custom price ranges so that LPs can build a personalized price curve that reflects their preferences for maximum return.

Looking at Uniswap’s DAI/USDC pool, most trades are concentrated between $0.99-$1.01, but only 0.5% of the LP funds are used in this range, and the remaining 99.5% are of the funds are never used. According to the Uniswap blog post, in Uniswap V3, the LP can select a customized price range when providing liquidity — for example, centralizing the $25 million DAI/USDC pool in V2 in the price range from $0.99 to $1.01 of V3. It will provide the same depth in this price range as the $5 billion in V2, with a maximum capital efficiency of 4000 times. It makes V3 a very flexible protocol adapted to different assets, while the transaction fee can also decrease to 0.05% (and Curve is down 0.04%).

By comparing the prices of the DAI/USDC pools at V3 and V2, respectively, the V3 pools are technically able to support a range as small as 0.02%, i.e., aggregate liquidity through “granular management,” but this also introduces the loss of gas fees.

As Messari mentions in their yearly review: Centralized liquidity is the future of AMM*, which the early success of V3 demonstrates. Since its launch,* Uniswap has increased its DEX market share to more than 70% (In June 2021).

In addition, the Uniswap V3 fee structure has changed. V2 has a fixed transaction fee of 0.30%, paid to the pool’s liquidity providers. V3 canceled the fixed fee and instead introduced four tiers: 0.01%, 0.05%, 0.30%, and 1.00%. LPs to set lower rates for less volatile assets (such as stablecoin) but higher rates for more volatile assets.

Let’s look at two ETH-USDC liquidity pools on V3 — one is 0.30%, and the other is 0.05%. From the data point of view, the TVL of the high-rate pool is relatively high, so it confirms that the LP is more inclined to the high-rate pool. Funds utilization is higher for the pool with a lower rate: average fund utilization of USDC/ETH 0.05% Pool exceeds 200%, about ten times that of the USDC/ETH 0.3% pool (the average utilization rate of funds is 20.85%).

Why? Because the lower fee pool offers traders better prices. In the case of liquidity concentration, there is also an impact on trading volume. For traders, the volume will be prioritized to the pool of low rates (0.05%) under the user-set slippage. If this pool is not liquid enough, the remaining ones will go to the medium rate (0.30%) and go to the pool of 1.00% of the high rate. Although much fewer funds enter the pool, slippage is still very low, and low slippage leads to a trader’s preference for a 0.05% fee pool, ultimately increasing overall fund utilization. It suggests that the rate tier is set up to allow Uniswap V3 to compete more effectively with DEXs such as Curve that is specifically directly with DEXs (especially stablecoin) of narrow price range trading pairs Curve through lower fees.

The V3’s average trade size is about 30 times higher than v2’s, reaching a staggering $60,000 by the end of the year.

It is worth noting that while Uniswap v3 popularized the concept of leveraged liquidity provision, the trading horizon that provides liquidity is narrowed. A higher degree of capital efficiency is achieved by eliminating unused collateral. This leverage increases the fees earned and risks, namely the impermanent loss. According to the research, 17 asset pools of the TVL exceed $10 million (account for 43% of the TVL) with a trading volume of more than $100 billion, which earned LP about $200 million in fees during V3’s launch from May 5th to September 20th. However, the impermanent loss caused more than $260 million during the same period, resulting in a net loss of more than $60 million. In other words, about 50 percent of V3 LP is in the red.

It shows a trade-off between risk appetite and efficiency preference. A higher capital utility may also bear the greater impermanent loss (especially for non-professional market makers). Although Uniswap V3 has also produced a new solution for impermanent loss, allowing liquidity providers to redeem only within the exchange rate range they accept through the “Range Orders” function, it still inevitably faces similar challenges.

2. DODO: Bring professional market makers on the chain

The design idea of Uniswap V3 is very similar to the PMM (Proactive Market Making) model launched by DODO. The core idea of PMM is to guide prices by introducing oracles gathering funds near the market mid-price, which can achieve a relatively flat price curve to improve capital efficiency. It provides liquidity as good as a CEX by mimicking human market maker behavior.

The figure shows that the DODO’s curve is flatter than the Uniswap V2’s curve near the market price, indicating higher capital utilization and lower slippage.

As we all know, AMM is often referred to as “inert liquidity” because the price points offered to traders are uncontrollable and not as knowledgeable and flexible as traditional market makers. It is where DODO intervened, and in early March this year, DODO officially launched the V2 version to bring professional market makers into the chain through the launch of DODO Private Pools (DPP).

In simple terms, market makers can leverage these private markets and customizable the PMM’s liquidity pools to deploy tailored strategies on the chain and react dynamically to market conditions. Market makers also can open up pools of capital to common users LP, an exciting step in the democratization of professional market makers.

We can see that after the launch of DODO V2 by analysis of data, the monthly average capital utilization rate increased from 42.17% to 77%, which significantly improved capital efficiency.

In addition to bringing professional market makers into the chain, DODO will also provide active market-making tools/liquidity management tools for other Protocols or any developer. It enables them to market their Protocol Token with the DODO DPP tool, significantly increasing asset efficiency. At present, DODO V2 has supported various asset issuance models: crowd-built pool, price increase auction, fixed price issuance, and customized bonding curve issuance. Meanwhile, it recently launched the NFT asset issuance platform supported by the PMM algorithm, which uses the fragmentation, pricing, trading, and buyout collection of NFT and other assets, allowing users to establish a highly liquid market at a very low cost.

3. Curve: Cross-asset exchange and automated market making

Curve, which focuses on providing stablecoin trading with low slippage, is the solution to improve asset efficiency.

The first trick is to do cross-asset exchange using the modularity of DeFi.

On January 18, 2021, Curve announced the launch of a cross-asset exchange trading service in partnership with Synthetix, a synthetic asset protocol. While Curve positions as a DEX specifically designed for stablecoin since its launch, AMM has shown the market a unique approach to improving capital efficiency in its innovative integration with Synthetix.

Specifically, Curve’s cross-asset exchange process involves two transactions. Taking DAI to wBTC as an example, First, DAI is converted to sUSD and then to sBTC; Second, sBTC will be converted into wBTC. In the whole process, Synthetix’s mortgage synthetic asset model was used as a bridge to achieve no slippage in exchange. In the end, CFMM of Curve was used to achieve extremely low slippage in exchange for sBTC and wBTC(Although the trading slippage of this scheme is almost zero, the asset price may change sharply during the 6-minute calculation period and cause losses).

The second trick is to use the “internal price oracle” to achieve automated market making.

In the Curve Crypto white paper, updated on June 9, 2021, they performed an upgrade to rebalance users without proactively setting up their liquidity. The implementation principle is to obtain a reference price through its internal oracle EMA (Exponentially Moving Average), which combines the Curve’s historical price and the latest trading price. Curve V2 can construct a new price curve with EMA so that liquidity is re-aggregated near the market price. On the one hand, it can achieve better liquidity and improve asset efficiency, and on the other hand, it is also conducive to reducing the impermanent loss of LPs.

At present, Uniswap V3 has given rise to professional LPs, providing market-making management services for common LPs. Through liquidity aggregation, Uniswap V3 essentially introduces the competition of LP market making: professional LPs will adjust the price range of their liquidity in real-time according to market price changes to obtain greater returns. At the same time, it is difficult for common LPs to adjust in time, leading to relatively lower capital efficiency and fee share. From an LP market-making perspective, Curve V2 is more friendly to common LPs, simply injecting funds into the liquidity pool and leaving the rest to Curve’s new changing curve.

In addition, we should not overlook that the launch of Convex Finance triggered Curve’s strong token economics and the Curve Wars. In May, it drove a surge to TVL in 2021 (currently TVL of the number one DeFi protocol exceeds $23 billion) and a high locked rate for CRV tokens (about 350 million CRV tokens are locked with an average lock-up period of 3.64 years).

Based on data calculations, the EVL indicator of Uniswap V3 is still 6.7 times that of Curve, which shows that Uniswap V3 is still leading in capital utilization efficiency based on its unique LP design. However, it still lags behind Curve on traditional metrics such as TVL due to previously lacking liquidity mining incentives in Uniswap V3. It is worth noting that Izumi Finance, launched in December 2021, serves as the programmable liquidity platform built on Uniswap V3 to complement the missing “convex-like” link in the Uniswap V3 ecosystem. The Uniswap V3 liquidity providers only need to pledge LP NFT tokens on the Izumi platform. As long as the NFT is in the incentivized trading pool and price range, they can receive liquidity incentives, which greatly increases the investment return of Uniswap V3 liquidity providers. At the historical data level, the current APR is stable at 20% after Izumi started USDT/USDC liquidity mining activities in Uniswap V3@Polygon, bringing a 50% TVL increase to its trading pair pool. LP, currently involved with Izumi on Uniswap V3@Polygon, has accounted for 73% of the total TVL of the USDC/USDT capital pool.

Looking back at DeFi summer in 2020, its explosion is largely due to the high returns generated by various types of liquidity mining that emerged at that time for liquidity providers. Uniswap V3 could not be designed for a long time due to its unique LP NFT design. SushiSwap and Curve carried out much of this activity. But now Uniswap V3, with the blessing of its ecological project Izumi, has an upgraded version of the programmable liquidity mining mechanism, so in future development, it is expected to have a greater impact on Curve’s TVL leading position.

4. SushiSwap’s BentoBox and Balancer V2: Single Vault

One of the reasons why investors are not capital efficient is that transaction costs are too high, such as gas fees being wasted on multiple approvals of the same token.

SushiSwap and Balancer have taken a joint look at this problem and offer a similar solution: a single vault. A single vault allows internal token balances to be maintained within the vault. Once a token is approved for use in the vault, it can be used for all protocols established on the vault, thus guaranteeing gas efficiency by reducing unnecessary token transfers.

“What makes BentoBox innovative is its effortlessly scalable design. Its scalar design allows BentoBox to serve as the infrastructure for the DeFi protocol on future Sushi. Unlike other protocols, it creates a major source of liquidity that any user can access with minimal approvals, minimal gas usage, and maximum capital efficiency. “

— SushiSwap, May 2021

Similarly, Balancer V2’s vault protocol changes the overall architecture of V1, implementing a separate vault for holding and managing all assets held in the balancer pool.

Bulk transactions are made against multiple pools with Balancer’s new vault, and only the final net token amount is transferred out of or transferred to the vault, saving a significant gas fee in the process. It is possible to make a single settlement for multiple transactions in Balancer V2, which dramatically benefits high-frequency trading. In addition, through Flash Loans, arbitrageurs can arbitrage even if they don’t hold tokens by trading information between pools of funds, which can improve process efficiency and reduce capital-intensive operations.

Because AMM is separated from token management and accounting for vaults, a pool of funds can implement any arbitrary, customizable AMM logic, including a weighted pool (for constant-weight index funds), a stable pool (for soft-linked tokens), and a smart pool (for ongoing parameter changes). It means that traders with different risk appetites execute different types of AMM strategies.

Balancer V2 also introduces the asset manager feature. An asset manager is an external smart contract designated by a pool to manage tokens deposited in a vault. Asset managers can process idle tokens in the vault, such as lending to partners such as AAVE to improve capital utilization.

Both BentoBox and Balancer’s vaults will allow dApps integrated into the vault to connect, so dApps can realize various user scenarios based on which to provide synergies between these dApps, which opens up vast design space for capital efficiency: after being nominated by the pool, external smart contracts that have full control over the tokens of the pool of funds can play a role by using the underlying tokens for other aspects, such as voting, income farming and lending to bring various potential benefits to users logically as well. At the same time, dApps brings new users to the vault, allowing TVL and protocols to grow.

5. KyberDMM

This year, DEX KyberDMM, the first high capital efficiency and liquidity convergence on the Fantom chain, was launched. It is the first multi-chain dynamic market maker in the DeFi field. Compared to “traditional” automated market makers and token exchange services, KyberDMM DEX has some key advantages: dynamic transaction routing, amplified liquidity pools, and dynamic transaction fees.

In simple terms, KyberDMM DEX maximizes capital utilization by enabling greater capital efficiency with very low slippage while reacting quickly to market conditions to optimize liquidity provider fees. In addition, KyberDMM DEX offers a new dynamic transaction routing feature that allows traders to aggregate liquidity from various DEXs on the Fantom blockchain to discover the best token price.

In terms of capital efficiency, the key to Kyber DMM is introducing the Capital Amplification Factor of Liquid Pools (AMP) and dynamic fees based on market conditions. AMP is set up through a programmable pricing curve for Kyber DMM. The creators of liquidity pools can customize the pricing curve and set the AMP of the liquidity pools in advance. Meanwhile, liquidity providers can select the pool to inject liquidity based on AMP.

The Future of DEXs: Trade-offs and Evolution

Just as DeFi’s growth has never stopped, the iteration of DEX in this year is still remarkable:

Uniswap V3 is committed to “centralized liquidity.” Although there are some criticisms that the resulting liquidity competition will cause unfairness, its determination to optimize capital efficiency is still impressive. Curve was the first Swap to take advantage of DeFi composability, and it re-optimized its market-making curve. Not only did it fend off Uniswap V3’s position in the stablecoin market, but it also dominated TVL for a long time, sparking a Curve Wars at the end of the year. BanlancerV2 introduced protocol vaults and asset managers (asset managers); DODO, Kyber DMM is mainly based on customized AMM curve logic and guides the direction of on-chain market makers and centralized liquidity. It is a pity that its long-simmering next-generation Trident has an uncertain future after SushiSwap broke out in fighting.

In addition to the eternal theme of capital efficiency, if we mention a little more about the future direction of evolution, we may think:

- As the performance of the public chain improves, the flexibility of future order book transactions may cause some DEX modes to return from AMM to the order book. The two modes of DEXs will coexist, which we can already see in data: according to the Block’s report, although most of the volume is carried out through AMMs, the largest order book-based DEX by volume is Serum, with a volume share of 2.6%.

- With the increasing number of DEXs and the increasingly fragmented liquidity, users may prefer to transact through DEX aggregators. 1inch was the leading DEX aggregator in the past year, with a market share of 64.9%, followed by 0x API (Matcha) with 16.8%. Overall, only 13.9% of DEX trading volume comes from aggregators, and a large amount of trading volume comes from DEX local routers or trading robots.

“There is no single right way to provide liquidity — it simply depends on your risk tolerance, your asset preference, and your expectations of future price movements. Exposing these trade-offs, and allowing LPs to choose for themselves, is the only way to increase the efficiency and usefulness of AMMs” — Hayden Adams, Uniswap CEO

As Hayden Adams points out*,* there is no single right way to provide liquidity. After all, this is a user preference choice problem. There are many factors behind the trade-off to improve capital efficiency, such as risk preference, asset preference, time preference mentioned at the beginning of the article. To optimize capital efficiency, iteration, no matter in which dimension, will give rise to new market opportunities, and naturally, there will be different trade-offs. Exposing these trade-offs and allowing LPs to choose for themselves is the only way to improve the efficiency and utility of AMMs.

Reference

- https://www.theblockcrypto.com/post/99100/uniswap-v3-capital-efficiency-details-dex-ethereum

- https://rekt.news/uniswap-v3-lp-rekt/

- https://messari.io/article/uniswap-v3-capital-efficiency-at-its-finest

- https://messari.io/article/the-past-present-and-future-of-decentralized-exchanges?referrer=grid-view

- https://www.chaininfo.top/news/9625228.html