To understand whether or not Bitcoin is a bubble, we must first come to an objective consensus on what defines the subjective term “bubble”. Ideally, this can be achieved by breaking the “bubble” idea down into smaller parts, and using them to analyze historical analogues to the Bitcoin bubble.

The most obvious analogue for the Bitcoin bubble is the dot-com bubble. Both phenomena were accompanied by growing global adoption of revolutionary information technology. What similarities and differences can we ascribe to each different bubble?

What Defines a Bubble?

In the finance space, usually the term “bubble” refers to the inflation of the price of an asset, commodity, or security in relation to its valuation. Market participants drive assets high above their technical valuation until the bubble pops, and the price dumps.

Some analysts ascribe financial market bubbles to behavioral finance. The insane buy-pressure is relative to cognitive bias related to herd behavior. Over-zealous speculative investors see their peers investing in the next new thing, and are eager to participate as well. Other behavioral explanations suggest that bubble behavior is rational, intrinsic, and contagious.

The claim that bubble behavior is rational came from an article dated 1990, of which I can no longer find a copy online. Perhaps this type of macro herd mentality seemed rational at the time, but times have changed. Three decades later, the internet and social media facilitate the transfer of data in speeds that used to be unfathomable. Herd behavior, like meme coin speculation, happens in a matter of hours or days, not over years. Can we still call this kind of macro movement a bubble when it is observed to span months, and even four-year cycles, in the current decade? To approach this question, we must investigate the most obvious analogue to the Bitcoin bubble.

The Dot Com Bubble and Bitcoin

The dot com bubble, or internet bubble, was a stock market bubble caused by excessive stock market speculation of internet companies in the late 90s. Between 1995 and its peak in March 2000, the Nasdaq Composite stock market index rose 400%, but later fell 78% from its peak by October 2002, effectively relinquishing all of its gains during the bubble. Many online shopping companies failed, like pets.com, but others survived, such as amazon.com.

Before the Bubble

The 1993 release of Mosaic software facilitated global access to the world wide web. Between 1990 and 1997 the percentage of households in the United States owning a computer rose over 100%. Simultaneously, the Taxpayer Relief Act of 1997, along with other economic factors, allowed people to participate in more speculative investments. Investors, equipped with additional liquid, were more eager to speculate in the nascent field of information technology, regardless of stock valuation. Any internet company, especially those with .com suffixes, were the target of overconfident investment. There was a significant number of individuals who quit their job to speculate in the financial market. On-paper millionaires were made… but most didn’t exit before the bubble burst.

The Bubble Bursts

The year 2000 marked the height of the dot com bubble. AOL merged with Time Warner company. 20% of Super Bowl XXXIV ads were purchased by dot-com companies (most were at least $2M investments). Billions of dollars were spent without much revenue generation outside of the valuation of company stocks. The bubble’s deathknell rang throughout late 2000, when Alan Greenspan, Chair of the Federal Reserved, repeatedly raised market interest rates several times, until… *pop*. All that was left of the bubble was the mess.

How much of the infamous dot com bubble narrative actually applies to Bitcoin? Bitcoin has enjoyed periods of rapid price increase, which empirically have been followed by periods of recession. However, the dumps that proceed the peaks never dipped below price levels leading to the bubble, as in the dot com craze. Bitcoin is no new phenomenon - it has experienced 2 prolonged “crypto winters” since its inception, but every time that people claim “the bubble has burst”, Bitcoin eventually rallies to fresh heights.

It is important to note that the technical functionality of Bitcoin as an asset far exceeds that of stocks. Bitcoin is the representation of blockchain as cutting-edge financial technology, whereas the dot com bubble represented the implementation of old business models on the new network of the internet. If decentralized finance continues on its course, and isn’t slain prematurely by excessive regulation, it will be a *financial revolution*: the great global redistribution of wealth within a new financial paradigm.

The terminology “bubble” applies to some obvious aesthetic similarities between the dot com bubble and Bitcoin, but how similar are the two phenomena, separated by over two decades?

If Bitcoin is a Bubble, then What Type of Bubble Is It?

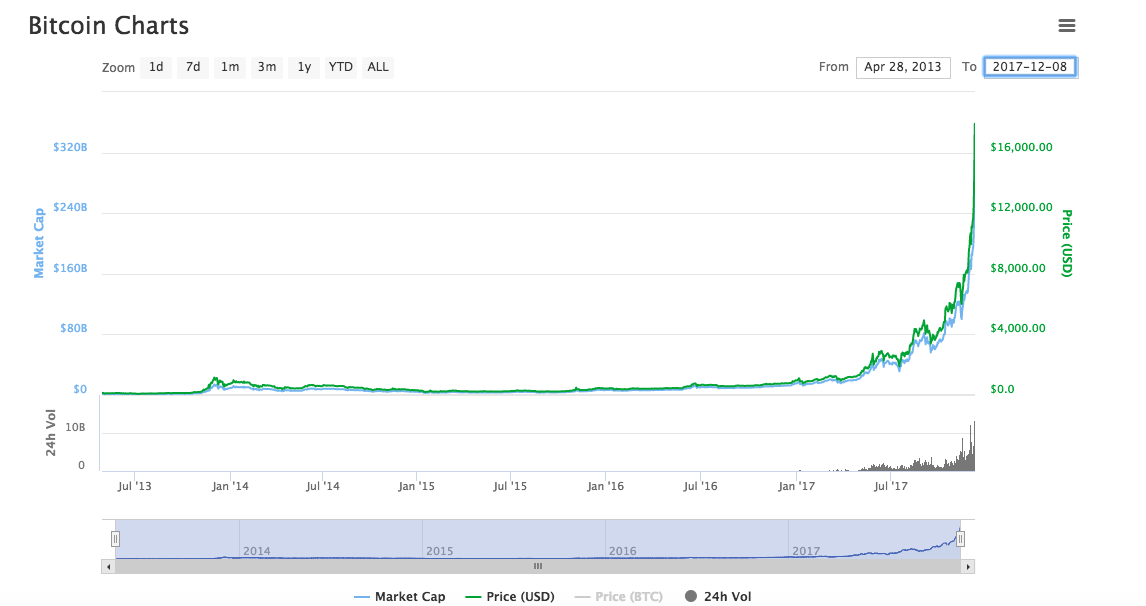

In my research, I came across a fascinating piece of journalism by Miko Matsumara titled Comparing the Bitcoin Bubble to the Dotcom Bubble. It was written almost at the height of the 2017 bullrun, when Bitcoin was priced at $19,000. Miko argues that of course Bitcoin was a bubble, but so is finance, and so is the universe for that matter. Everything is a bubble. Intrinsically, bubbles, after experiencing an exponential growth curve, are followed by a dump.

In retrospect, Miko’s analysis was impressively sharp mid-term financial (non)advice. He almost called the exact top of the 2017 Bitcoin bullrun. But his analysis goes deeper. Miko compares Bitcoin to gold, calling it the gold standard of cryptocurrency. He also compares Bitcoin to the internet. The internet facilitates the public transfer of data. Bitcoin facilitates the *secure* public transfer of data. Interestingly, he notes that the dot com bubble peaked at $9.6T, while, even as of October 2021, the Bitcoin market cap has never exceeded $2T.

Bitcoin represents the value of cryptocurrency at large. It is the lifeline of all cryptocurrencies, and the scion of decentralized finance. Bitcoin compels financial innovation, especially in regards to the trustless custody of assets: Bitcoin never relies on a third-party during financial transactions. In contrast, the dot com crash made banks and the FDIC the targets of scandalous slander. Companies that were backed by the FDIC siphoned government funds, while the rest were left in the bubble mess. Decentralized finance, as spearheaded by Bitcoin, ensures that the individuals and institutions who speculate in the cryptocurrency market are solely responsible for their successes and failures.

**

**

Blockchain is Inevitable; Bitcoin is Not

Bitcoin is the gold standard of crypto: a single asset which represents the lifeline of an entire sector. To quote Miko,

“The Internet is without a doubt the largest transfer of information (bits) we have ever seen in our lifetimes, whereas the internet of value will be the largest transfer of wealth in our lifetimes. Netflix wants $10 of your bank account every month. Amazon maybe wants $100 of your bank account every month. Bitcoin wants your entire bank account for the rest of time.”

Backed by this, Miko claims that the secure internet of value represented by cryptocurrency has the potential to be *100x larger* than consumerization of the entire internet.

**

**

Conclusion: Zoom Out from the Bitcoin Bubble

Subjective labels, like bubbles, incite fear. The word “bubble” itself provokes memories and horror stories of past market failure. Of course there are similarities between historical events like the dot com bubble and the rise of Bitcoin, but as we’ve considered throughout this article, the most obvious similarities are merely superficial. Upon diving deeper and comparing constituent components to historical analogues, we begin to find a universe of features of the Bitcoin bubble that would be anachronistic in the dot com bubble narrative.

It is not realistic to relate macro movements of Bitcoin in 2025 to macro movements of the stock market in 1995. Information travels orders of magnitudes faster than it did in the 90s with the 9-5, 5-day-a-week stock market. Cryptocurrencies trade nonstop, and if you forget to check Twitter tonight, you might already be late to the latest groupthink meme coin tomorrow. Yes, Bitcoin will fly higher, and yes, afterwards it will probably dump, but that dump won’t end in a generational mess that ruins fortunes (for most - play it safe, Degens).

To those who are afraid that this bullrun is the last stand of cryptocurrency, I say: zoom out. Blockchain technology is not going away. Cryptocurrency is arguably the most progressive application of blockchain. Decentralized finance is emerging as a *truly revolutionary* system that flips capitalist maxims topsy-turvy.

At less than two decades old, cryptocurrency is just beginning. The last Bitcoin ever minted will be mined in the year 2140. Until then, we have a lot of building to do.

Imagine blowing a colossal, hyper-viscous bubble. One that will take many subsequent breaths to fully inflate. Envision taking a huge breath, then blowing. The bubble begins to inflate, until you are out of breath. You start to inhale, and the bubble starts to shrink - but it doesn’t disappear. Finally, you blow out again, and look! The bubble grows to a larger size than ever before! But it still has so much room to grow. Each time you take a new breath, the bubble shrinks a bit, but each time you exhale it grows to a size never seen before. The fluid is so viscous that it seems like it will never pop, so you keep breathing, and blowing, and breathing, and blowing. Eventually, probably, the bubble will pop, but who cares? It won’t happen anytime soon, and anyway you’re having fun blowing it up.

Bitcoin is the future. Blow your bubbles accordingly.

Locke

This article was originally published under my previous alias, Demosthenes, as shown by this tweet

**

**