The default response I typically get when talking to people about algo stables is something like “are you crazy?! don’t you know about what happened to Terra/Luna???”

Having studied the Terra model and its collapse deeply, there is plenty of reason to believe that algo stables can avoid the same fate and will eventually succeed.

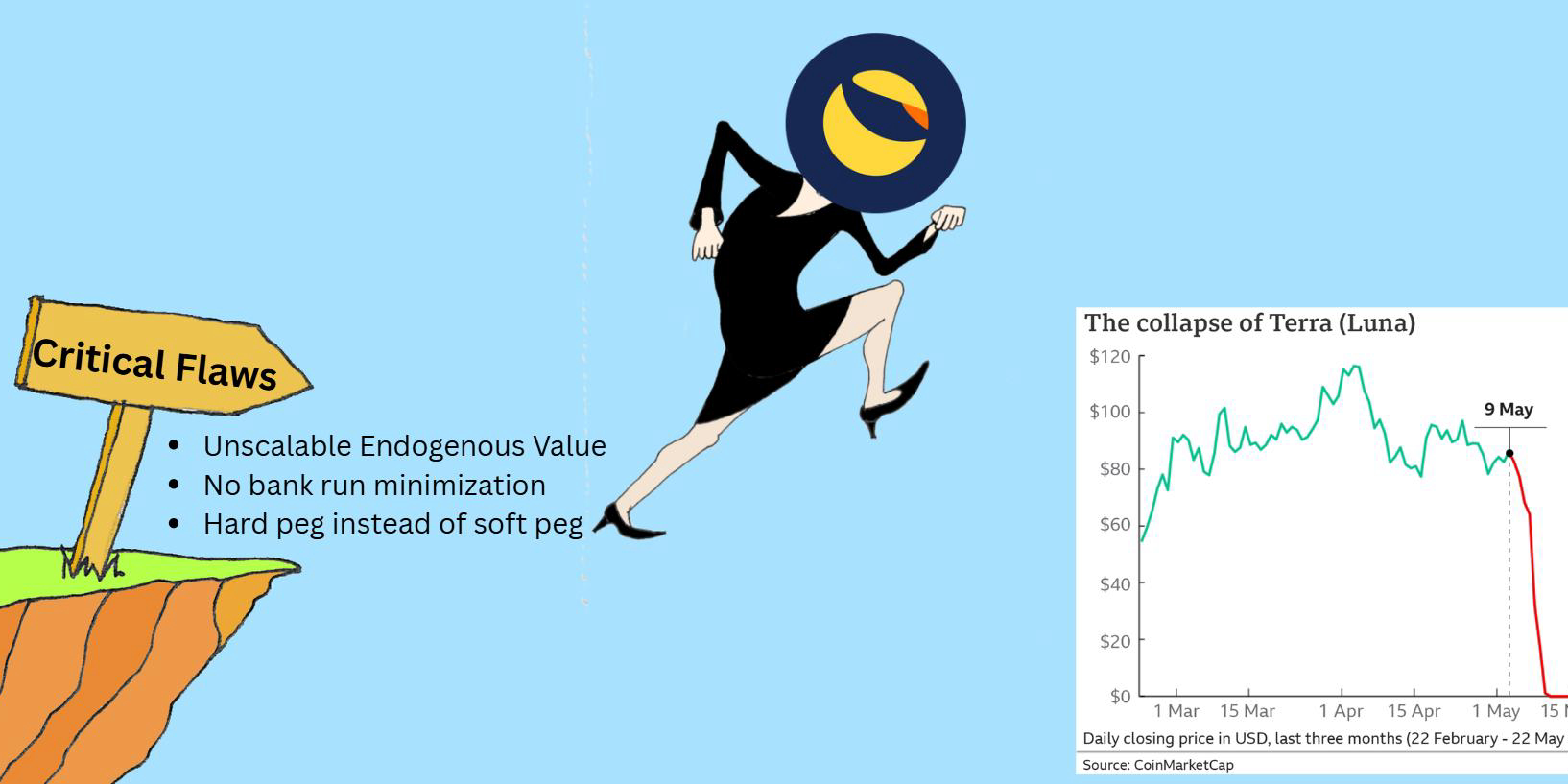

There were three fundamental flaws with the Terra/Luna model.

-

Terra used an unscalable source of endogenous value: equity.

-

Terra had no bank run minimization mechanism.

-

Terra maintained a hard peg instead of a soft one.

During Terra’s collapse, these three flaws exacerbated one another, creating a negative feedback loop that culminated in one of the largest and fastest bank runs in history.

At the time of writing, there is significant evidence that each of these flaws is solvable with proper mechanism design.

1. UNSCALABLE ENDOGENOUS VALUE

The UST stablecoin was redeemable for $1 worth of LUNA. Owning LUNA was comparable to owning equity in a company, where the value of LUNA was derived from the value of the Terra network (i.e., the use of UST). Equity is a terrible source of endogenous value.

To better understand why, let’s consider what would happen if Microsoft, a $4T company, issued MicroBucks, a $1 pegged stablecoin that derived its value in the same way (i.e., through redeemability into $1 of Microsoft stock).

At first glance, you might think that MicroBucks could safely grow up to the value of Microsoft equity, or close to it. After all, there are people all around the world that independently value Microsoft at ~$4T for reasons that have nothing to do with MicroBucks.

HOWEVER, upon closer analysis, it is not actually the market cap of the issuer that determines the number of MicroBucks that can be safely issued against Microsoft stock, it's the minimum size of the bid for the equity at any given time.

Because MicroBucks are redeemable for Microsoft stock, the ability for a MicroBuck holder to receive $1 for their MicroBuck is contingent on someone buying $1 of Microsoft stock from them after they convert their MicroBuck to Microsoft stock.

The problem is that the size of the bid at any given time for a stock (no matter how great the stock) is generally decoupled from, and always significantly smaller than, the market cap of the stock.

Herein lies the first major flaw: the equity needs to be orders of magnitude more valuable than the outstanding stablecoins in order for the bid to be large enough to process redemptions smoothly. In practice, there is no source of equity large enough to support a scalable stablecoin.

2. NO BANK RUN MINIMIZATION MECHANISM

Money is fundamentally a social phenomenon. Therefore, bank runs can always happen. The best money will have the best bank run minimization mechanism. Terra had none.

Besides the fractional demand for equity at any given time compared with its total value, the other problem with using equity as the source of endogenous value is that equity is fungible, and fungible assets offer no bank run prevention mechanism (specifically due to their fungibility).

Let's reconsider the MicroBuck example and evaluate the incentives in place for a true believer of Microsoft, someone that LOVES the stock at $4T, thinks Bill Gates is god, and has season tickets to the Clippers, in the instance where there is a bank run on MicroBucks.

Once the bank run starts, the Microsoft lover has a choice to make: hold onto their beloved Microsoft stock, or sell now to buy back later at a lower price.

Because there is a reasonable expectation that there will be a significant increase in the supply of Microsoft stock on the market due to conversions from MicroBucks into Microsoft stock, there should be ample opportunity to buy back the Microsoft stock at a significantly lower price.

In such a circumstance, even the Microsoft lover is going to participate in the bank run. When even your biggest fans are obviously incentivized to participate in causing you pain, there is a serious design problem.

The system offers no incentive for those that believe in its long term value to stick around during the bank run, and instead makes the optimal strategy to participate in the bank run. YIKES!

Worse still, anyone that would otherwise be interested in buying the stock is not going to buy until the bank run ends. During the bank run, the size of the bid for the equity (i.e., the source of the value of Microbucks) evaporates entirely.

A negative feedback loop in which supply skyrockets and demand disappears brings the price to zero in a flash.

3. HARD PEG INSTEAD OF SOFT PEG

Despite the use of unscalable endogenous value and the lack of a bank run prevention mechanism, the kiss of death for Terra was its insistence on perfection. Even in instances where the system was experiencing a bank run, the protocol was willing to offer redemptions of 1 UST for $1 of LUNA.

If someone is participating in a bank run, they are typically willing to take a haircut on their value to leave the system in a timely fashion. Instead of letting people leave the system at a discount, Terra was designed to pay every person that left the full value of their holdings, up until there was no money left.

This created two outcomes for participants during a bank run: either be one of the first to leave and get the full value of your holdings out, or miss the boat entirely and be left with nothing.

Given these two outcomes and the lack of a bank run prevention mechanism, it is no surprise that the entire system collapsed within a week once the bank run started. It was foolish to not participate in the bank run.

CAUSE FOR HOPE

With a better understanding for why Terra collapsed the way it did, it is possible to see a path forward to creating a scalable network-native medium of exchange.

-

Credit is a scalable source of endogenous value with a positive feedback loop: the more the system repays its debt, the more creditworthy the system becomes, thereby enabling it to borrow at lower interest rates and support the issuance of more stablecoins in a progressively more sustainable fashion.

-

The Stalk System originally implemented by Beanstalk and now refined by Pinto has demonstrated efficacy at minimizing bank runs in practice by creating an opportunity cost for leaving and coming back later, and rewarding those who stay.

-

Low volatility money with a soft peg still offers significant utility and is radically more sustainable than a hard pegged stablecoin: if people want to leave the system at a discount, let them; in a tradeoff between perfection and resilience, live to fight another day.

In future posts I will expand on each of these elements individually.

-ben

See the original post here.