First Published on @IOSG Medium on Aug 12, 2020

The economics behind mining

The upstream of the Bitcoin industry mainly composed of mining industry participants such as individual miners, mining farms, mining pools, and Bitcoin mining machine manufacturers. FPPS (The Full Pay-per-Share) for miners includes mining rewards and transaction fees, while PPS (Pay-per-Share) only includes mining rewards. Transaction fees can change at any time and increase when the network is congested. In the case of Bitcoin mining rewards being halved, miners’ reliance on transaction fees becomes greater. In general, the miner market is a self-balancing market, so there will be no long-term mining disasters. The impact of miners on the price of bitcoin is mainly determined by the pressure of their sales of bitcoin rewards.

The key economic factors behind mining

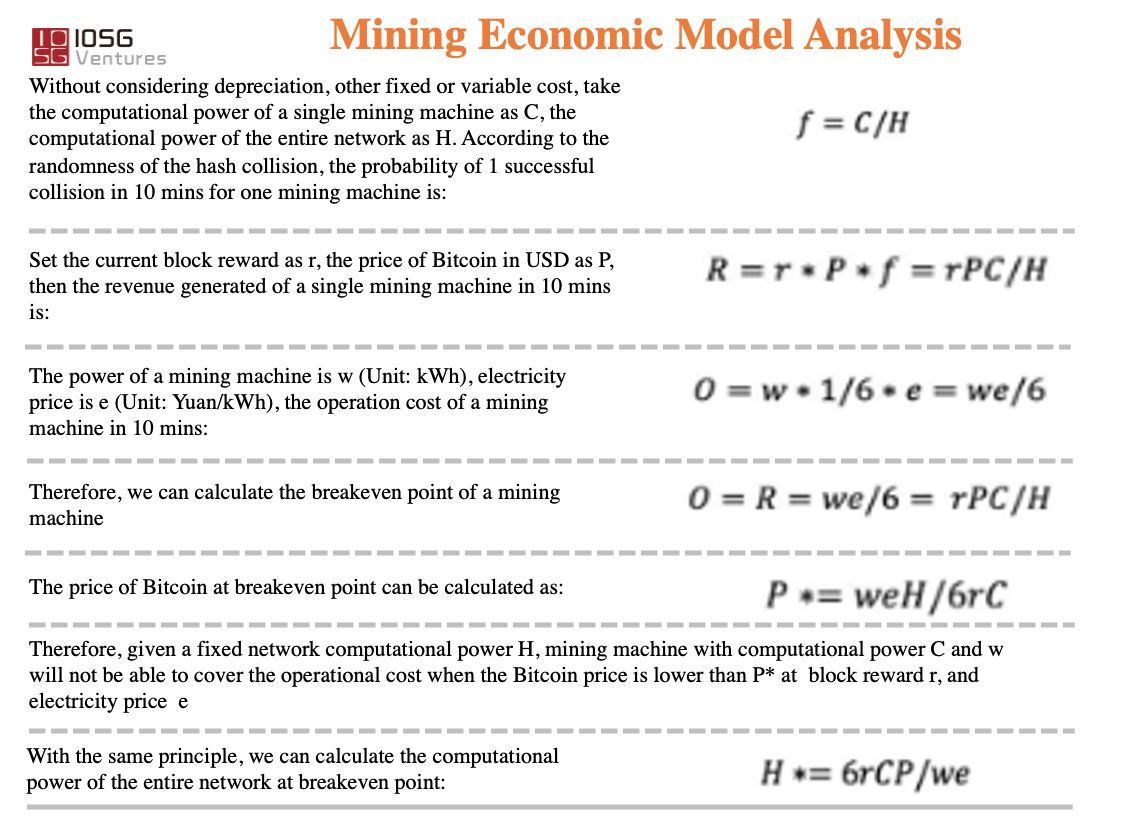

1. Bitcoin price/reward: If the price of BTC is too low or the reward decreases, the income generated by the mining machine may not cover the electricity bill which means miners need to temporarily shut down the machines or sold in the second-hand market.

2. The computation power of the entire network: The computing power of the entire network mainly depends on the capital interest in entering the mining machine industry and the performance of future mining machines. If BTC price is stable and the computing power of the entire network increases (such as the launch of a new mining machine on the market), then it may still cause the elimination of outdated mining machine, thus unable to recover the capital cost invested in the mining machine. Judging from the current market of mining machines, the income of ASIC mining machines has stabilized. ASIC mining machines refer to mining machines that use ASIC chips as the core of computing power. ASIC is an electronic circuit designed for a specific purpose. Since ASIC chips are customized for specific calculations, the efficiency can be much higher than that of general-purpose computing chips such as CPUs. At present, the main chip manufacturers are Samsung and Taipower. The new mining machines mainly use 7-nanometer chip technology, while the 5-nanometer chip is still under testing, and mass production is unlikely in the short term. Therefore, the profit of the mining machine using 7nm chips will gradually stabilize in the next few years, and it will be the most sought-after mining machine model.

When the total network computing power reaches H*, the revenue generated by the mining machine will not be able to cover the electricity bill. The computing power consumption ratio (C/w) of the mining machine shows the overall performance of the miners. The higher the computing power consumption ratio, the larger the corresponding H*.

The current computing power is showing a steady upward trend, so the higher the computing power consumption ratio of the mining machine, the longer useful life there will be. Therefore, when the currency price is stable, mining farms tend to buy the most advanced equipment to eliminate low-efficiency mining machines. It can be seen that as long as the upstream industry can continue to introduce new equipment with higher efficiency, it will receive orders.

The current Break Even point for Bitcoin price and computational power of the entire network

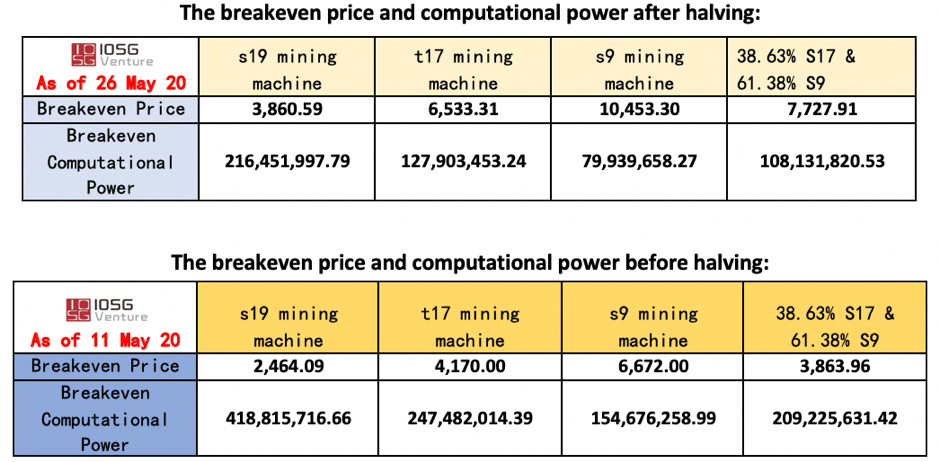

According to Blockware’s research, as far as Bitmain’s mining machines are concerned, the current mining industry is approximately composed of 38.65% s17 and 61.38% s9 mining machines. We compared the current (end of May 2020) breakeven point of the three generations of Bitmain mining machines and the breakeven point on May 11, 2020 (before the halving), and studied the impact of the halving on Bitcoin miners. In addition, we also analyzed the income of miners in different electricity fee intervals:

In the case of an electricity fee of US$0.052 per kWh, we can see that the Bitcoin halving does not have a significant impact on the most advanced s19 mining machine, because as long as the BTC price does not fall below $3,860, s19 will continue to make profits. But for the s9 mining machine, the situation is different. Before the halving, miners will continue to make a profit as long as BTC price does not fall below $6,672. After the halving, BTC price will need to reach US$10,453 to maintain breakeven. According to Blockware’s research, the current mining industry consists of approximately 38.63% of s17 and 61.38% of s9 miners. If we take a weighted average according to this ratio, we can see that the breakeven price before the halving is $3,863, after the halving, it breakeven price changed to $7,272. For all miners to make a profit, the electricity fee needs to be $0.04/kWh and the BTC price needs to be $8,500 and above. For the most advanced s19 mining machine, at the current $0.05-$0.06/kWh average electricity price, it can be profitable as long as the Bitcoin price is $4,500 and above. For the current average mining pool configuration, under the average electricity cost, miners can still make a profit as long as the BTC price is greater than $5,000,. Therefore, we can see the following after the halving:

Old miners (s9) are basically unprofitable, so miners need

- Update their machine

- Continue to sell Bitcoin to maintain operations to the last minute (this kind of miner believes that the price of Bitcoin will continue to rise to more than $10,000)

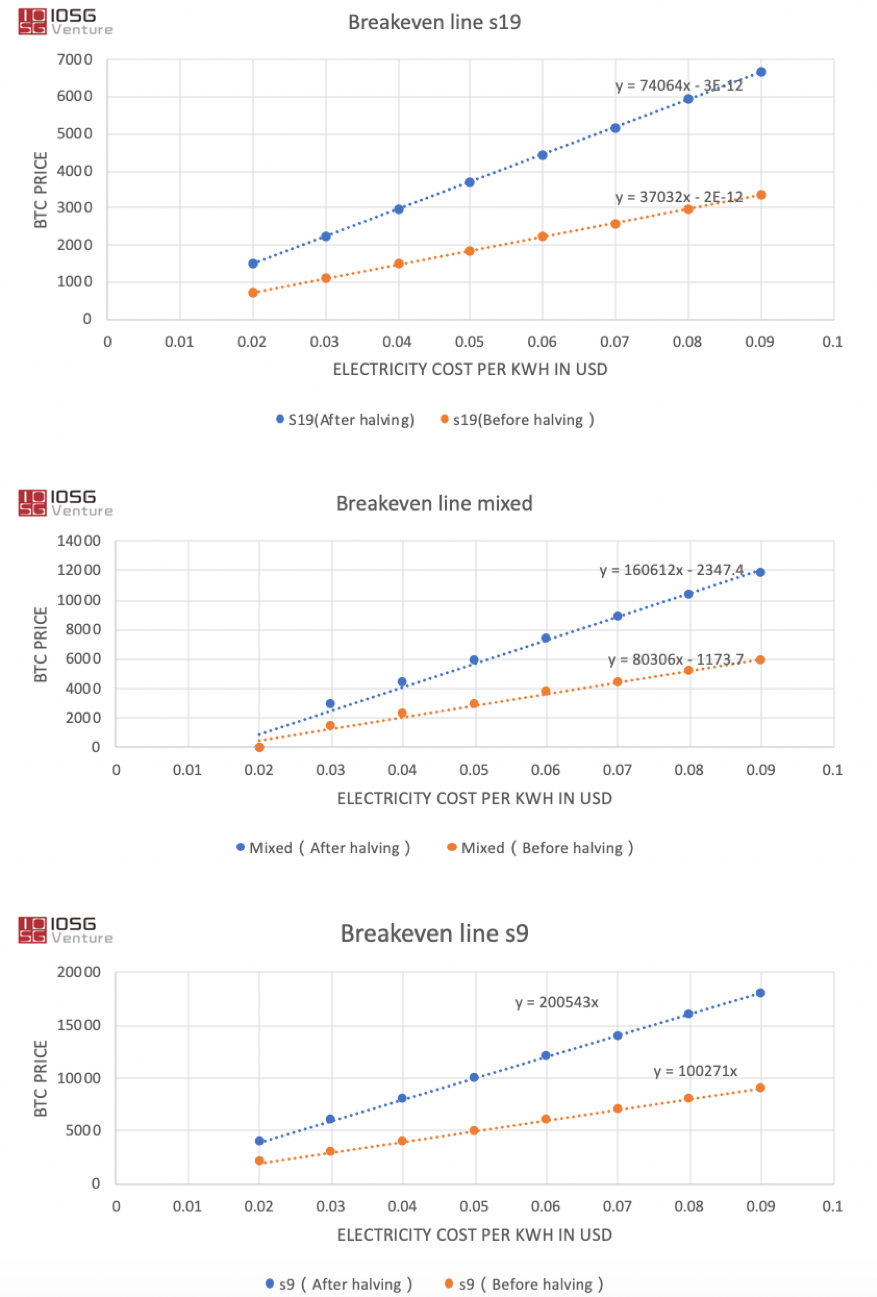

After all the shutdown of old mining machines, the computing power of the entire network will decrease, the profitability of miners will increase, and new miners will enter and start a new cycle. Therefore, the entire mining industry is a self-balancing market, and systematic crises will not cause disaster. By drawing the break-even curve, we can see the BTC prices and electricity cost at different break-even points under the current computing power:

Through profit and loss analysis, we found that:

- After the halving, with the electricity bill and computing power unchanged, miners are demanding higher BTC prices to maintain breakeven. After halving, mining machines (no matter what type) are more sensitive to changes in BTC prices and electricity costs (increasing slope).

- In general, the more advanced the mining machine is, the lower the overall sensitivity to electricity cost and BTC prices (the slope is smaller)

- For large mining pools with advanced mining machines, Bitcoin’s halving will not cause losses.

- With the current electricity fee of $0.05+, the s9 mining machine is no longer profitable, but if it is used with the s17 mining machine, it can be profitable when BTC is more than $7,400.

- Therefore, the timely upgrading of the mining machine after the halving will be one of the key factors to maintain profitability

- The technological innovation of mining machines is the most important factor that determines the future of mining.

Will the halving be the main factor that pushes the BTC price to the top

The current view that Bitcoin halving will cause the price to rise is mainly explained based on the two dimensions of the stock to flow model and the sales pressure of miners.

1. Stock to flow model

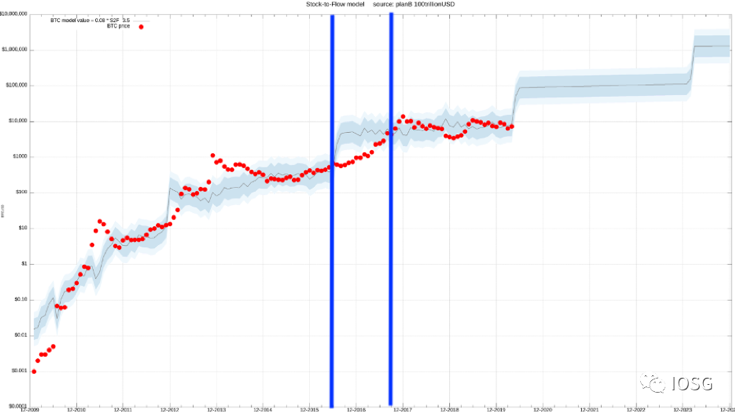

The leading indicator of Stock to flow is the ratio of stock to capacity (stock/annual output). It explains the scarcity of an asset. The larger the s2f, the scarcer the assets (the stock becomes larger and the output becomes smaller). As after the halving of Bitcoin, the reward becomes smaller, and therefore the s2f ratio of Bitcoin will become larger.

The above figure shows the relationship between the valuation of the Bitcoin price through the s2f model and the actual price of Bitcoin. We can see that the actual price of Bitcoin and the model price have a certain degree of correlation, but we think it cannot directly explain that the rise in the price of Bitcoin is caused by the decline in supply:

- This type of model lacks a fundamental basis. The S2F model only considers the relationship between supply and price, and believes that this factor is the main determinant of price**. We do not believe that supply is the dominant factor affecting the price of Bitcoin, because the total circulation of Bitcoin is fixed, no matter how the demand for Bitcoin changes, miners cannot change the supply of Bitcoin. This is very different from gold and other metals. Gold miners can choose to accelerate mining when the price of gold rises. The supply of Bitcoin is inelastic. The basic economic theory tells us that in a market with inelastic supply, the main factor that affects prices is demand, not supply.**

- In addition, even if such a relationship does actually exist, this model does not explain why a sudden drop in supply is an information shock that leads to price fluctuations. Since Bitcoin’s halving is publicly known, based on the efficient market hypothesis, we can know that the impact of the halving has been considered in the current Bitcoin price.

- We saw that the Bitcoin halving last occurred in July 2016. After the halving, the price of Bitcoin did not fully follow the price trend of the s2f model. Bitcoin only reached the model’s forecast at the end of 2017. There is an interval of one and a half years, so we don’t think the s2f model can estimate the price of Bitcoin very well.

2. The selling pressure of BTC miners

The behaviour of miners can be interpreted from the following perspectives:

Miners can only make stable profits when the price of Bitcoin remains at a high level for a long time. Short-term price increases/falls cannot have a huge impact on the entire mining industry.

- Some miners are Bitcoin holders with a large amount of Bitcoin on their hands, so there is no obvious liquidity crisis in the short term. In addition, Bitcoin lending also solves part of the liquidity problem for miners.

- Regardless of how Bitcoin miners choose to participate in mining (connecting computing power to the mining pool/selling computing power to custodians), the upstream mining machine manufacturers remain the monopoly on mining. Therefore, in the bull market, the manufacturers of mining machines will have the pricing power of the mining machines, while in the bear market, the demand for mining machines will also decline. Therefore, the dominator of the mining industry is the mining machine manufacturer.

- In order to fulfill the contract with an electricity supplier, miners may have to operate even they are in a loss.

- In summary, mining machine manufacturers are the dominant players in the mining industry. Bitcoin’s short-term rise and fall will not cause miners to suddenly shut down and stop production. Whether miners continue to participate in mining depends on their ability to resist liquidity crises.

The impact of this halving on miners should follow the below logic:

- Miners increase liquidity in various ways to reduce the impact of Bitcoin halving such as selling Bitcoin.

- Some capable miners will implement the equipment update, whereas small miners may need to continue to sell Bitcoin to maintain operations.

- As efficient miners update their equipment to make their mining capacity more efficient, this will make it more difficult for low-efficiency miners who rely on selling bitcoin to maintain their operations, and will eventually lead to low-efficiency miners withdrawing from the market.

- The remaining high-performance miners will redistribute the computing power of the entire network. The Bitcoin price at the time of the halving is about US$8,800. After the halving, the block rewards obtained by miners are equivalent to the amount when bitcoin price is about $4,400 before the halving. BTC price is between $3900-$5300 on March 12–16. At that time, the hashrate of the whole Bitcoin network dropped from 120EH/s to 95EH/s. We can see that the drop in hashrate here caused the change in difficulty of Bitcoin mining. In the subsequent period, mining difficulty fell from 16.55T to 13.913T.

- After the adjustment of mining difficulty, the surplus of miners remaining in the market will continue to increase, and new miners will have the opportunity to enter, and the miner market will enter a new cycle.

Therefore, we see that the Bitcoin miner market is a self-adjusting equilibrium market. Perhaps the low-efficiency miners still hold a positive attitude, thinking that they can wait until the computation power decreases and the difficulty decreases to make a profit again. However, only when they withdraw from the market, the computing power can then be reduced. Therefore, the market will keep low-efficiency miners under liquidity pressure until they leave the market. At that time, the market computing power will be rebalanced, the difficulty will be readjusted, and the mining market will enter a new cycle.

Since the selling pressure is no longer a variable, a stable factor naturally cannot be a determinant of fluctuating prices.

3. The halving is more of a proof that the Bitcoin mechanism can work as designed

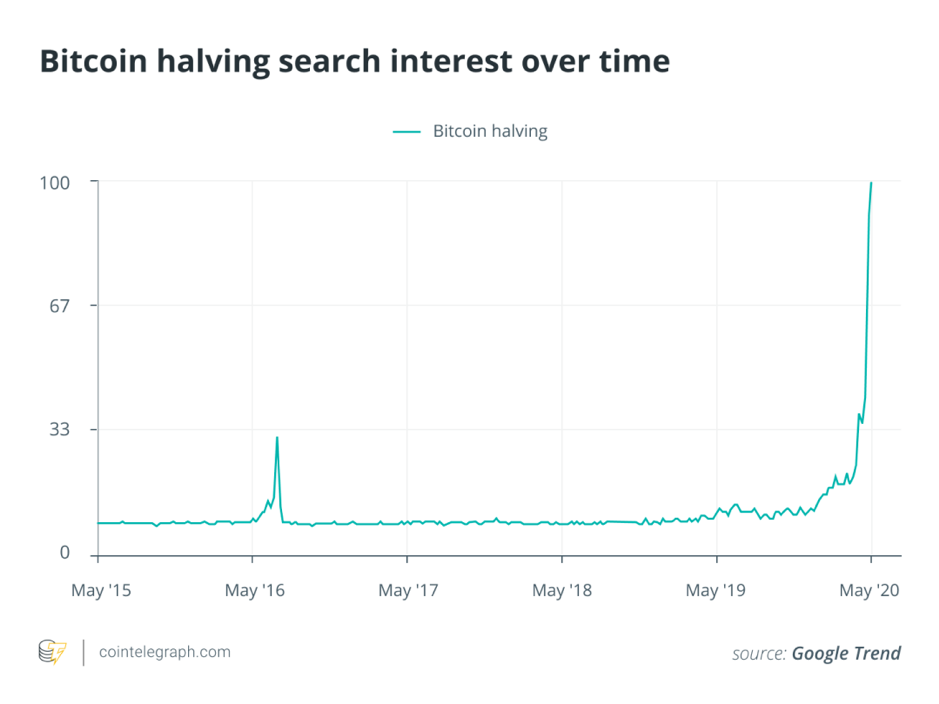

The fundamentals of secondary market prices are still based on the relationship between supply and demand. The net outflows or inflows from the market are the direct factors affecting prices. We can see that the news of Bitcoin’s halving is an absolute hot spot in the industry.

We can see that the search for Bitcoin halving on the Internet has rapidly increased. People’s attention to the event will bring greater net inflows to the market. Therefore, we believe that the main impact of the halving on the price of Bitcoin is:

- It proved that Bitcoin’s mechanism can operate as designed. Bitcoin is indeed a successful cryptocurrency, so it has increased the market’s popularity.

- The increase in market enthusiasm has increased the net inflow of the market, resulting in a short-term price increase.

Where did the bitcoins mined by the miners go?

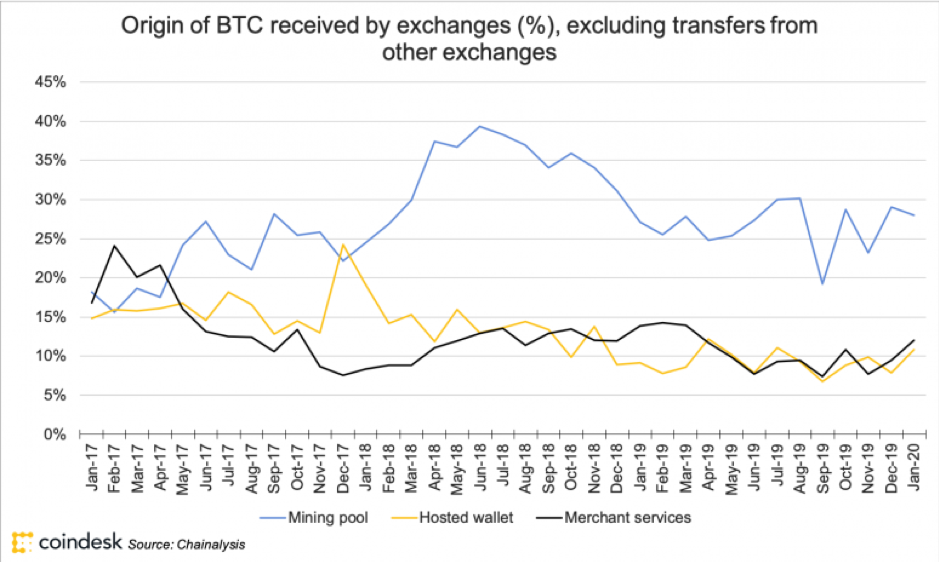

Miners generally sell bitcoin through exchanges. If we analyze the data from January 2017 to January 2020, we can see that more than a quarter of all BTC received by exchanges came from mining pools. Therefore, miners must be extra careful when selling bitcoin rewards, because their actions may lead to a massive sell-off in the market.

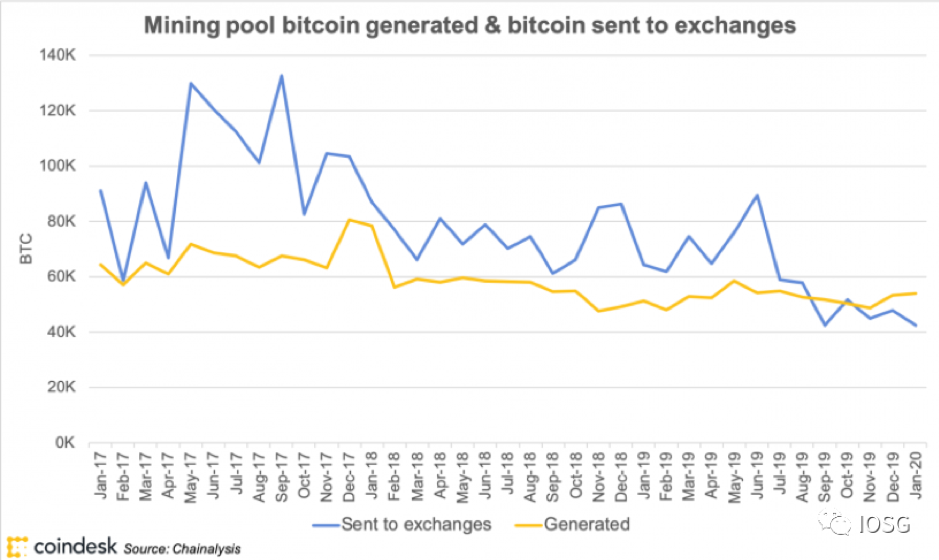

Since bitcoin miners need to sell their bitcoins at the right price in exchange for fiat currency to cover costs, we can know that miners tend to build inventory during bear markets and reduce inventory during bull markets. The following figure also proves this:

Recently, on June 3, 2020, the price of Bitcoin fell by 8% within 5 minutes of the beginning of US trading hours, from $10,137 to $9,298. But the miners continue to sell their bitcoins:

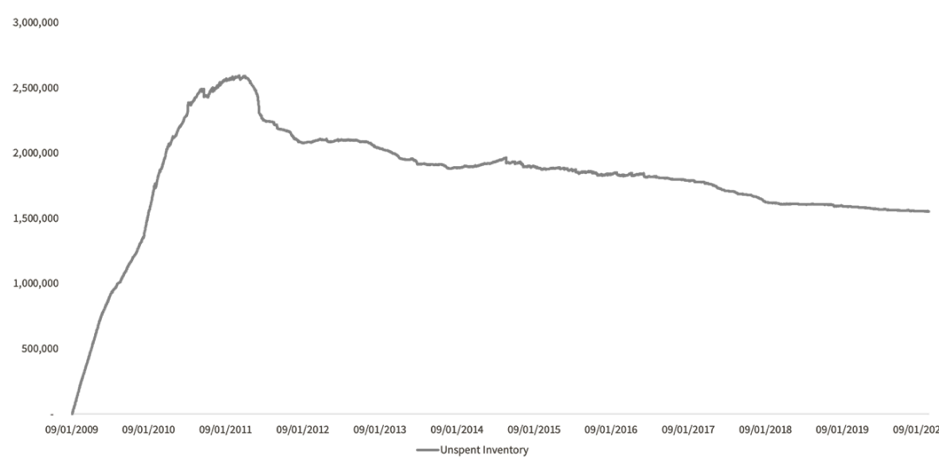

We saw that on June 3 miners mined 844 bitcoins but sold 920 uncolored bitcoins, which caused the MRI index to exceed 100%. This shows that miners believe that the market is still strong and supported, and the sales of uncolored Bitcoin also shows that miners are optimistic about the current market price. If we observe the unsold uncolored bitcoins (January 2009 to January 2020), we will find that the highest inventory of bitcoin miners occurred on March 11, 2011, when there were 2,593,051 Unsold bitcoins. The increase in Bitcoin’s inventory from 2009 to 2010 was mainly due to the fact that it was very easy to mine Bitcoin at that time, and then the Bitcoin inventory began to gradually decline.

Therefore, MRI actually reflects to a certain extent that there are strong quotations in the market that make miners willing to sell their bitcoins.

When the bid is reduced, the MRI will also decrease, and the inventory of uncolored bitcoin will increase. In fact, MRI reflects the demand for Bitcoin, and high MRI reflects the strong market demand to a certain extent. We believe that miners are smart participants. In an equilibrium market, they will consume the BTC inventory when the market is strong.

In summary, mining as a core component of the Bitcoin industry has a greater impact on the early price of Bitcoin**. In the future, they will still be one of the most important players in the Bitcoin ecosystem. However, due to the continuous increase in the market value of Bitcoin, more external factors have an increasing influence on its price**. For example, the secondary market becomes more active. At the same time factors such as increased institutional interest in Bitcoin have laid the foundation for Bitcoin to become a mainstream asset.

Reference

荀玉根. (2017). 港股玩家都有谁:投资者结构、筹码分布. 上海: 海通证券.

秦普岳. (2017年11月30日). 一图看懂主流矿机:ASIC矿机、GPU矿机、CDN矿机与云矿机对比. 检索来源: 金色财经: https://www.jinse.com/news/bitcoin/103580.html

王学恒. (2017年2月20日). 港股专题研究 — 港股波动性认知差异的根源. 检索来源: 格隆汇: https://www.gelonghui.com/p/111125

刘雪峰. (2018). 浅析比特币产业链之二矿场经济学. 上海: 广发证券.

李雪婷. (2018). 2008 年 — 2018 年全球比特币 发展研究报告. 中国: 星球日报研究院.

钱柏均. (2020年05月12日). HashKey:读懂比特币减半后市场供需与矿工博弈,以及本次减半的市场影响. 检索来源: ChainNews: https://www.chainnews.com/articles/572098310069.htm

赤兔咨询. (2019). 比特币价格的秘密. China: 赤兔咨询.

金锄矿业. (2019年12月31日). 矿机的前世今生-史上最全矿机发展史(下). 检索来源: 知乎: https://zhuanlan.zhihu.com/p/100321893

苏宁金融研究院. (2020年03月18日). 黄金下跌背后的原因是什么?. 检索来源: 钛媒体: https://www.tmtpost.com/4274317.html

小吒闲谈区块链. (2020年02月25日). USDT 14天增发1.85亿美元,币圈“印钞机”启动,BTC要王者归来?. 检索来源: 知乎: https://zhuanlan.zhihu.com/p/108955072

链比特LianBit. (2020年03月18日). 比特币到底有没有价值?. 检索来源: 链文: https://www.chainnews.com/articles/180827513681.htm

比推BitpushNews. (2020年03月21日). 比推专访韩锋: 比特币的反弹会是最迅速,最快的,明年牛市一定会到!. 检索来源: 链文: https://www.chainnews.com/articles/695234792404.htm

AlmudhaFahad. (2018). Pricing efficiency of Bitcoin Trusts. APPLIED ECONOMICS LETTERS, 504–508.

AVAN-NOMAYOOSATO. (2019年12月27日). US Bitcoin Derivatives Market, Highlights of 2019. 检索来源: Cointelegraph: https://cointelegraph.com/news/us-bitcoin-derivatives-market-highlights-of-2019

BaekC, & ElbeckM. (2015). Bitcoins as an investment or speculative vehicle? A first look. Applied Economics Letters, 30–34.

BaurDrik G, & HongKiHoon. (2018). Bitcoin: Medium of exchange or speculative assets? Journal of International Financial Markets, Institutions and Money, 177–189.

Bitfinex. (2020年05月10日). What will happen after the Bitcoin halving? 检索来源: Bitfinex: https://blog.bitfinex.com/trading/what-will-happen-after-the-bitcoin-halving/

Bitmex. (2020年June月07日). Perpetual Contracts Guide. 检索来源: Bitmex: https://www.bitmex.com/app/perpetualContractsGuide#Funding-Rate-Calculations

Blockware. (2020年March月31日). Blockware. 检索来源: 矿工与比特币价格: https://mp.weixin.qq.com/s?__biz=MzAwOTk1NjM0NQ==&mid=2247489410&idx=1&sn=3c98e82d8dee02bb98bc40d635792b95&chksm=9b56e914ac2160024eadb9606084120a77f557c16eaafe221e08ff7c031bc12d0b8f65f07b05&mpshare=1&scene=1&srcid=&sharer_sharetime=1585578951062&sharer_sh

Bytetree. (2020年June月07日). Bytetree. 检索来源: Bytetree Terminal: https://terminal.bytetree.com/bitcoin

Cryptomood. (2020年March月12日). How Will The Coronavirus Pandemic Affect Bitcoin? 检索来源: Cryptomood: https://medium.com/@cryptomood/how-will-the-coronavirus-pandemic-affect-bitcoin-9cc35937030e

Cryptozoa. (2020年March月30日). The Bitcoin Virus. 检索来源: Cryptozoa: https://medium.com/cryptozoa/the-bitcoin-virus-37ae50e43040

D’SouzaMatt. (2020年05月02日). 写在第三次减半前:万字解读矿工驱动的比特币价格机制. 检索来源: Blockware Solutions: https://www.blockwaresolutions.com/research-and-publications/hx3hpnbbaxdy2dx8ja3gx9ka648tyk

GeanakoplosJohn, & FostelAna. (2012). Tranching, CDS, and Asset Prices: How Financial Innovation Can Cause Bubbles and Crashes. AMERICAN ECONOMIC JOURNAL: MACROECONOMICS, 190–225.

Gil-AlanaAlberikoLuis. (2019). Cryptocurrencies and stock market indices. Are they related? Research in International Business and Finance.

GodboleOmkar. (2020年June月03日). Miners Are Selling More of Their Bitcoin. That May Actually Be Bullish. 检索来源: Coindesk: https://www.coindesk.com/miners-are-selling-more-of-their-bitcoin-that-may-actually-be-bullish

GodboleOmkar. (2020年Mar月09日). Story from Markets Bitcoin’s Plunge Was Foreshadowed by Miner Inventory Data. 检索来源: Coindesk: https://www.coindesk.com/bitcoins-plunge-was-foreshadowed-by-miner-inventory-data

HayesAdam. (2017). Cryptocurrency value formation: An empirical study leading to a cost of production model for valuing bitcoin. Telematics and Informatics, 1308–1321.

HelfmanMark. (2020). 2020: The Year Wall Street Takes Over Cryptocurrency. 检索来源: Mark Helfman: https://markhelfman.com/2020/02/07/2020-the-year-wall-street-takes-over-cryptocurrency/

HOUGANMATT. (2020). The Bitwise / ETF Trends 2020 Benchmark Survey of Financial Advisor Attitudes Toward Cryptoassets. San Francisco: BITWISE ASSET MANAGEMENT.

JonesPaul. (2020). May 2020 BVI Letter — Macro Outlook. May 2020 BVI Letter.

KöchlingGerrit. (2019). Does the introduction of futures improve the efficiency of Bitcoin? Finance Research Letters, 367–370.

LambMark. (2019年Mar月03日). Physical Delivery vs Cash Settlement (Adoption vs Market Manipulation). 检索来源: Medium: https://medium.com/coinflex-official/physical-delivery-vs-cash-settlement-adoption-vs-market-manipulation-86e8cbd48837

LaVereMichael. (2020年March月18日). High-Risk Leverage and Liquidations Crashed Bitcoin: Report. 检索来源: Crypto Globe: https://www.cryptoglobe.com/latest/2020/03/high-risk-leverage-and-liquidations-crashed-bitcoin-report/

NetworkMetrics’ State ofCoin. (2020). Coin Metrics’ State of Netword. 检索来源: Coin Metrics’ State of Netword: https://coinmetrics.substack.com/

PlanB. (2020年04月18日). Bitcoin Stock-to-Flow Cross Asset Model. 检索来源: Medium: https://medium.com/@100trillionUSD/bitcoin-stock-to-flow-cross-asset-model-50d260feed12

PomplianoAnthony. (2020年03月20日). The Best And Worst Assets Coming Out Of The Corona Financial Crisis. 检索来源: Off The Chain : https://pomp.substack.com/p/the-best-and-worst-assets-coming?token=eyJ1c2VyX2lkIjo3OTQ1MzIwLCJwb3N0X2lkIjozMjIzNDcsImlhdCI6MTU4NDcxODg2NywiaXNzIjoicHViLTEzODMiLCJzdWIiOiJwb3N0LXJlYWN0aW9uIn0.2cpkhPdJ7-Mz6mewBrp7_PtcmcuRFl-t97QM4zYHMvQ

PurdyJack. (2020). Bitcoin Halving 2020 Explained. Messari.

Ryan. (2020年Jan月08日). 比特币会是比黄金更硬的资产?关于价值、稀缺性及S2F. 检索来源: NPC源计划: https://mp.weixin.qq.com/s/eTR6n8shQR46y_YWWvHIqw

SamaniKyle. (2020年03月17日). March 12: The Day Crypto Market Structure Broke (Part 1). 检索来源: Multcoin Capital : https://multicoin.capital/2020/03/17/march-12-the-day-crypto-market-structure-broke/

ShchurDamian. (2020年March月10日). 2020 Predictions — Coronavirus, Stocks and Bitcoin. 检索来源: Data Driven Investors: https://medium.com/datadriveninvestor/2020-predictions-coronavirus-stocks-and-bitcoin-48fe365cd867

SmalesL.A. (2018). Bitcoin as a safe haven: Is it even worth considering? Perth: Elsevier.

TodayBitnews. (2020年03月18日). Cryptocurrencies in Times of Сrisis. Will They Someday Become a Global Safe Haven? 检索来源: Bitnews Today: https://bitnewstoday.com/news/cryptocurrencies-in-times-of-srisis-will-they-someday-become-a-global-safe-haven/

TorpeyKyle. (2020年Jan月15日). Here’s Why Some Financial Advisors Are Adding Bitcoin To Client Portfolios. 检索来源: Forbes: https://www.forbes.com/sites/ktorpey/2020/01/15/heres-why-some-financial-advisors-are-adding-bitcoin-to-client-portfolios/#28f9d4a178a1

ZmudzinskiAdrian. (2020年March月29日). Bitmex research unveils who funds bitcoin network development. 检索来源: Cointelegraph: https://cointelegraph.com/news/bitmex-research-unveils-who-funds-bitcoin-network-development