Author: Ishanee Nagpurkar @ IOSG Ventures

Financializing NFTs was the much-anticipated hype of Q3 — Q4 2021 but its adoption has been on a standstill. While the NFT markets continue to have a good year in 2022 (not as good as 2021), financializing them hasn’t worked as well as previously anticipated. Foundational problems like oracles for NFTs, appraisals and instant liquidity for NFTs are yet to be solved which is base layer to any DeFi protocol.

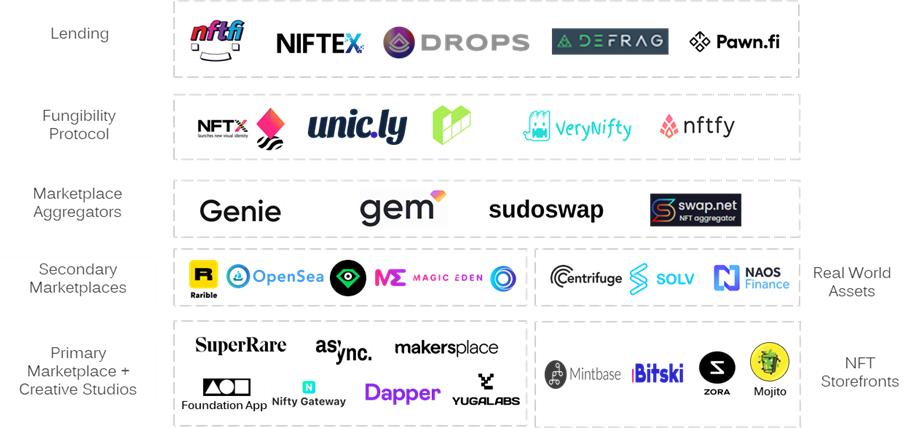

The full infrastructure stack for NFT Fi has grown from primary marketplaces to a full-fledged ecosystem across multiple blockchains (some illustrated below).

NFT-Fi 1.0 waiting for adoption

As the NFT asset class grows, it also possesses risks to its investors. Risk of illiquidity and volatility would be at the top. NFTs are inherently illiquid asset and their denomination in ETH makes them volatile and exposed to currency risks. Investors measure profit/loss in a single method of accounting which is either US Dollar or their local currency.

While it’s difficult to change the denomination of NFTs for the entire industry, NFT enthusiasts were determined to create fungibility protocols such as NFTX, Unicly and Fractional. The mission is to bring in liquidity to these markets; but they ran into liquidity troubles themselves:

- NFTX tracked the price floor of collections which meant their vaults garnered interest from low value NFTs which were being deposited as a “short” against the floor price of the NFT. Majority of NFT investors would not use the protocol unless they wished to speculate on the floor prices of NFTs which were driven by market sentiments and/or prone to floor sweeping.

- Fractional and Unicly provide a more flexible approach and doesn’t require floor price tracking. However, it relies heavily on a large number of investors and whales to speculate on the price of the NFT collection. Acquisition of an entire collection is also difficult (but not impossible!) since it required coordination of deep pocket whales / investors for the collection’s ERC20 holders to make any meaningful exit.

Majority of the assets deposited in the fungibility protocols are also PFPs and are largely considered to be non-productive assets — there is no real reason to borrow NFTs except for vanity.

Productive NFTs

The concept of productive NFTs came forth with the rise of guilds such as YGG and IP rights to collection holders like BAYC.

Royalty backed NFTs

Royalty-backed productive NFTs are still on the rise and the wave will likely be pioneered by Yuga Labs and music NFTs. This is a category of NFTs to watch out for the next couple of months as they earn revenues from commercially licensing the NFTs and distributing the earning back to the collection holders.

Royalty-based NFTs are productive yet unlikely to be borrowed/leased since there is no PoW for holders — royalty will be collected as long as the underlying IP is being licensed commercially. Typically, the deal-making process will be initiated by a creative studios such as Yuga Labs or Recur Forever. As holders, royalties collected are passive incomes.

Gaming NFTs

Gaming NFTs provide a core utility (access to games and rewards)to its holders which subsequently spawned the entire industry of P2E games and guilds. They are unique in that to earn yield, owners must provide a “Proof of Work” which is through playing the game and winning PvP tournaments.

Guilds are asset managers and allocators who buy gaming NFTs in bulk which are then leased out to a group of players (aka scholars) who use the NFTs to play games such as Axie Infinity. The rewards earned in the P2E games are then distributed back to the players, guilds and middlemen called managers.

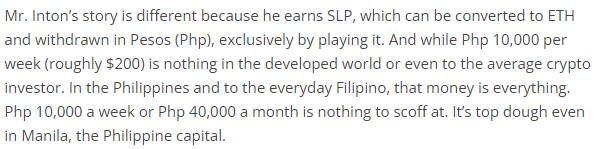

An access issue arises for gaming NFTs where the supply is scarce with an unlimited demand (players). The NFTs also don’t generate passive income — they need to be utilized in the games to earn rewards aka Proof of Work. To make the NFT productive, owners now have an incentive to lend/lease the NFT. Scarcity of supply and earning potential are incentives for players to borrow/lease from the owners. Some players will likely buy directly from the market; but through Axie’ case study, we know that most scholars are not crypto natives. They don’t own ETH to begin with and are primarily motivated by the income earned in $SLP.

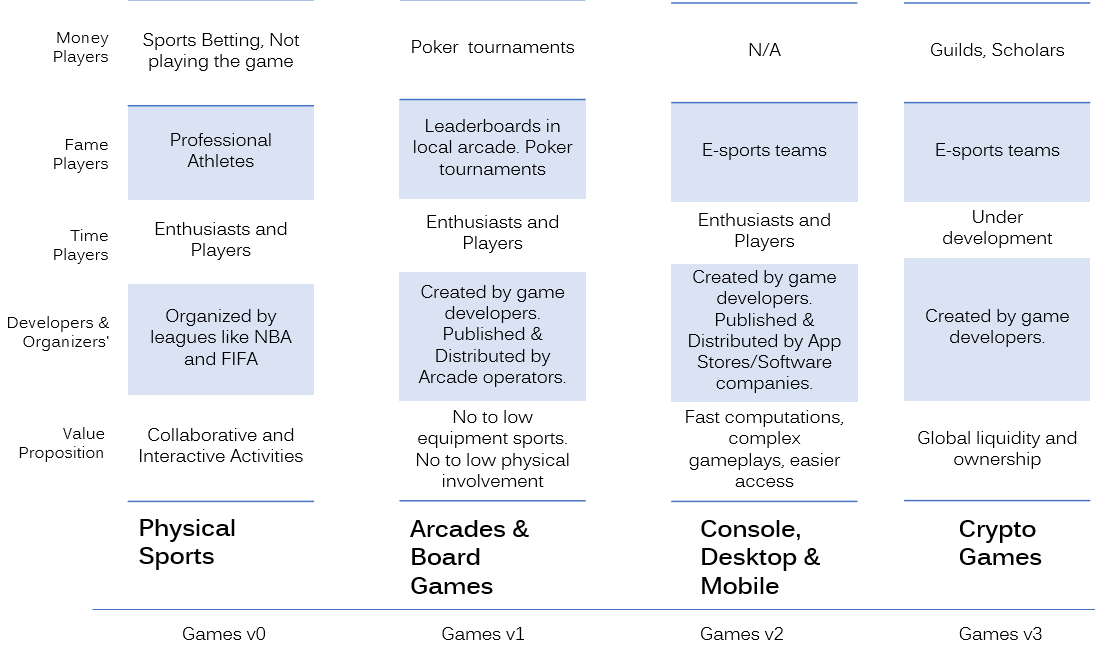

Till date, majority of the crypto game players have been money players. As “play and earn” and guilds become mainstream, it is apparent that more “time” and “fame” players will enter the market. A new group of players will inevitably emerge in the future too — fame players aka esports teams in crypto games who play high stakes PvP games for high token rewards.

As games mature, they will onboard new players. Subsequently, their player compositions will change — skewing away from money players to time players. However, just like in today’s F2P games where majority of revenue is earned by a small percentage of players, the money and fame players will be responsible for trading activities on the marketplace and eligible for in-game rewards via PvP tourneys.

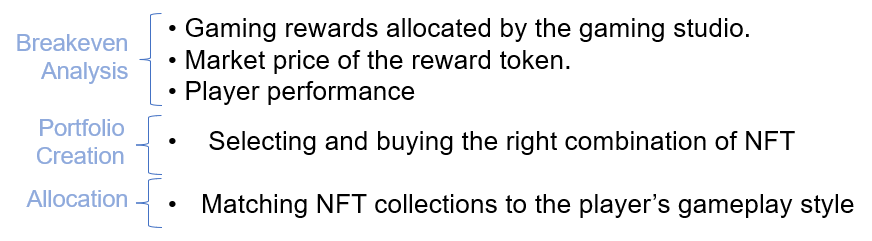

As this happens, guilds and asset owners will need to allocate their premium NFTs to the right players. We expect the decision making process to become more data-driven than it currently is, which is driven by key metrics showcased in the diagram below.

Guild Ops (Centralized)

Centralized avenues for a guild’s operations management has been on the rise. A case study below shows how a guild would manage its Axie assets.

Managers Ronin wallets have with Axies with the ability to natively assign the NFT to Scholars via QR codes. The codes are distributed to scholars. The sub-account can play the game using the NFT but can’t move the underlying asset. They manage frequent pay-days as well where the guild managers manually transfer earnings.

The key problems highlighted here includes

- Excess operational work for managers to manage QR code distribution and paydays.

- Scholars have to trust and rely on managers / guild to pay back their % of earnings on time.

This has inspired guilds and founders to create their own smart contract solutions. Larger guilds such as YGG and Merit Circle will likely create their own customized solutions but micro-guilds (defined as guilds with <100 players) will migrate to general purpose SaaS platforms like GuildFi, GuildOS, 0xAdventure, Blockchain Space, etc.

Assuming data becomes the next key commodity, all guilds will likely want to gain an advantage over the others and will subscribe to means that will track player data (off-chain). Platforms like GuildFi enable this via their Guild ID and Leaderboards — features that are prominently seen in Mobile Games such as Clash of Clans. While centralized platforms are efficient, they require players to have a provable track record or allow platforms to collect required information. Although a common practice in Internet companies, tracking player data to the crypto-native folks might not be a feasible solution.

Path Forward

While the centralized solutions are already a game changer for most guilds, tracking player data and the centralized nature of the services creates single points of failure which becomes crucial when platforms evolve from an SaaS platform into a DeFi hub for NFT lending, leasing, mortgaging solutions.

- Player data once used by guilds for making allocation decisions will be used as credit scores for players who want to borrow ERC20 or NFTs against their future yield as loans / mortgages.

- Leasing out NFTs occurs in a custodial manner and as a result, any hacks or restrictions by the platform on players will lead to loss of funds and assets for the player. This can especially become a high risk situation for players from sanctioned countries.

- Heavy reliance on platforms as exchanges or fiat off-ramps.

Road to decentralization

The hope is that lending, leasing, mortgaging solutions will be available on-chain with minimal human intervention. The exoskeleton for most of these solutions are already being built out and will continue to develop as the entire industry becomes infrastructurally scalable by using L2s and faster L1s.

- As more games embrace on-chain features such as Blockchain Monster Hunt or DeHorizon, most of the player data will be accessible on-chain via Dune, Graph or CyberConnect.

- NFT borrowing and leasing can be accessed using vaults such as ReNFT or IQ protocol. Pegaxy is a game on Polygon which already has in-house lending capabilities eliminating a big need for guilds as asset managers.

- NFT mortgage protocols which allows players and guilds to buy NFTs, use them to play & earn rewards and use the yield generated to repay the debt (Alchemix model).

Let’s deconstruct some of the major challenges that currently stand in the way of DeFi for Guilds / Games:

Third-party NFT lending/leasing protocols

These are solutions such as ReNFT and IQ Protocol who take on the role of the middleman for a small facilitation fee. The P2P leasing/lending protocols will allow asset owners to deposit & lock NFTs in a vault which is then leased out to an interested party in exchange for a small rental fee. The actual NFT never leaves the vault but the playing-rights (utility) of the NFT are forwarded to the renter’ address.

Key challenge to third party protocols is that they require games to integrate with their protocol. The games don’t accrue any material benefit from enabling third parties to do so. Due to the open-source nature of crypto, games can easily spin out their versions of Ronin QR codes / ReNFT’s vaults. Ronin’s recipe for this is currently fully closed source and the key barrier for games to develop their own versions is lack of resources and effort in building auxiliary modules that don’t directly contribute to gameplay.

Some games however like Pegaxy have built this functionality. Technically, they don’t require guilds but continue to work with them to ensure community engagement and as a means of customer acquisition. We can expect more games to continue down this path in the future.

Mortgaging solutions

Mortgaging solutions for gaming NFTs have a unique positioning in the market. As free to play business models continue to prevail, premium NFTs will continue to remain a paid service. Premium NFTs = boosted gaming rewards and hence, guilds and asset owners will continue to buy the NFTs.

Using debt to finance NFT purchases as opposed to cash or revenue sharing models (guilds) will be preferred for fame players aka esports teams. Due to the fact that players have differing play styles, when playing MMO or TCG games, esports teams are sensitive to ownership of their assets. Potential rugpull of these assets by guilds or centralized guild platforms or asset owners on ReNFT is a threat to their income and hence owning these assets make the most sense.

A decentralized mortgaging solution will continue to have several factors that require heavy governance / human oversight and this is due to the nature of NFTs and game economies. Creating smart price oracles for NFTs in different price tiers is an unsolved problem and a bottleneck for all DeFi projects looking to use NFTs in their systems.

Summary

We saw the birth of GameFi and Guilds in 2021. A lot of new primitives, ideas, incentive structures are being experimented with and the space is early but ripe for NFT financialization. GuildFi will likely start with centralized systems until we solve some of the structural problems like price oracles for NFTs, smarter appraisal and analytics and better risk models for the games and their economies. Once these three have been solved for, the industry will start its road to decentralization which might take a few years to see mass retail adoption.

Some things to look out for:

- On-chain game plays

- On-chain player identity systems

- Trustless NFT delegation

- Transparent credit scoring for game players

END