introduction

solana has been five years, of which Jito (the leader of MEV infrastructure on solana) has developed less than three years, but its market share has rapidly grown from the initial 15% to 95% today. It can be said that most of the Meme trading transactions on Solana have to go through him!

The whole process is not wide, please readers set up the bench, click on the collection,Let the 14 Jun depth of the underlying principle, with you gradually revealed:

-

What is Jito-solana? Why can he?Occupy the market in 2 years?

-

Solana compares the differences in the core mechanics of Ethereum.

-

Why do your trades always get clipped?

-

SolanaWhat will the future MEV landscape look like?

1. What is Jito-solana?

Of course, Solana is not only doing mev infrastructure Jito-solana (95% of the market share of the leader), there are other Paladin, Deeznode, BlockRazor, BloxRoute, Galaxy, Nozomi, etc., different entry point manufacturers.

This article will start with the development process and technical principles of the core leaders, and then comment on the advantages and disadvantages of these companies and entry points.

1.1. Jito's development timeline

First, let's take a look at the magic of his market share growth rate with a timeline, pay attention to the pledge rate and related partners.

-

Established at the end of 21

-

Launched on Solana Mainnet in June, 22, there were 200 validators in September of the same year, covering 15% of the pledge volume

-

In '22-23, funding + iteration + in partnership with Solana foundation, Jito client was included in official recommendation

-

After 23 years of TGE, pledge Jito gets MEV income plus, forming pledge repledge mode.

-

Q1 24 Due to strong community opposition, shut down the channel for jito-solana to send transactions to jito-blockengine.

-

Over 500 cooperation validators in Q2 24, covering 70% of Solana MEV, and handling 3 billion transactions in 24 years

-

In Q1 of 25 years, the pledge coverage rate has reached 94.71%. Today, the importance of cross-chain Bridges remains self-evident.

Therefore, it can be said that Jito is the leader of the infrastructure in the MEV ecosystem on solana today, and he has developed in the past three years.

Built a solid solana verifier support base, allowing the vast majority of transactions to pass through jito's system.

It was his system diversion that caused solana's outages to plummet,

He's the one who made the clips profitable,

He is also responsible for solana's validators increasing their MEV revenue by an additional 30%, and steadily.

It is he, from the original dragon slayer to the dragon, and repeatedly jump between the warrior and the dragon, sometimes fierce, sometimes friendly.

In the mainstream Meme narrative of today's market, it has become two hands that eat all the way up and down.

1.2. What kind of system does Jito build?

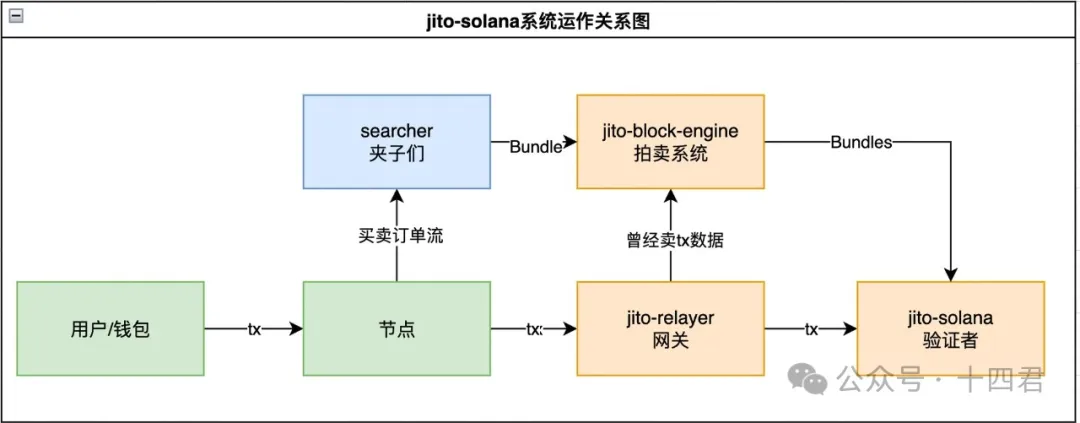

It is actually three core services, block-engine, jito-solana, and jito-relayer. The relationship between them is as follows:

The first is block-engine, which is an auction system.

The typical scenario is to allow the clips to submit less than 5 fixed order transactions through a Bundle consisting of multiple transactions for auction, in which an additional transaction named Tips can be sent to the verifier as an additional tip, so that the verifier is willing to give priority to packaging the Bundle.

Other scenarios are similar to okx, gmgn, bn wallet and other dex platforms, in order to avoid users being clamped, you can separately add tip to the user's transaction, take the auction route, so as to reach the end of the transaction chain faster.

The second is jito-solana, which is a set of clients that replace verifiers to make transactions to verify blocks.

Its core function is to allow the verifier to receive the Bundle package sent by the block-engine, so as to prioritize the construction of this transaction and finally complete the transaction sequence. At its peak, the number of bundles processed per day was up to 2500W (recently 1000W), and each one was almost profitable.

The final TIP fee is paid to the unified account, followed by 95-97% to the verifier, and 3-5% to jito itself.

One of the most controversial is the jito-relayer, which can be understood as a gateway for verifiers to receive transactions.

At first, when the relayer received the transaction, it would delay 200ms and send it to jito-solana, while the synchronous one would send the transaction to block-engine without delay.Obviously, this is selling order data. So the earliest rise of jito is due to this spread of user damage.

It should be noted that in March 24, this rule officially announced that it would no longer transmit data, but to this day, the forwarding switch and the 200ms delay setting item can still be found in jito-relayer.

So, are validators selling user data today? All accompany blockengiThe closed source of ne is not open and unknown.

1.3. How much money does Jito make?

Obviously, the spread between this transaction clip and the non-clip will be accompanied by the introduction of the tips mechanism, and eventually to the verifier, thus causing his market share to rise sharply. Who would turn down 30% more?

Therefore, the total number of bundles initiated in the last year reached 4.3 billion, and the total Tips fees generated reached 5.51 million SOLs, which at the market price of 140 million, accompanied by a total of 7.7 billion dollars of additional revenue for jito infrastructure.

However, not all of this is for the benefit of the Jito system provider, beforeIt is mentioned that there is a 3-5% platform split between jito and validators, so the actual revenue of jito itself is about 20-27W SOL in the past year, which is about $3500W revenue.

That's like two days of King of Glory, isn't it? In fact, it is not necessarily, because this is a real platform revenue after all, in the face of most industries in the web3 field can not say specific revenue.

He has achieved oligopoly, exclusivity of other competitors (after all, the validator can only run one client), and revenue from the recent meme weakness, if the long-term solana more transaction scenarios mining.

Even in the case of no market competitors for a long time, the platform adjusted the share from 3-5% to 30% (this is actually the common platform rate after the Internet application monopolized the market).

Then you can give a very high PE estimate, according to the 30PE of the web2 industry leader, the valuation can reach 1 billion, and according to the common web3 according to the expected monopoly and the potential industry growth of 300 times the valuation, it can reach the level of 10 billion. Similar estimation method reference"Super agent or business wizard? Then look at the year after the cross-chain bridge leader LayerZero went from V1 to V2"

However, we are not here to sort out such a macro conclusion today, nor is it just an imaginary valuation to understand him. I want to go into the details, to understand the deeper principles from which to analyze the future development of the market.

1.4. What requirement scenarios can jito support?

The topic is actually what types of MEV attacks are currently available

The most common is Frontrun, such as:

-

Arbitrage, like Ethereum, moves bricks without risk.

-

Sandwitch Attack, typical sandwich attack. SOL makes about $2 a sandwich.

-

JIT - Just in time liquidity. An operation that provides immediate liquidity.

There is also the Backrun trailing type:

It refers to the insertion of arbitrage trading after the target transaction (such as a large DEX transaction, clearing event), and the use of market fluctuations caused by the target transaction to make profits, the specific scenario is:

-

dex arbitrage: You can think of any trade as a direct spread between different DEXs. Then follow up to close the spread.

-

Liquidation following: After the user's collateral is liquidated, the trailing transaction acquires the asset at a discount and resells it.

-

Predictor delay: The predictor performs a reverse operation based on the outdated price before it updates the price.

In addition to the obvious attack scenario, there are other acceleration scenarios that are suitable for jito,So objectively speaking, jito cannot be said to serve only mev, but for all scenarios with accelerated, bulk transaction bundling needs,

For example, the lively opening activities on Solana, in fact, the dealer will use the Bundle's bundling mechanism and acceleration mechanism to open + deploy chips and other operations.

For example, major exchanges can also avoid being attacked by giving users large transactions bundled tips. But note that none of this actually stops the verifier from doing evil (in fact, you can't tell which verifier is doing evil).

2.Explore the system differences between Solana and ETH

Why is Jito so good for Solana?

Why isn't there a parity of bulls in this market like ETH?

We have to start from the differences between the two systems, you may have heard many times POH consensus, but in fact, Solana's transaction life cycle is different from eth, which also creates a completely different ecology of the two.

2.1 MEV pattern of ETH

Two years ago, on the 1st anniversary of the Ethereum merger, I systematically analyzed:"Ethereum's MEV Landscape One Year after Merger"

It can be clearly seen that the system life cycle of Ethereum is very clear:

This is because after the merger, two very important points for MEV emerged:

1.The Ethereum block interval has become stable. It is no longer a case of relatively discrete random 3-30S before, which is 50/50 for MEV, although Searcher does not need to hurry to see slightly profitable transactions, it is directly sent out, but it can continuously accumulate a better total sequence of transactions, and hand over to the verifier before the block, but also aggravate the competition between Searcher.

2.Miner incentive reduction. It made validators more willing to accept MEV transaction auctions, and made MEV reach 90% market share in a short period of 2-3 months.

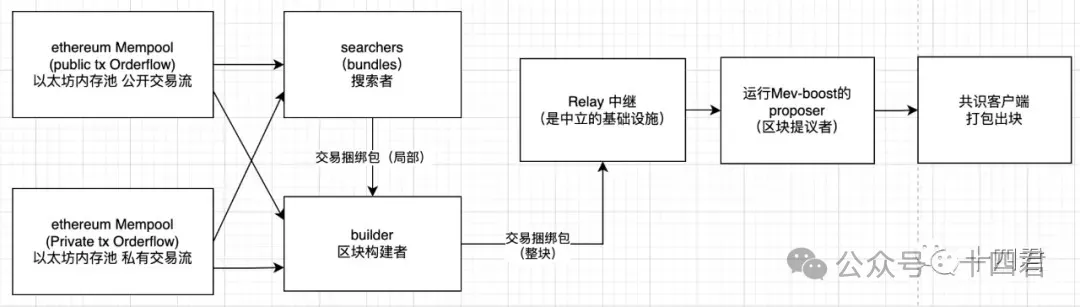

So there are Searcher, Builder, Relay, proposer, Validator roles.

The life cycle of each block is:

-

The builder creates a block by receiving transactions from users, searchers, or other (private or public) order streams

-

The builder submits the block to the relay (i.e. there are multiple builders)

-

The relay verifies the validity of the block and calculates the amount it should pay to the blocker

-

Relay sends transaction sequence packets and yield prices (also auction bids) to blockers in the current slot

-

Blockers evaluate all bids they receive and choose the sequence package that gives them the highest return

-

The blocker sends this signed title back to the relay (i.e., completes the auction)

-

Post-release block rewards are distributed to builders and proposers through intra-block transactions and block rewards.

So, I think,Ethereum's MEV is necessarily a case of high internal competition between Searchers and Builders.

And here's the actual data:The overall rate of return decreased significantly by 62%.

-

In the year prior to the merger, the average profit calculated from MEV-Explore was 22MU/M (started in September 21 and ended before the merger in September 22, numerical merger with Arbitrage and liquidation modes)

-

One year after the merger, the average profit calculated from Eigenphi was 8.3MU/M (starting in December '22 and ending at the end of September' 23, the numerical combination of Arbitrage and Sandwich models).

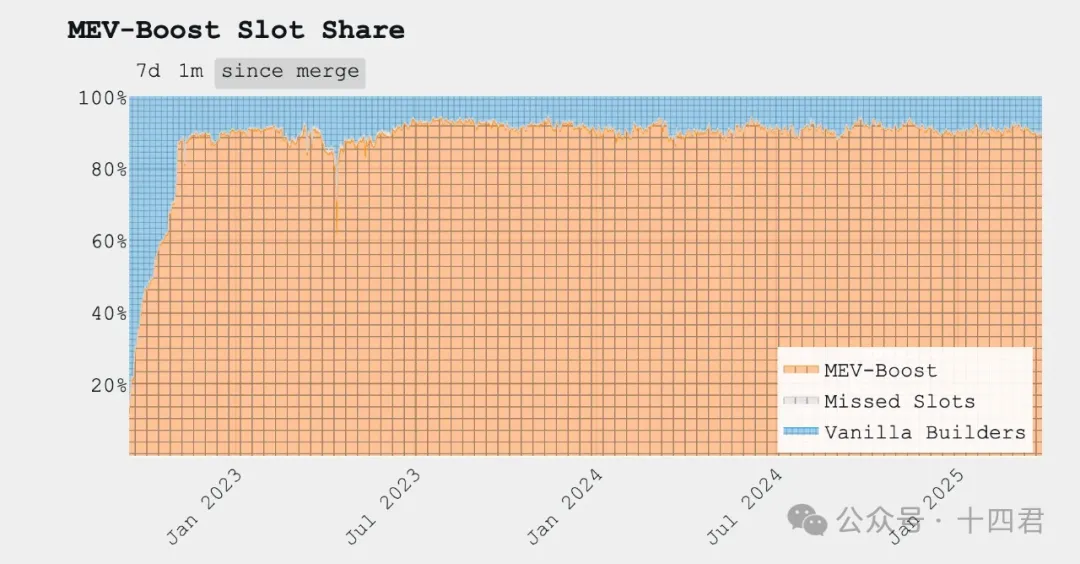

Of course you might think,Isn't MEV-boost faster on ETH? I do!

But fast growth does not mean high profits? We have just analyzed how much profit is, and the rapid growth of Ethereum is rooted in the fact that miners' incentives are reduced, and validators are more willing to accept MEV transaction auctions in order to reach 90% of the market share in a short 2-3 months

And the most difference between ETH and Solana is that there are multiple builders, and their different final revenue affects the decision of the verifier, so the competition between builders is formed.

Because of the competition, searcher's profit is getting smaller and smaller, and because of the competition, the only thing that affects the builder outside of the algorithm is the amount of data.

The searcher that can't compete will exit the market, and the builder that can get a lot of data often has its own infrastructure, and the market voice forms a stable total order flow, rather than relying on the spread of Mempool between nodes.

It all leads to,The MEV market of ETH is actually more market-oriented than a pure oligopolistic platform system such as Solana, which is relatively able to give users a little respite.

2.2. Solana's block mechanism

After understanding the ETH system, please clear your mind, because there are many things in Solana that are different from Ethereum, even traditional blocks are different.

It is these mechanisms that bring about the root cause of rampant mev in Solana systems.

We can use a chart to quickly compare these four core characteristics

among The key lies in the two characteristics of no memory pool and direct connection to the leader. The former brings transaction delays and the latter brings validators to do evil.

2.2.1 Solana does not have a memory pool

The 200ms delay of jito we mentioned earlier, and the synchronous transmission to blockengine, is actually a realization of the memory pool, so objectively speaking, he does not do the memory pool mechanism (this is actually Solana speed up and privacy protection optimization function), how will affect the transaction block mechanism?

If you are an ordinary user, initiate a transaction, to a node, equal to broadcast.

Then in the default configuration, this node will immediately find the current leader and the next leader (a total of 2 validators) and submit your transaction.

And where will the order of trade be? It is important to distinguish between native Solana and jito-solana:

-

Native Solana: After the leader gets the transaction, in theory, whoever comes to my leader first according to FIFO (first-in-first-out) will be included in the transaction sequence. Combined with the mechanism of POH, it is equal to splitting a block into a large number of small ticks for synchronization.

-

Jito-Solana: Normal transactions to the leader have a queue that calculates the current gaslimit (CU in SVM system, compute resource), which has a lower weight than Bundle transactions, so normal transactions are behind Bundle transactions. If it's the same deal, thenJito-Solana prioritizes the deals that attack you. Here he gives 80% to the Bundle and only 20% to the traditional ordinary transaction.

As a result, Solana has no memory pools and simply reduces the number of public passes, rather than eliminating (or possibly eliminating) passes altogether.

This feature, in turn, makes Searcher on Solana the exclusive preserve of high-end gamers.

2.2.2 The subsequent block leader is predictable

The validators will be randomly sampled from 1300 validators in each epoch (approximately 2-3 days), using the VDF algorithm, and will have the effect of pledging weight.

Let's say the total sol amount is 200W, you pledge 20W of sol,So every random chance, you have a 10% chance of being picked.

If it is selected, it is responsible for the next 4 slots (the benchmarking concept of blocks in solana) about 1.6s of time.

This speed is very fast, so any valid node can figure out who the subsequent verifier is, try to link with him, and submit the user's transaction. Due to the network delay, it is easy for the transaction to miss the current leader and be sent to the next leader.

2.2.3 leader's linked strategy also has pledge weighting

namely SWQoSMachine madeAt present, the total capacity of p2p connections of the leader is 2,500, of which 80% (2,000 connections) are reserved for SWQoS (that is, pledged nodes).

The remaining 20% (500 connections) are allocated to transaction messages from non-equity nodes.

It sounds confusing, but in fact it is a new mechanism to prevent spam and enhance Sybil resistance, so that the leader can prioritize the transaction messages broked by other pledge verifiers.

2.3. Why is Solana easy to be attacked?

Even many ordinary users, in order to make their transactions not be caught, think that I can also give high Priority Fees (transaction priority fees, so that miners can package my transactions first? So you don't get caught?

The truth is, a little, but not much, and in extreme cases, the opposite.

From the figure above, we can see that the user actually givesPriority FeesIt's a similarly proportional probability, whereas tips are prone to volatility and competition, and tips are essentially a single transaction, so from the outside, you don't really know which transactions are in the Bundle.

So no matter how high your priority fee is, it is only in the last 20% of the verifier queue to get a block in this slot, but for the Searcher who can find your order in the first place, so as to issue a clip attack on you, with you have a high priceThe Bundle of Priority FeesOn the other hand, the average CU unit price is higher, which naturally gives higher priority to processing in the Bundle consumption queue of the verifier, and broadcasts synchronization.

Similarly, the rest of Solana's mechanisms are fragmented and seem, at first glance, to be In favor of a mechanism that prevents users from being easily clipped, why is the clip on Solana the most rampant? The key points are:

- A leader can never be sure of wrongdoing

There are two ABs before and after the leader, both of which can get all user transactions.So the cost and ambiguity of leaderB's evil is reduced.

As the second leader, I see a profitable transaction, so I quickly build a clip attack to blockengine to auction, and then under the 80%Bundle priority mechanism, naturally my attack will take effect first, but the package is leaderA.

And how do you decide that leaderB was the aggressor?

Of course, you could say that ultimately leaderA packaged the attack transaction, so he was the attacker, but by default, 95% of validators would have done the same thing, so the chance of intervention against them would have been smaller.

In fact, it is unreasonable to punish A, after all, there are other links in the middle, and it may also bring information disclosure, as follows.

- Transaction retry, dwell time is long

Obviously each slot is only a mere 400ms, but have you ever traded on Solana inexplicably stay more than 23s experience?

You may be jumping to the conclusion that the node you are linking to is not performing well, but it is not.

Because of the Swqos mechanism, if you link to an ordinary node, then he calculates to find the leader, to submit transactions, but when the network is crowded,He only has 500 connection pools for normal nodesOnce the link fails to commit, it will retry all transactions of the node for 2s.

The above parameters are the underlying default parameters of Solana nodes. Different nodes can have different Settings (for example, 1s retry).

For the average user, how can the probability of encountering a retry be measured?

As of March 2019, solana currently has about 1300 verifiers and 4000 RPC nodes.

Once crowded, 2700 nodes compete for 500 link pools in 1.6s (4 slots). If the space of the leader is not crowded, it will continue to find the next one.

So under the illusion. How will your transactions be treated if they are stuck in nodes for a long time? If your CU price is not high enough, and the leader is full, and he sees the deal, what should he do?

Yes, selling data, for high-traffic nodes, some Searchers will buy the order flow at the price of $1W a month.

- meme narration and pledge to increase income scale

First of all, meme market stage, because the current mainstream narrative of Solana is Meme ecology, so the pool on the chain is very shallow, resulting in the user easy to trade the slip point needs to be set relatively loose to make a transaction, which also magnify the searcher's attack revenue (so far, we have sampled several, all of which can reach $2 in revenue. Compared to eth, the return of almost $0.1 is very high.)

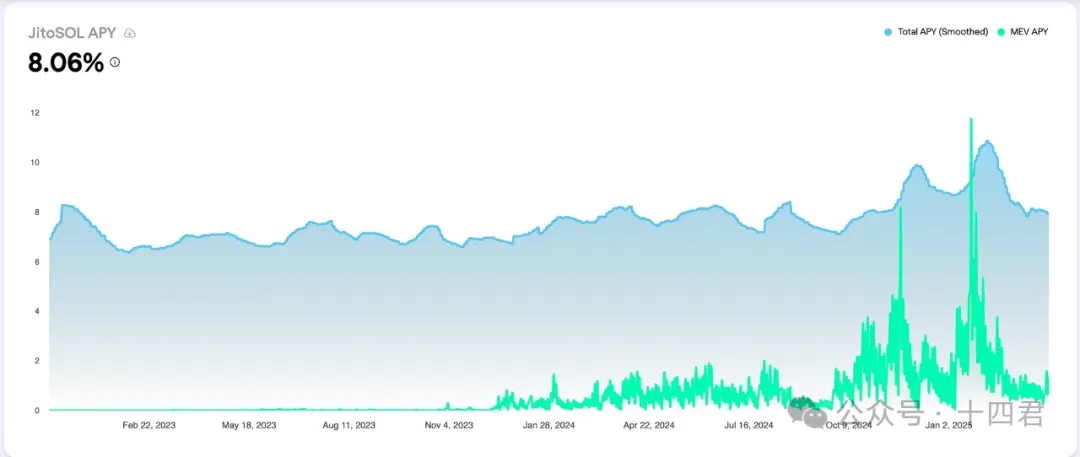

The second is Solana's verifier pledge income, which is about 8% annualized, a relatively stable value over the years.

The annualized return of mev enhancement is about 1.5%.

The combination of the two, equal to the pledgor to run an additional jito-solana client, can increase the pledge yield by an additional 15-30%. In local cases, when the market explodes, even the mev yield can exceed the pledge yield itself.

2.4. Why are Solana's verifiers prone to defection?

The profit is too high, and the cost is also very high, forcing the verifier to continue to expand the source of revenue.

Approx. 300-350 SOL voting cost per year for verifiers ($42,000 at $140 market price) and $4200 hardware cost (not including the cost of dynamic networks)

Solana's huge node configuration burden requires node performance of at least 24 cores, 256GB memory, 2*1.9TBNVME.

The common custom Latitude model on the market, currently used by 14% of validators, costs $350 a month.

As a result, only 458 of Solana's 1,323 validators were profitable. This is why the "SIMD-0228 proposal" was voted down.

As a result, the proposal would further reduce the block incentive, which would inevitably force smaller validators to quit. And even lead to the irreversible transformation of the platform's centralization. And what do you think will happen when the mev share goes up and the essential work share goes down?

Let's take a look at their strategy from competitors other than the Jito

3.Other MEV competitors on Solana

3.1 Paladin: Do VIP jump start and transaction protection

Current market share: 5%, launched at the end of 2023, with 205 officially claimed as of March 2025Verifier nodeDeploy Paladin, pledge 53M of SOL, Using the Paladin client can increase node revenue by approximately 12.5%.

In fact, it is essentially based on a forked modified version of the Jito-Solana client.

The core selling point of the launch is

-

P3 Priority port:Relinquish the block leaderOpen this fast VIP channel and re-process according to the rules of the original FIFO.

-

Identify and exclude clip attacks: While this initially seems to work against verifier rewards, Paladin validators are compensated through trust-based mechanisms. Validators that avoid the "sandwich" can attract direct transactions, creating a trust ecosystem and boosting earnings.

-

Paladin BotThis is an open source high-frequency arbitrage robot that runs directly on the verifier node and only starts when that node is elected Leader. When the Leader owns the Paladin Bot, it doesQuickly execute a simple and risk-free MEV strategy(such as pin-to-pair DEX spread arbitrage, centralized exchange and on-chain spread arbitrage, etc.), and the profits are directly included in the verifier's income

By December 3, 24, the last bot has been officially deleted.

3.2. bloXroute: Network layer optimization + private channel guarantee

bloXroute Labs is an infrastructure company that provides a blockchain data distribution network (BDN) that has previously accelerated transaction broadcasting and reduced latency on chains such as Ethereum.

bloXroute is not directly involved in MEV allocation, but by providing faster channels, it can helpJump start tradingGet to the Leader faster.

Unlike Jito/Paladin, bloXroute does not directly modify the Solana authentication client or introduce a transaction auction mechanism, but is available to all nodes at the network layerFaster message channels.

The main idea is to relay Solana's block "shred" (fragments) to all verifiers more quickly through a global network of accelerated nodes, reducing the delay of data broadcast when the Leader sends out blocks and the fork caused by poor network. So the services provided are:

-

Solana BDN AccelerationAccording to the official documentation, bloXroute Solana BDN can reduce block fragmentation propagation latency30-50 milliseconds

-

MEV-Protect RPC Service, similar to Ethereum's protected private transaction port, which indicates that bloXroute plans to allow users to send transactions privately to the Leader through its RPC to avoid being seen by third parties, thus preventing a jump or jump start.

3.3 BlockRazor: Network layer optimization + private channel protection

BlockRazor is a newly established MEV infrastructure project in 2024, and the team behind it is mainly from Asia. It is positioned as an "intent-centric network service provider" that it plans to offer on mainstream blockchainsMEV Protect RPC, high performance network acceleration, MEV BuilderScheduling service

Scutum MEV Protect RPCThis is a private transaction gateway service launched by BlockRazor, similar to Flashbots Protect. Users can submit transaction bundles through Scutum RPC,

BlockRazor ensures that these transactions are not published through a public mempool, and are sent directly to the block producers to avoid being rushed or sandwiches

4. Summary

4.1. How do you view the MEV competitive landscape on Solana?

Just the day before yesterday, a new contender entered

Warlock Labs raised $8 million on March 27, 2025, with the aim of reshaping on-chain order flow.

However, he focused on Ethereum's track, planning to ensure that order flow data is accurate and responsible for processing users' transactions by further providing some kind of proof and on-chain registration.

This is my point:A really good market will constantly have new competitors enter, but an oligarchic market will bring challengers blocked, and what kind of market does the platform layer expect to become?

Let's think about it a little bit more,What really matters in this mev infrastructure?

Paladin is built on Jito-Solana, which means that, in fact, jito can upgrade a version, no longer support the so-called P3 channel, similar to the 3Q war of the year, and finally who is more just need (obviously social) who won, the same also happened in wechat to prohibit NetEase cloud music and other friend circle sharing, If it were not for the existence of a larger layer of rules machine, this exclusive competition strategy could be applied to any track indefinitely. And today's 5% market share of paladin is also because of the early use of built-in bots to improve the profits of validators, although his open source bot is only around the non-aggressive (that is, do bricks and not make sandwiches and other types of obvious damage to user interests), but it is still forced down by market public opinion.

In addition, several other competitors, bloXroute and BlockRazor, are taking the accelerated + privacy channel route, the so-called privacy, the limit is to give the leader only the current one, so as to avoid the next one to do evil, and face the evil direct attack on both sides.

And the ability to accelerate is indeed today's real technological hard power. It is also the focus of the next wallet /Dex market battle.

Objectively speaking, the original client code of Solana is still written with some historical debt, so people have jumped out and changed the client, so that the configuration is low and the synchronization is fast, and in addition, combined with the mechanism of Swqos, in fact, the verifier can also improve the link stability and success rate.

In addition, jito's blockengine system is actually a multi-center system, but then multi-center (not completely decentralized), there will be a single point of failure, because he is the core link of the upstream, so once down, it is about equal to Solana down.

Therefore, in order to achieve multi-node disaster recovery acceleration, it is still necessary to go through the system that has been Ming Wen a wave of pressure test challenges, which is why the bugs of the Binance wallet will appear more, and many historical technology has not been completed.

But the hard power of technology is something that will eventually be solved.

In the end, whichever continent the leader is located in, he will establish the shortest channel, so that his transactions can reach the leader quickly, and he can also establish a multicast strategy to divert different user needs. The future competition will inevitably be the result of fine operation.

But what can not be solved is the problem of market competition crowding out.

If jito-solana takes advantage of the oligarchy and changes the bundle-first strategy from 80% to 90% to 95%, the average user will have to raise Priority Fees indefinitely to compete for the missing 5%CU space.

But in fact, when the total CU is underutilized, it will eventually affect the total revenue of the verifier (and because a large number of transactions are accumulated in the unprocessed queue, the verifier has a stronger incentive to do evil), so Jito will not start such a competitive mode until it is a last resort.

So why is the ETH market more open to competition? And Solana's competition is more exclusive?

The author believes that the root cause is the lack of Builder bidding role.

ETH can generate multiple final block sequences from multiple builders, and the verifier is to verify and select which one.

However, Solana only has multiple blockengines (and they are all his own), and the transaction queue he sends to the verifiers is actually a single Bundle (5 transactions), which eliminates much of the Builder competition.

Objectively speaking, from the development of ETH, it can be seen that this competition will significantly expand the benefits of the verifier, and reduce the benefits of Searcher, when the Searcher's benefits are reduced, the attack will also be reduced, and finally achieve a balance.

In the future where technology and market are balanced, what is the real competitiveness?

At this point, the author believes that when the technology gap is smoothed out along with talent competition and investment, when the market is centralized and decentralized and ultimately affects the overall SOL ecology, it will be solved. Now Solana has opened the discussion of multi-Builder, and even further opened the discussion of the solution of further random block production by multi-leader.

Although multi-leader also means that more people will get your order, since the final blocker is a random one of multiple simultaneous queues, the competition of multiple builders is also realized in disguised form, and the market impact will be the same as the previous route.

True competitiveness, then, will shift to the data silos of order flow.

jupiter, for example, has occupied more than 80% of the dex market share, then his order flow is the biggest cake, depending on how he weighs whether to provide the best price, or take a random point of "lucky goose" to obtain profits, even if the loss of brand reputation.

Here I think the reason why they do not end up doing their own mev infrastructure, I am afraid that in the face of the developing market stage, who can not say that they are as big as the traditional factory, so this time to focus on profit will give competitors the opportunity to overtake.

And mev is always a problem of game theory, once it reaches a monopoly position, then the monopoly relies on the support of validators, who will push the facility to give profits.

Any dragon slayer has the seemingly unstoppable potential to become a dragon, and a combination of dragon and warrior.

Of course you might say,How could jito be a dragon slayer when it was the infrastructure that was going to MEV in the first place?

4.2. What is Jito's contribution to Solana?

A lot of the previous, are jito over, then jito is helpful?

Objectively speaking, jito works.

When I first started watching Solana three years ago, I was dissing it at the time (OK, I was too loud), but the root cause of this analysis was that it had too much downtime.

Then why is there such a high rate of downtime?

On the one hand, there were too many holes in the early code, and it was later found that paying money would solve most of the problems (the machine configuration kept getting higher and higher).

On the other hand, it is the strategy of FiFo, when there is a highly profitable transaction on the chain, even if it is only in the form of backrun attacks, then who follows the most recent, then the higher the profit of the transaction.

Obviously, each Searcher would build a facility to send the fastest transactions to the leader, so early leaders were always subject to flooding.

And the emergence of blockengine, jito further produced a bidding link, you see the profit, then you go to auction to sell, here the flow is diverted.

There is also a function of blocking failed transactions here, because if your transaction is in conflict with someone else's, and someone else's price is higher, then because the two Searchers are the same person's transaction, then it must be stored in conflict, so if you bid, then blockengine will give you a direct rejection. Then you raise the price again and continue the auction (he may also randomly refuse you, so that you mistakenly think that you must further bid, well, big data kill more kind).

Of course, you ask, why are we still seeing so many failed deals on Solana?

Of course, because blockengine is multi-center, between different centers, 400ms such a fast block speed, so that he can not do fast data synchronization, so as to exclude the auction error situation generated between different blockengines.

Therefore, I think jito is also responsible, after all, he has made Solana's downtime significantly reduced.

In addition to downtime, his bundled trading has also allowed the market to have a variety of application scenarios.

In order for a market to thrive, in fact, it needs to serve market makers to do things well. Solana's most explosive market is Meme market, which is inseparable from the opening group, who need to "cryptically" collect low-price chips at the same time of launch. This is a highly sniper scene, if the operator of the plate cannot collect enough low-price chips with profits, Then he may simply abandon the pull and directly reopen.

In fact, it is both disadvantageous, after all, he himself has made a blind bid.

And there are other needs to accelerate transactions, such as various dex, now also more trust that jito-solana will not be as blatant as before to sell data, so for high-value transactions, users will give an extra tips fee, take the blockengine fast route, directly occupy 80% of the CU processing queue. Thus improve the transaction speed and avoid being caught.

Improve Solana pledgeers' returns and increase the overall degree of decentralization

The previous data has been analyzed, Solana itself pledge income is about 8% annualized, and through jito's mevtip income, it can reach about 10%, which is a good space.

andOnly 458 of Solana's 1,323 validators are profitableOthers are not completely unprofitable (otherwise, who would do it), and others are either directly evil, indirectly evil, or have no motive to make money (for example, just to speed up Swqos). In essence, the appeal count is based on pledged proceeds rather than fully incorporated mev proceeds.

So it's also because of jito that the remaining 800 validators are profitable and today's Solana is less centralized.

Therefore, overall, jito-solana still has merit, at least for now he has not completely adopted exclusive competitive strategy, at this time, there are still opportunities for third parties to cut in.

4.3 How will the MEV pattern develop in the future?

The author has mentioned a number of key points before, I think that now seems to be a unique super strong, but it is actually an opportunity to lurk.

First, because the MEV profit on Solana is generally higher (about 2U, better than about 0.1U of ETH), the wind of meme will accompany different narrative scenes and the transaction will be eternal, so there will still be new Searchers entering, although the high acquisition cost of order flow on Solana blocks some small players. But competition among the big players also increases investment along with profits.

Second, there is a lot of opposition on Solana to the MEV infrastructure. This forced jito to announce that it was shutting down the way it sold data, and forced paladin to remove the built-in bot's functionality. In this category, simd-228, there is also simd-96, which has been adopted.

Half of the original base fee+Priority Fees in the rewards received by the verifier will be destroyed.Now only half of the base Fee is destroyed. This in turn increases the verifier's revenue from packaging normal user transactions, thereby increasing their incentive to fight jito's de-weighting of normal transactions. There are constantly new proposals to participate in Solana's macro decision-making game.

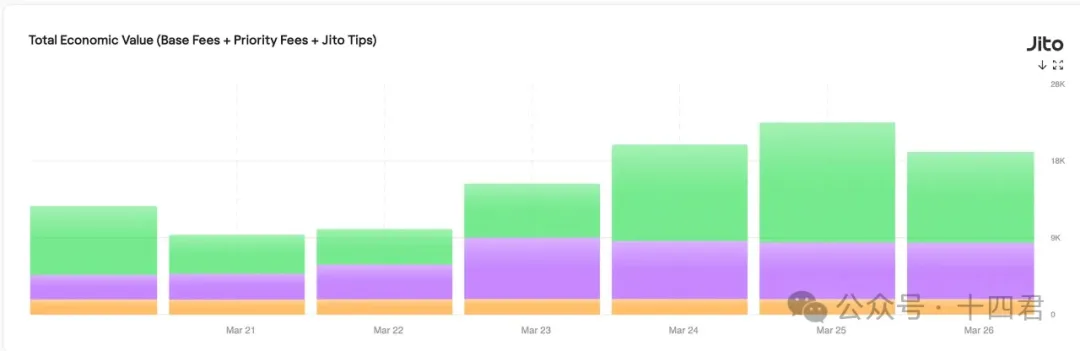

Third, mev's overall profit margins are large enough, such as last year, Jito Labs' October fee revenue of $78.92 million, double the record of $39.45 million set in May.It is higher than established DeFi protocols such as Lido and Uniswap. Here, even if jito itself wants to pay dividends with the verifier, the overall spread is the lower limit of the user's loss scale.

How much loss there is, how much power there is, and users' expectations for reliable service can also be quantified. The BlockRazor and bloXroute opportunities.

Also,What I'm also looking forward to are some more cutting-edge explorations:

-

Starting from the privacy transaction: Threshold Encryption, Delayed Encryption and SGX encryption, basically from the encryption of transaction information, decryption conditions are required, or time lock or multi-signature or trusted hardware mode

-

Starting from fair trade: there are fair order FSS and order stream Auction MEV Auction and MEV-share, MEV-blocker, etc., the difference is from no profit at all to sharing profit to weighing profit, that is, it is up to the user to decide what cost to obtain the relative fairness of the transaction.

-

At present, PBS is actually a proposal of the Ethereum Foundation, but the implementation has reached a separation with MEV-boost, and in the future, the core mechanism will be converted to the protocol mechanism of Ethereum itself.

Most of these have been proposed in Ethereum itself, but their compatibility differences have not yet surfaced in the user's vision, but these are also places where Solana itself can learn from.

5. Write at the end

The end of the competition is often not surpassed by the efforts of the same track,It won't be the next jito who kills jito.It's a completely new form of application.

In a previous study,[UniswapX Protocol Interpretation]Summarizing UniswapX's operating processes and profit sources, he wanted to fully characterize MEV's specific rate of return, after all, that is what he is fighting and paying dividends to users (essentially losing the real-time value of the transaction in exchange for a better exchange price).

Then the order book form of exchanges (even decentralized exchanges) are also a good tool to fight against MEV, you can think of when the future computing power is further improved, daily transactions are further expanded, then the AMM mechanism and the corresponding MEV attack derived from the largest attack scenario, will disappear. But there are other challenges to the order book that are no less problematic than MEV.

As can be seen from the recent twists and turns of hyperliquid, putting aside the hidden worries of centralization, on the way to the compliance control of web3 as a whole, players on the table have changed into suits and entered the international hall.

At this time, compliance is a full range of swords, after all, at this time, he stands on the side of the user.

This article is thousands of words in scale, logic and data can not be separated from the following articles, thank you for the research provided for the development of the industry!

Original link:Click details

Reference document:

https://dune.com/queries/3272756/5525700

https://www.helius.dev/blog/solana-mev-an-introduction

https://www.helius.dev/blog/solana-mev-report

ttps://solana.com/docs/core/pda

https://cogentcrypto.io/ValidatorProfitCalculator

https://solanabeach.io/validators

https://medium.com/taipei-ethereum-meetup/after-the-merge-mev-309e836698cf

Background message author, discuss web3 industry issues

Like attention, fourteen with technical perspective to bring you value

Weekly more bloggers, recommend adding stars to reduce the omission of the latest original views!