Author: @CryptoScott_ETH | @RealResearchDAO

Foreword

The speculative nature of the cryptocurrency market is extremely strong, and users who participate in crypto investment have a high risk appetite. Therefore, we can see that the trading volume of leveraged trading products on centralized exchanges is much larger than the spot trading volume. The outbreak of DeFi summer has caused some spot transactions to be migrated to on-chain decentralized exchanges, so that people who are also looking forward to leveraged trading can participate in decentralized exchanges. Last year was the first year of the outbreak of the new alt public chains. The gas fees of these new public chains were much cheaper than Ethereum mainnet, which greatly reduced the cost of leveraged transactions and provided the basis for the outbreak of leveraged trading on-chain. However, the on-chain leveraged trading did not explode on a large scale like the spot trading in DeFi summer last year, mainly due to

- insufficient liquidity to support large-volume transactions, making it difficult for institutions to intervene, mainly in the retail market;

- The spot trading volume in DEXs is composed of the long-tail demand of various small currencies. They have a high price fluctuation and are thus not suitable for leveraged trading. Therefore, leveraged trading lacks the need for long-tail trading;

- The new public chains are more centralized. For blue-chip pegged assets such as BTC and ETH, there is a certain risk of capital security when cross-chain trading on the new public chains.

Optimism has recently seized the market share of Layer 2 protocols by launching their tokens, which has further stimulated the rush of token issuance of Layer 2 protocols. With token incentives, the liquidity of the entire Layer 2 protocols will be improved. At the same time, it’s worth noting that Layer 2 protocols are more secure than other new public chains. Therefore, the rush of token issuance of the L2 protocols is expected to trigger the outbreak of on-chain leveraged trading. This article evaluates the investment value of GMX by comparing three well-known L2 leveraged trading protocols, DYDX, Perpetual Protocol, and GMX.

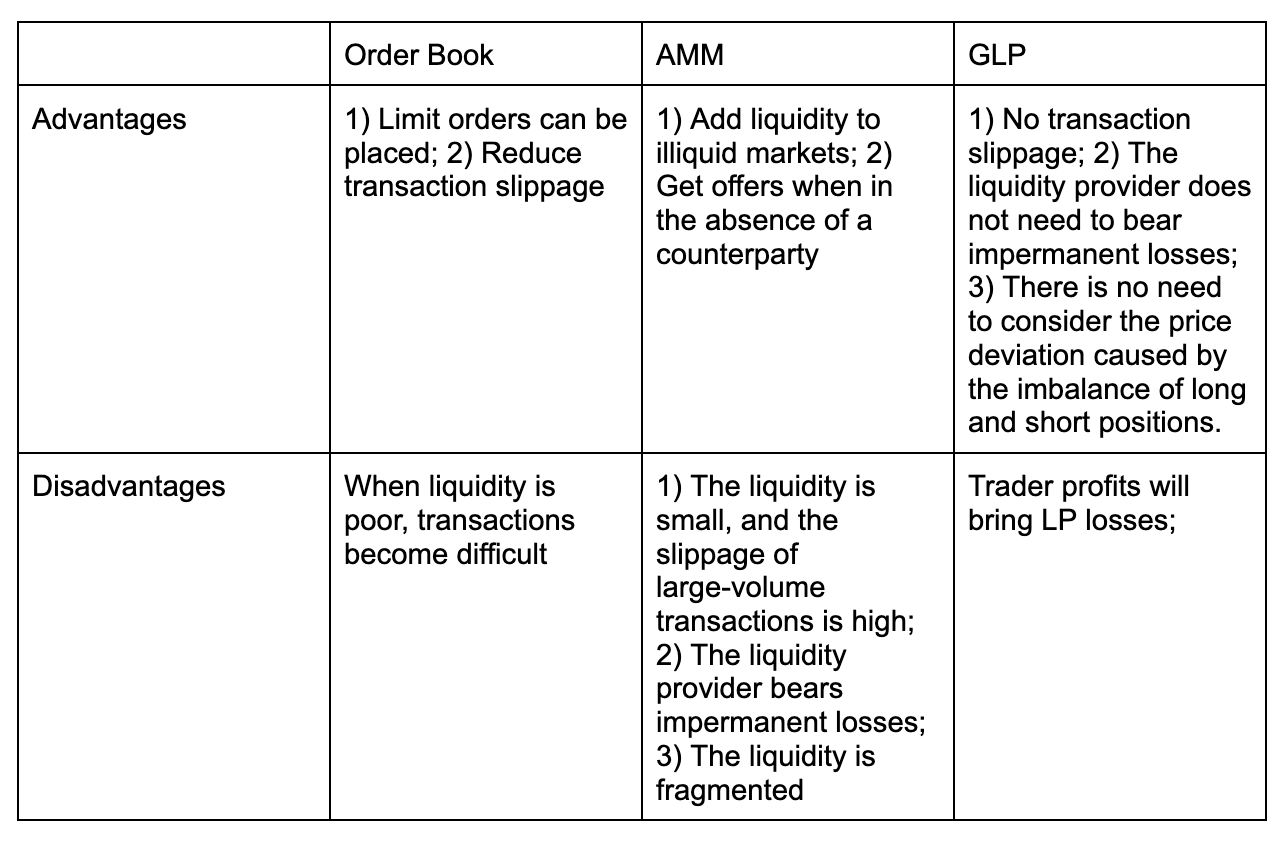

How to achieve leveraged trading?

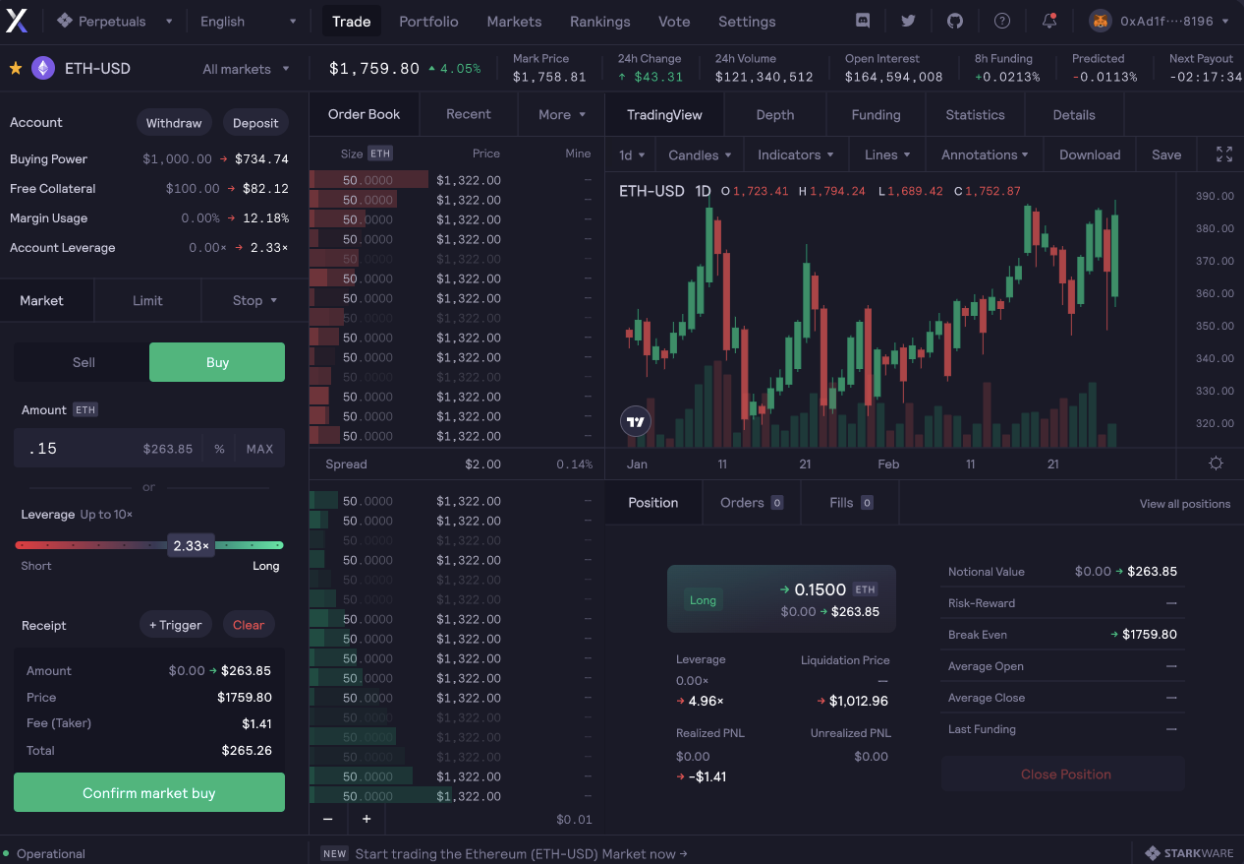

Semi-decentralized Order Book Model - DYDX

DYDX is a leveraged trading platform built on the Layer 2 protocol called StarkEx. It uses an order book model for trading, so the trading experience is almost the same as CEX, and the funding fee mechanism is used to balance naked positions. The entire transaction process is executed off-chain without going on-chain, and only goes on chain when the funds are transferred in and out of the margin account. DYDX has introduced professional market makers to enhance their liquidity. The entire transaction process is a three-party game process between market makers, long traders, and short traders.

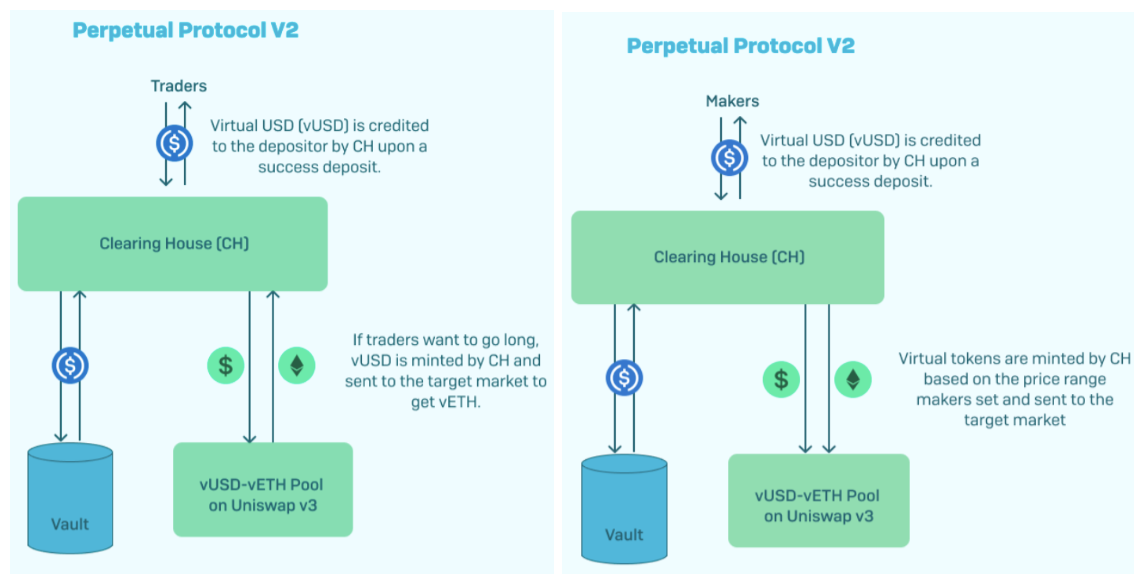

vAMM/AMM Model - Perpetual Protocol

Perpetual protocol is a decentralized perpetual trading protocol built on Optimism. In their V1 version, the transaction process uses virtual AMM (vAMM) for pricing. The virtual AMM refers to the x * y = k model of AMM. The vAMM does not store real assets, but it is convenient for liquidation. When trading, virtual assets are minted in vAMM. If you open a long position with 10x leverage at 100 USDC, 1000 vUSDC will be minted and put into vAMM. A funding fee mechanism is used to balance naked positions. Since the K value setting in the V1 version has a greater impact on the pricing results, in their V2 version, vAMM is abandoned and the AMM mechanism of Uniswap V3 is adopted. When the user deposits funds to provide liquidity, the funds will be deposited into the Vault, and a group of LPs will be minted into Uniswap V3. When users trade, the margin will be deposited into the Vault, and vUSD will be minted and swapped in Uniswap V3. The entire transaction process is a game process between AMM's LP and the long and short traders.

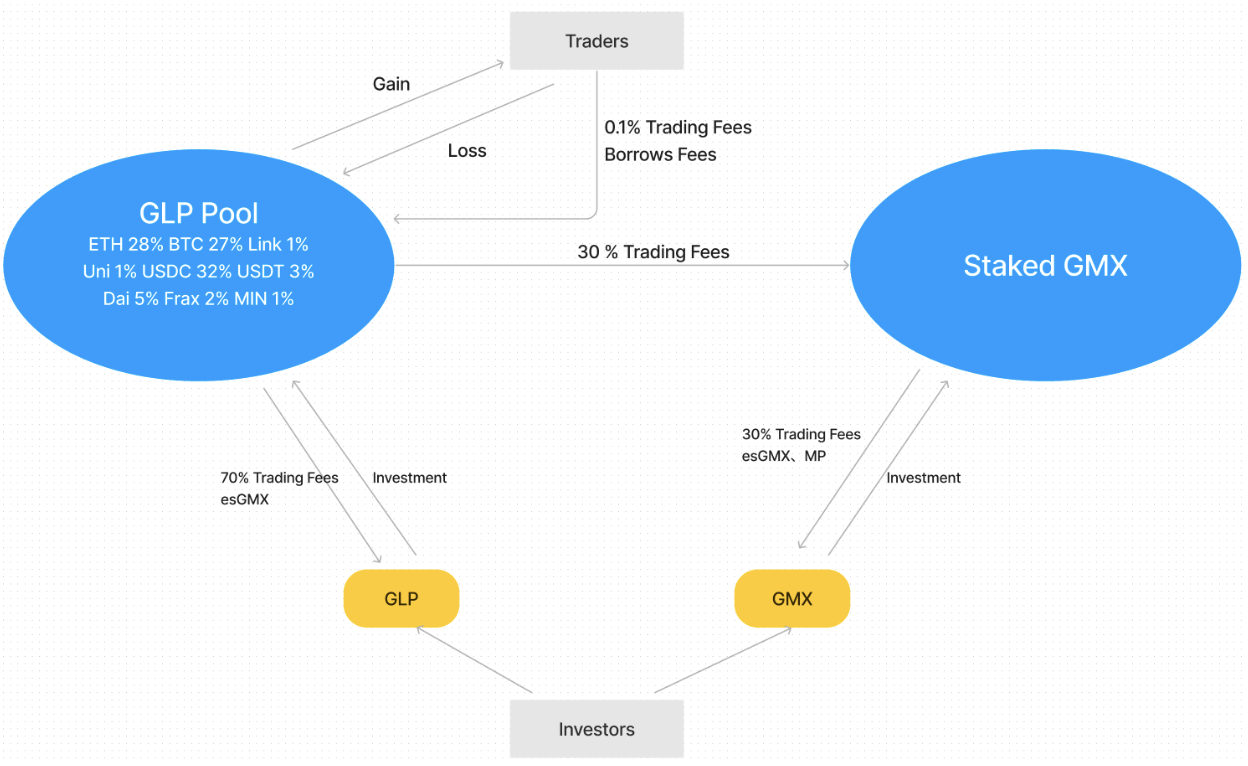

LP as the Counterparty - GMX

GMX is a leveraged trading protocol deployed on the Layer 2 protocol Arbitrum, which currently supports up to 30x leveraged trading. The counterparty of all transactions is the GLP pool. The GLP token is a special token composed of BTC, ETH, USD and other tokens in a certain proportion. Users can use the tokens included in the GLP to purchase GLP to start market making , because it is a single currency liquidity, so there is no problem of impermanent loss. Since the counterparties of all transactions are LPs, there is also a zero-sum game between LPs and traders: the margins of traders' losses will be directly allocated to GLP (reflected in the price increase of GLP), and traders earn profits directly from GLP they acquired (reflected in a drop in the price of GLP). Since the order book and AMM modes are not used, there is no problem of price deviation, and there is no need to balance long and short positions through funding fees. The price of opening and closing positions is provided by the keeper or oracle.

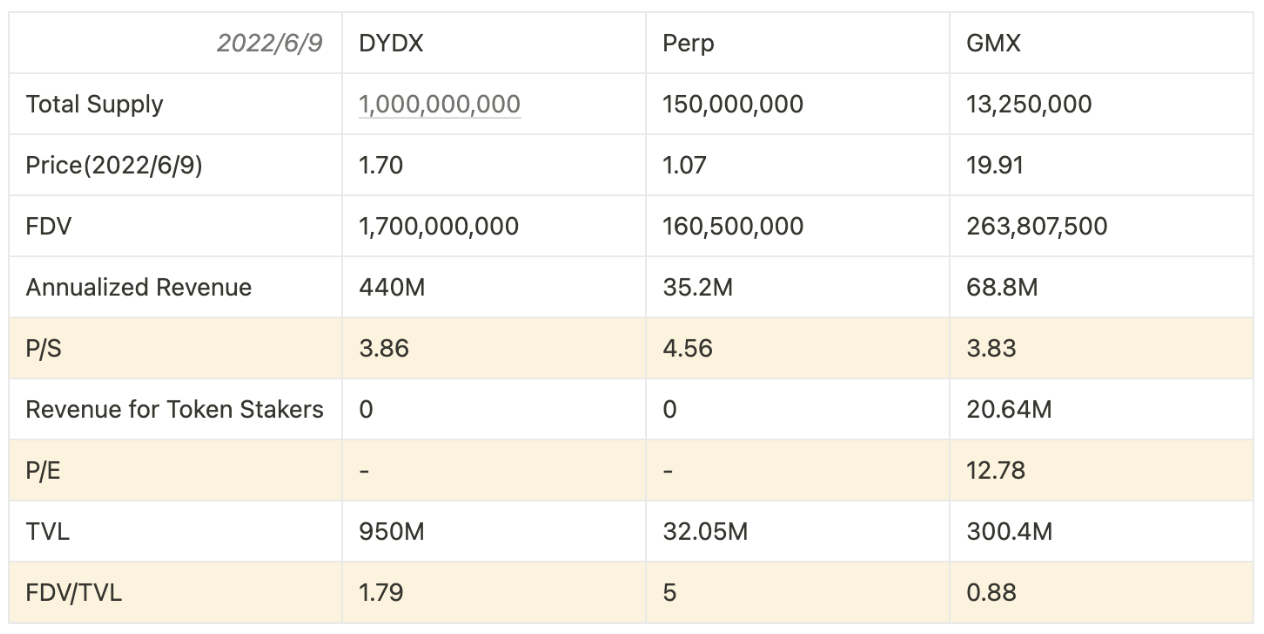

A Comparison in Mechanisms

A Comparison between Token Prices

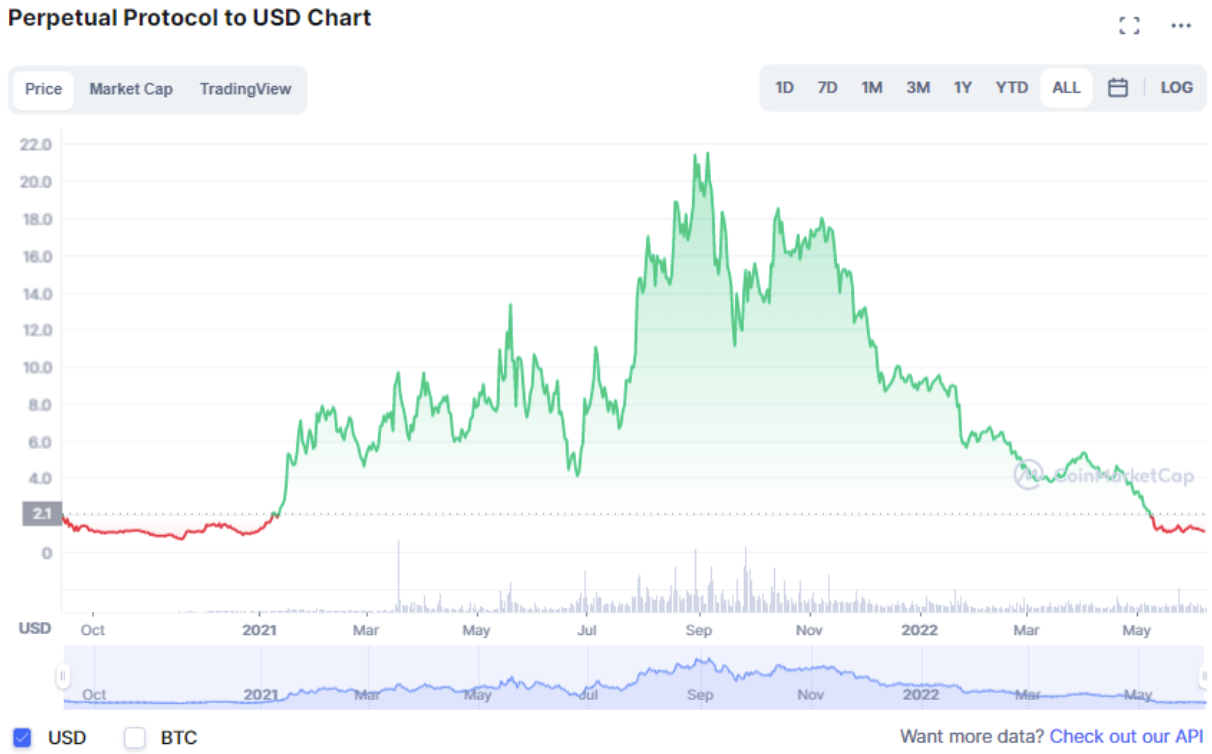

Although DYDX has been leading in trading volume, the price of DYDX token has continued to decline since its listing due to the massive selling pressure generated by DYDX's trading reward incentives and the inability of the token to capture the profits generated by the protocol.

As a perpetual futures product that issued tokens earlier, it enjoys a certain advantage in the derivatives market. However, the k value of the vAMM mode of the v1 version is not easy to set, and it’s vulnerable to attacks. The game process is more complicated. If the market is not balanced between long and short, traders may still lose money even though they bet in the right direction. Although the V2 version is based on the real liquidity of Uniswap V3, the AMM model has many defects, and the pricing process is more complicated. In the case of insufficient liquidity, the trading experience is poor. After DYDX issued their token, it attracted the attention of investors in the derivatives market and seized most of the market share, which made Perpetual Protocol's revenue and token performance continue to decline.

The game theory of GMX is simple and reasonable. Since it was deployed on Layer 2, its performance has continued to grow. The price chart of their GMX token has also followed the sentiment of the cryptocurrency market, and it has not crashed badly like DYDX and PERP.

Detailed Analysis of GMX

GMX is a perpetual trading protocol migrated from XVIX and Gambit on BNB Chain to Arbitrum.

Highlights

- 0 trading slippage

- Up to 30x leverage

- No impermanent losses on LPs

Mechanisms

- Leveraged Long

- If the loss is measured by the USD standard, the maximum profit of the trader, that is, the loss of GLP, will be infinite, so the long assets are locked according to the leverage ratio. For example, use 1 ETH or its equivalent assets to leverage 10 times to long ETH, then 10 ETH in GLP will be locked. When the user closes the position, the user's profit or loss is calculated by the price of the oracle machine, and the locked assets in the GLP are unlocked and profits or losses are paid to the user.

- Leveraged Short

- The maximum profit of a trader, that is, the maximum loss of GLP, is the current price of the asset, so it is necessary to use stablecoins for shorting. If the current price of ETH = $2000 and short 1 ETH with 10x leverage, you need to pay $200. At this time, $2000 in GLP is locked as the maximum loss of GLP. When the user closes the position, the user's profit and loss is calculated through the price of the oracle machine, the assets locked in GLP are unlocked, and the user's profits or losses are paid.

Tokenomics

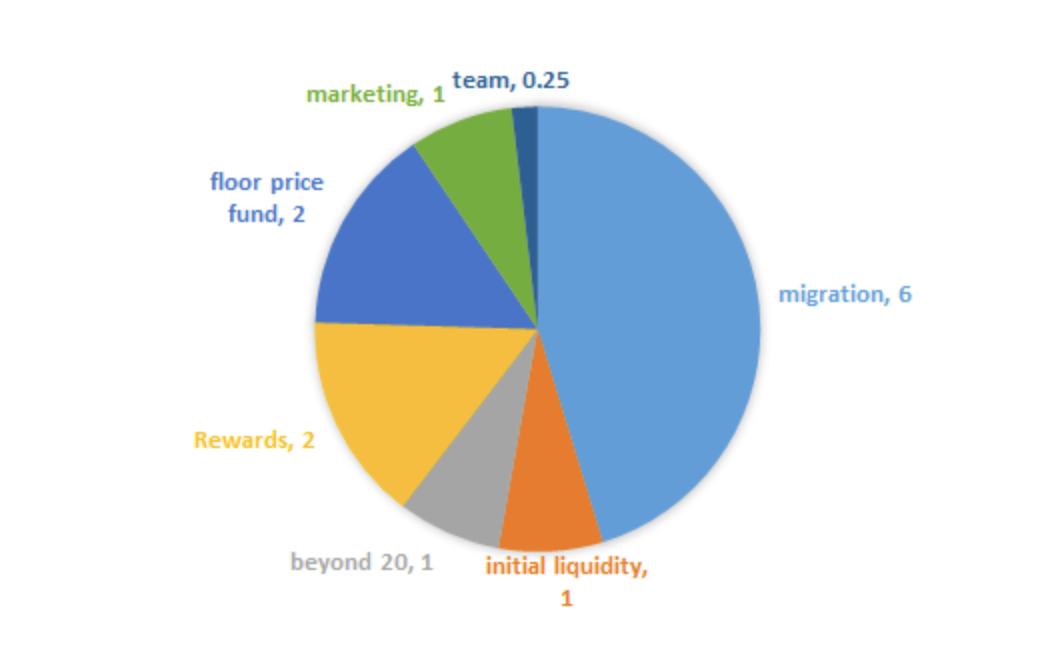

GMX Token Allocation

The governance token is GMX, and the total supply is 13.25 million.

- 6 million (45.28%) migrated from XVIX and Gambit

- 1 million (7.55%) and ETH to form LP as initial liquidity

- 1 million (7.55%) to provide additional liquidity after GMX price exceeds $20

- 2 million (15.09%) as staking reward

- 2 million (15.09%) for the GMX floor price fund to guarantee the minimum liquidity requirement of GMX.

- 1 million (7.55%) for marketing, partnerships and community developers

- 250,000 (1.89%) distributed linearly to the team within 2 years

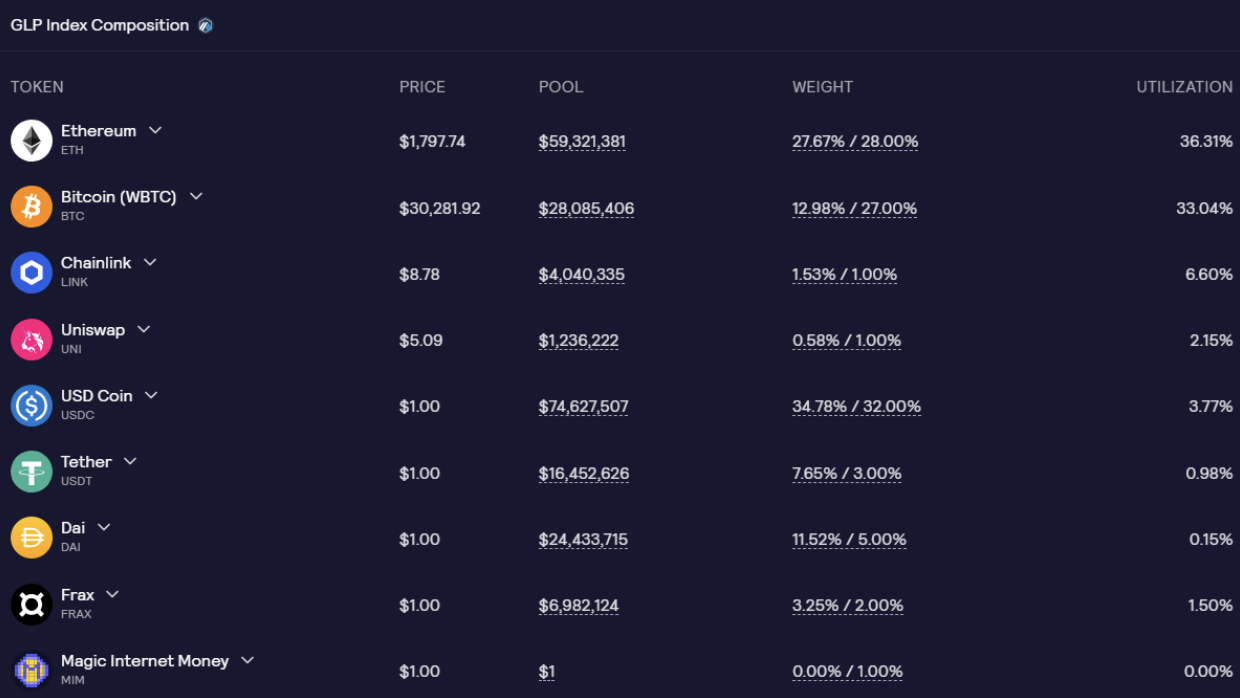

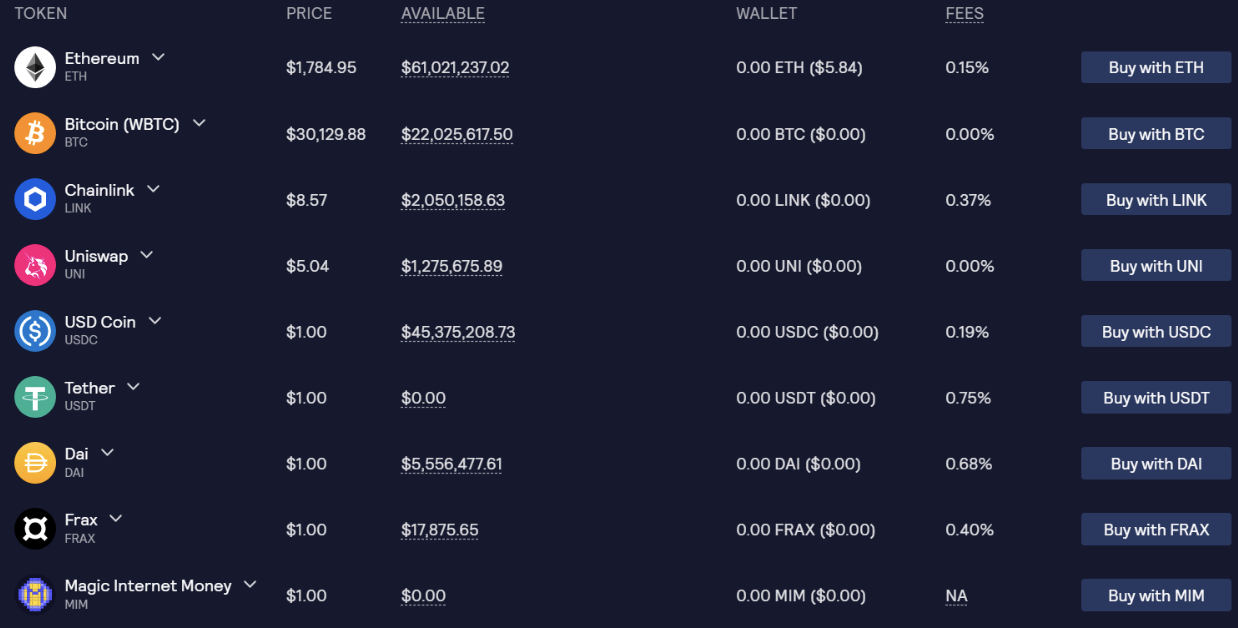

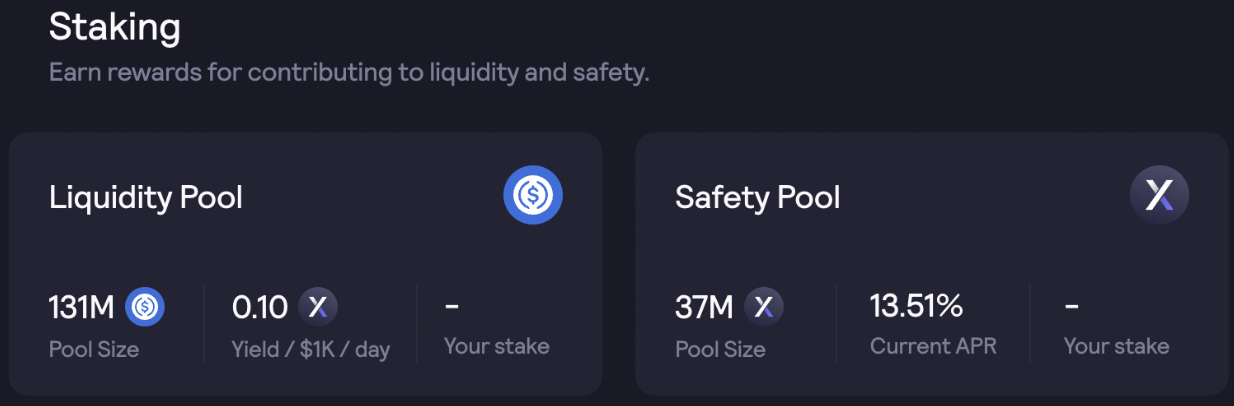

GLP - The Counterparty of Trading

- GLP is the liquidity provider for perpetual futures trading, acting as the counterparty to all traders.

- A basket of asset indexes is formed according to a certain ratio. When users use the assets in the basket to purchase GLP, new GLP will be minted. The purchase process is equivalent to providing liquidity to the protocol and selling GLP into assets in the basket. GLP will then be destroyed, which is equivalent to withdrawing liquidity (you need to hold GLP for at least 15 minutes to be destroyed).

- Rebalance the asset ratio by adjusting the purchase rate. When the asset ratio is higher than the target ratio, the purchase fee rate will be increased, and when the asset ratio is lower than the target rate, the purchase fee rate will be reduced.

- In the long run, traders have a high probability of losing money, and GLP has a greater chance of winning

Capturing Value

Platform’s revenue source

- 0.1% transaction fee

- Borrow fee, the hourly rate = (assets borrowed) / (total assets in pool) * borrowing rate(depending on the liquidity in pool, currently around 0.0005%)

- Uniswap ETH/GMX LP fee dividend, as the Floor Price Fund to provide GMX’s minimum liquidity

GMX

- You need to stake GMX on the platform to capture value

- 30% platform fee dividend

- Escrowed GMX (esGMX) Rewards:

- Users can choose to release esGMX linearly for one year, but they need to keep the amount of GMX staked before esGMX will be released. For example, staking 1000 GMX will get 100 esGMX. If there’s only 500 GMX staked, only 50 esGMX will be released.

- Users can choose to stake esGMX, and esGMX and GMX have the same dividend weight.

- Multiplier Points Rewards:

- 100% APR reward, i.e. stake 100 GMX, get 100

- Multiplier Points after one year Multiplier Points and GMX have the same weighted dividend ratio. When the user ends the staking of GMX, the same proportion of Multiplier Points will also be destroyed.

GLP

- 70% platform fee dividends

- Escrowed GMX (esGMX)

Operating Stats

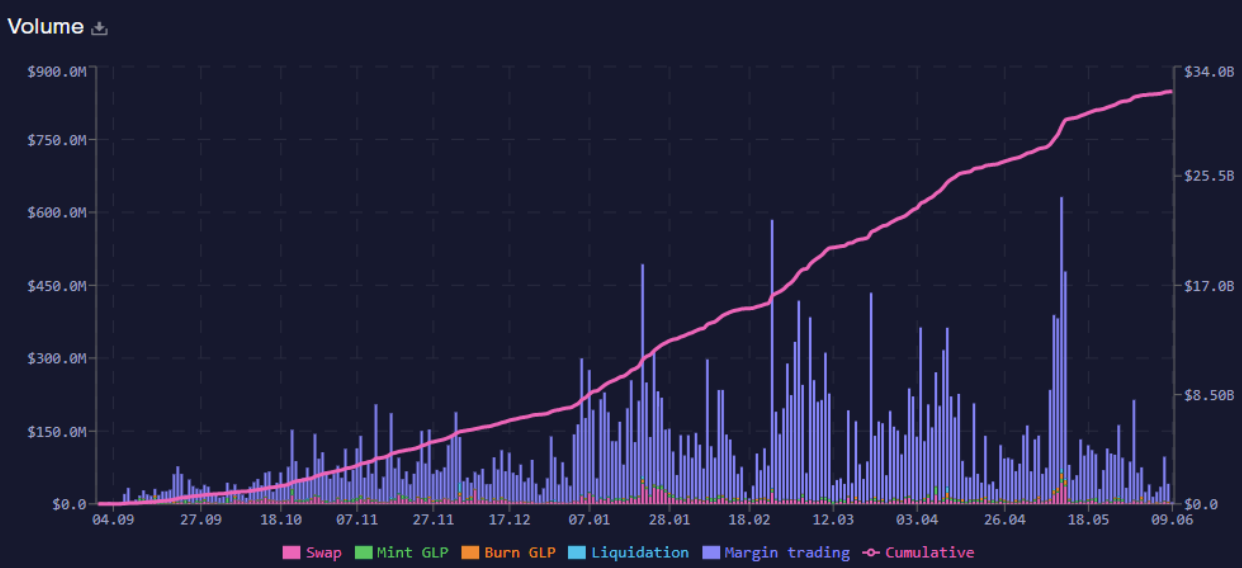

Comparison in Trading Liquidity

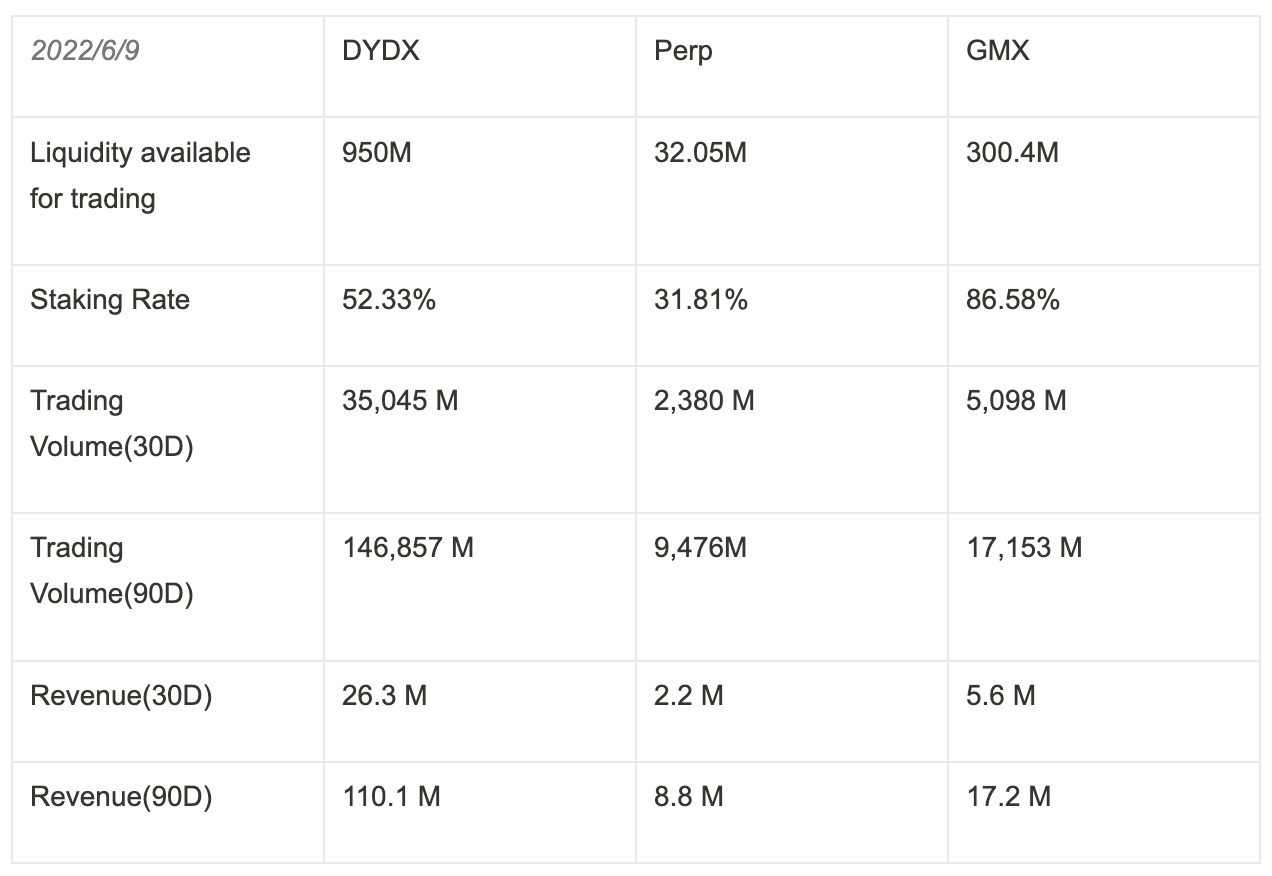

Trading liquidity is measured by the TVL available for trading.

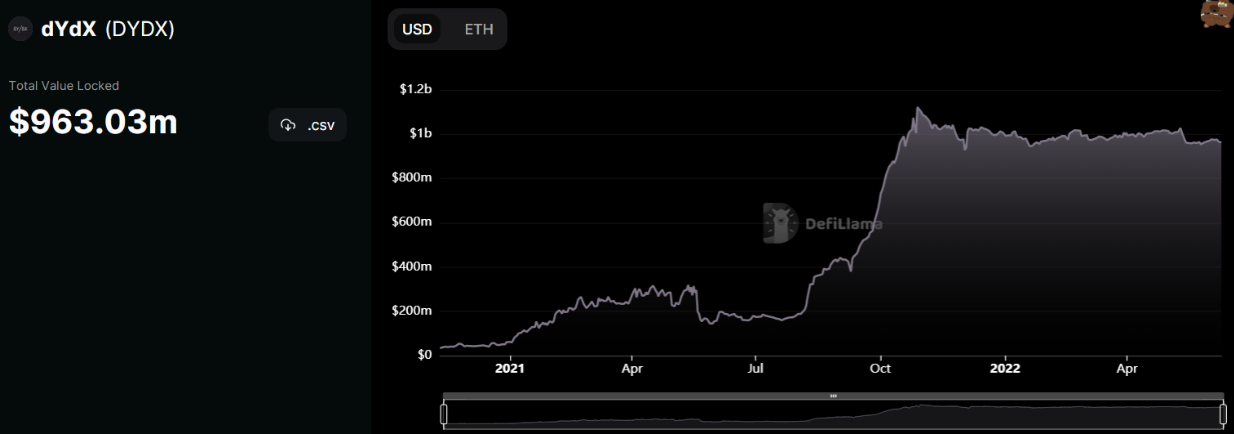

- DYDX: In addition to users staking USDC, there are also centralized market makers to provide liquidity. The main liquidity is provided by professional centralized market makers, thus a smaller drawdown in TVL in the bearish market.

- Perpetual Protocol: The liquidity is poor, and the bear market backtest is large. Since LPs need to bear impermanent loss, they cannot motivate liquidity very well, and derivatives transactions are extremely dependent on liquidity.

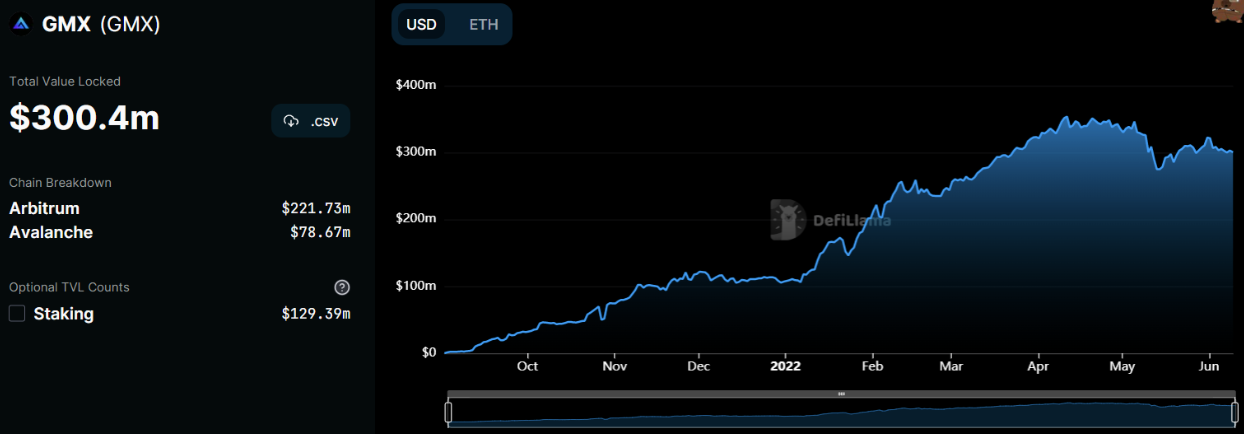

- GMX: The liquidity growth of GMX is relatively good, and the bear market drawdown is small.

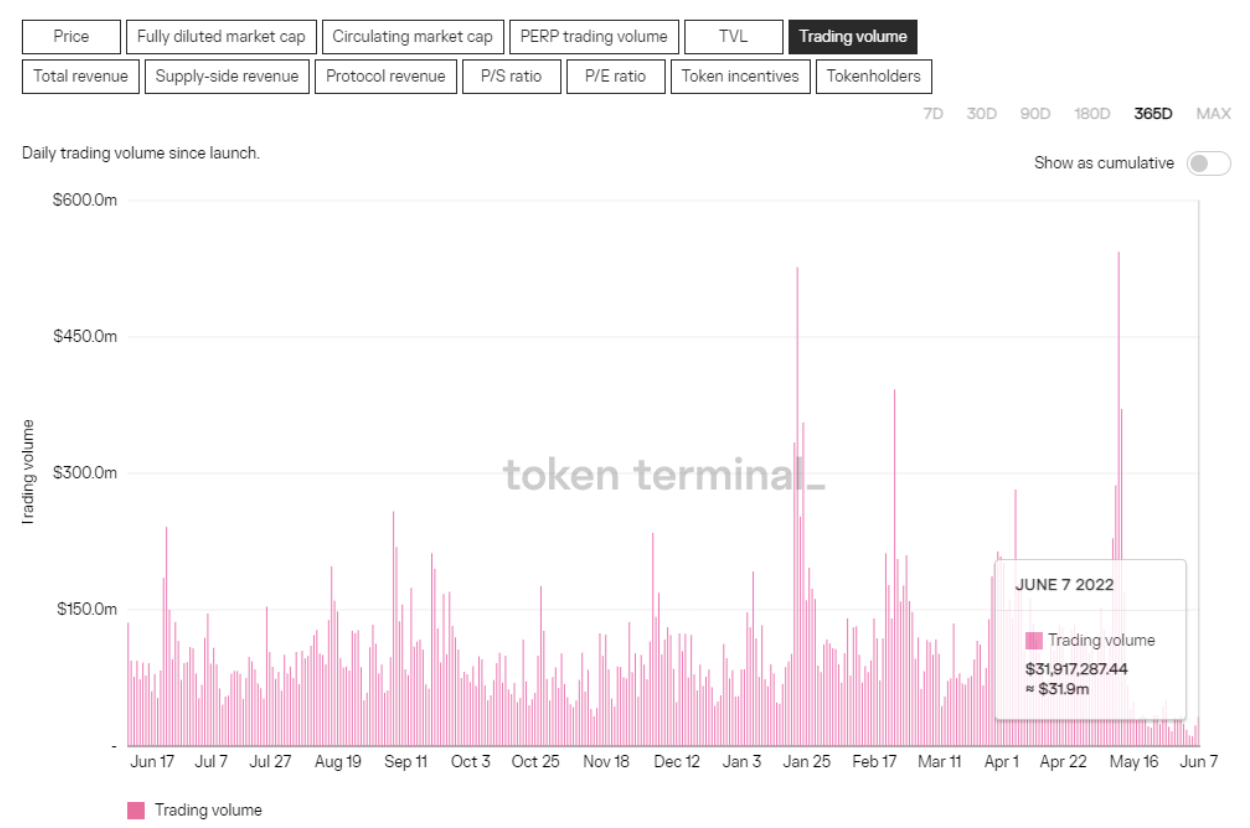

Trading Volume

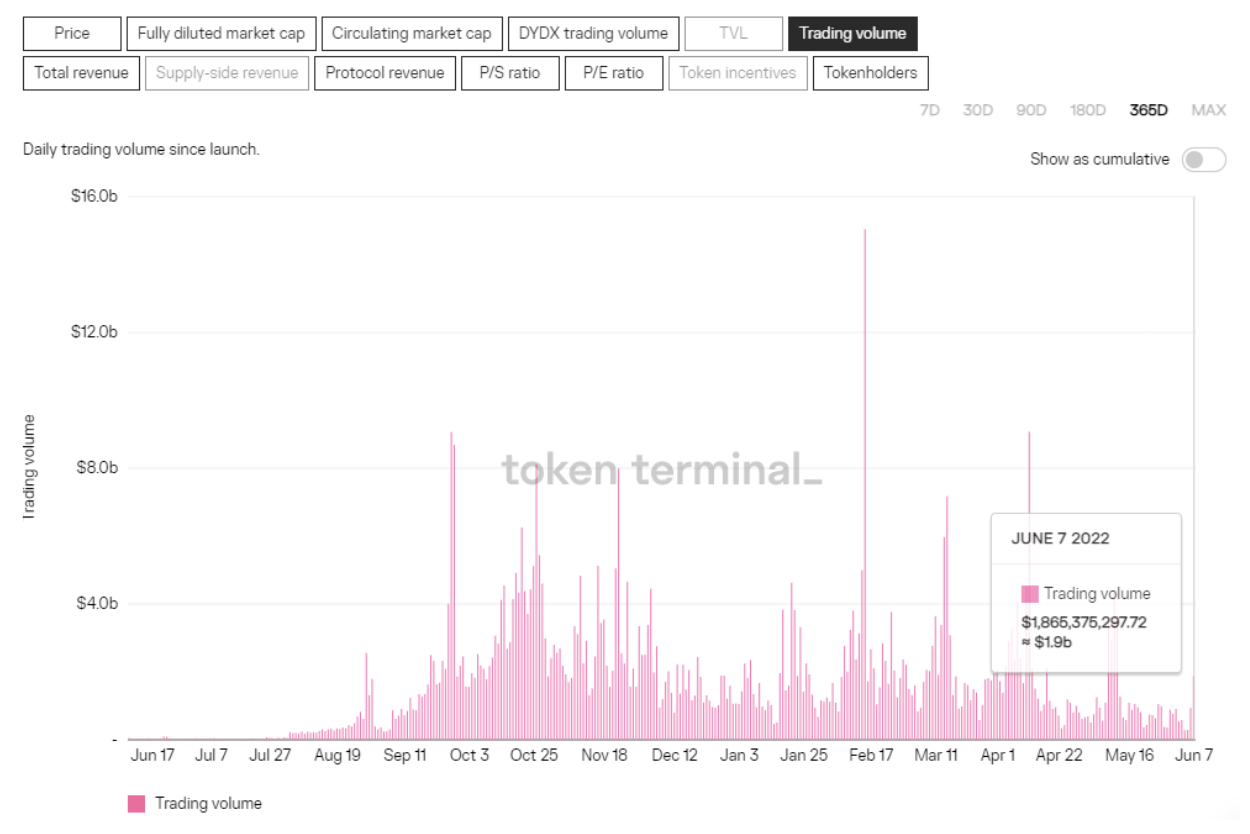

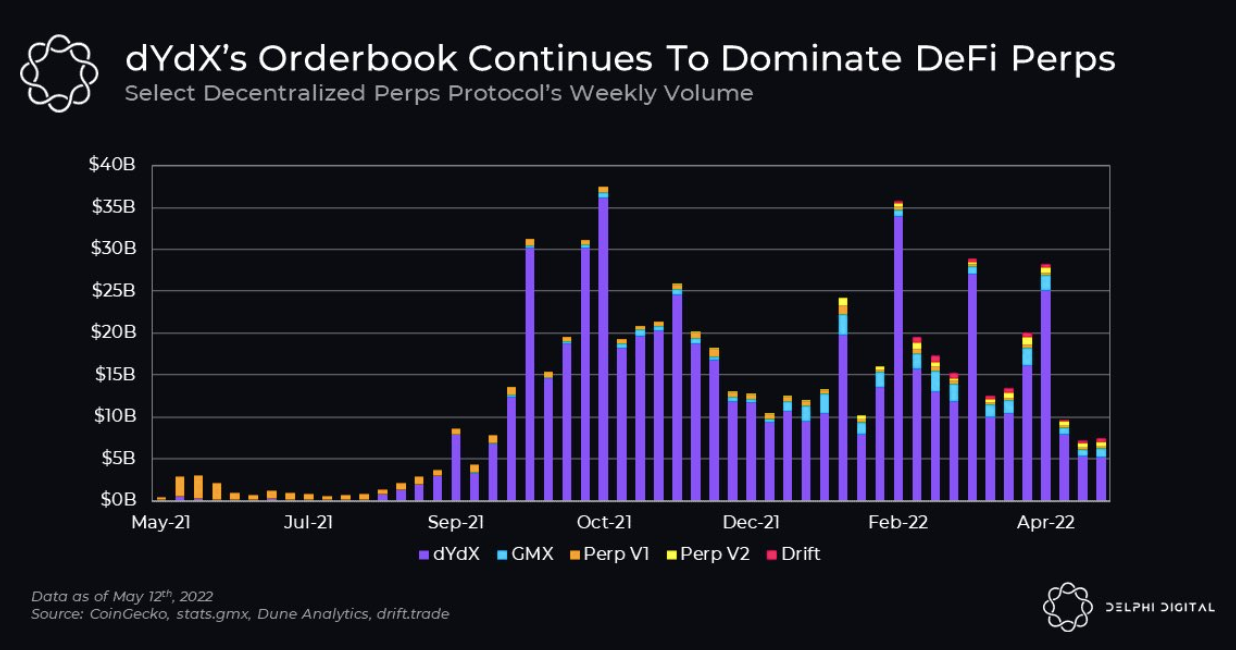

- DYDX: Trading mining rewards and professional market makers drive high trading volumes

- Perpetual Protocol: Lack of liquidity leads to high transaction slippage, which cannot motivate trading well.

- GMX: The trading volume in the bull market is 300-500M, the trading volume at current is 30-70M. The main trading volume is contributed by leveraged trading

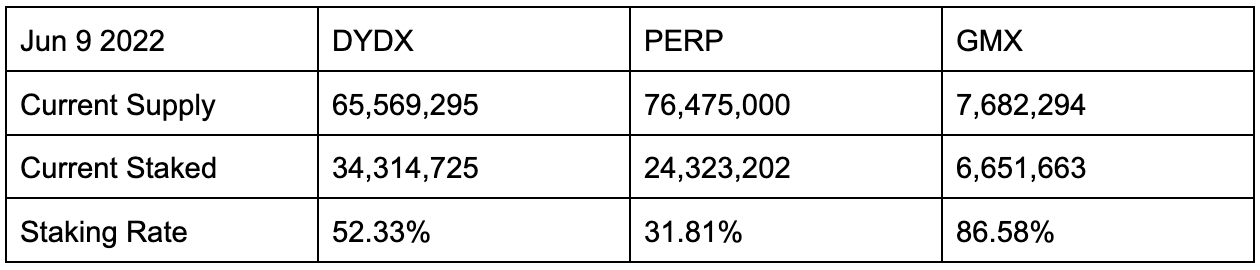

Ratio of Token Staked

The token staking rate reflects the token’s ability to capture value and the degree of reluctance to sell stakes.

Value capture ability:

- Perp: token reward, trading dividend is planned,

- DYDX: 0 trading dividend, token reward,

- GMX: 30% trading dividend + token reward

The staking rate of GMX’s circulating tokens is high, and the market stakes are relatively reluctant to sell; PERP V2 trading dividends are being designed, and the veToken model is expected to be used. At present, there is a certain lock-up period for withdrawing from staking. The poor performance of the token market also reduces users' willingness to stake.

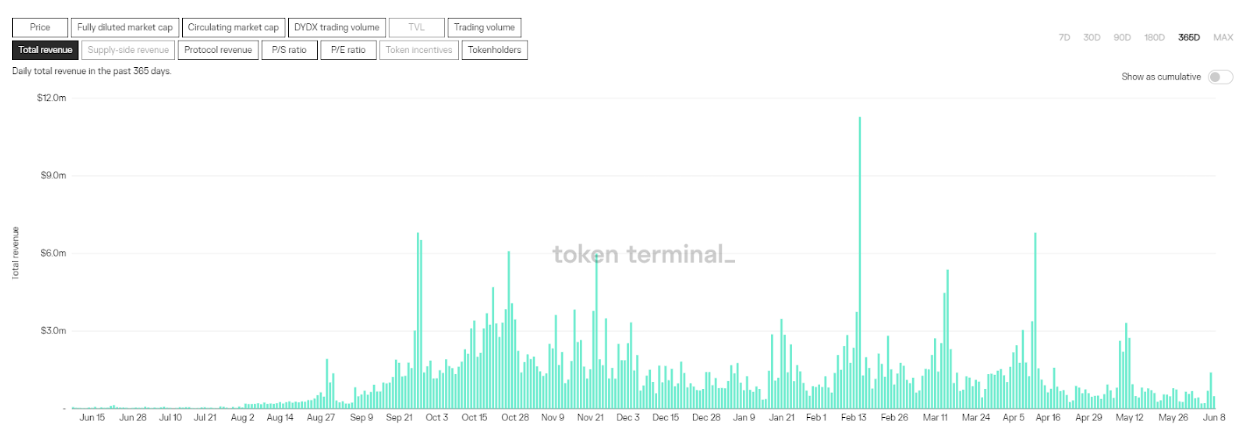

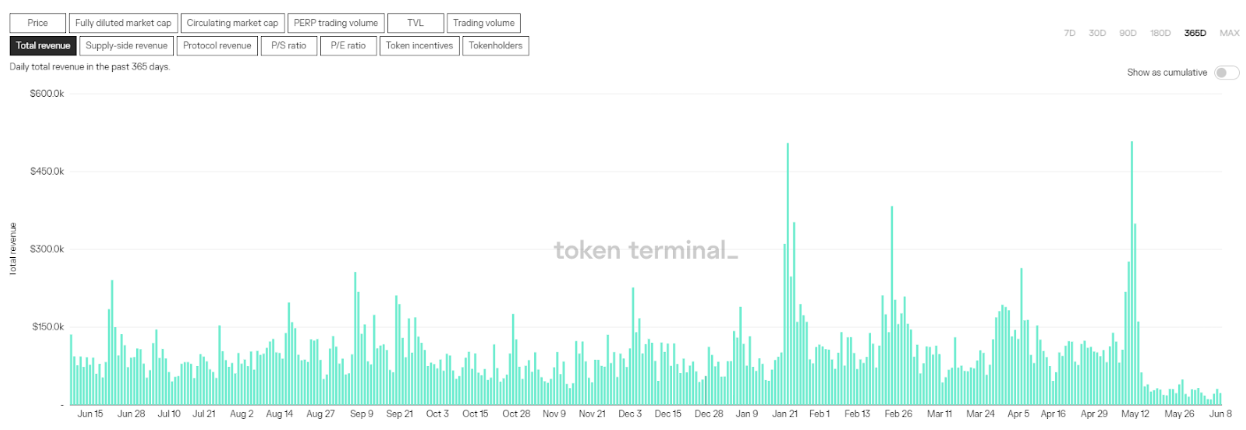

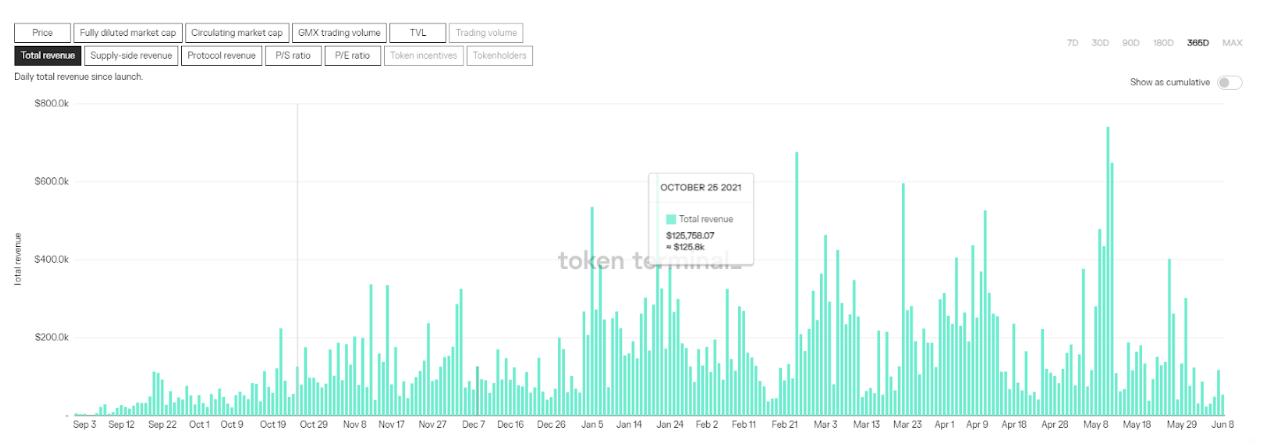

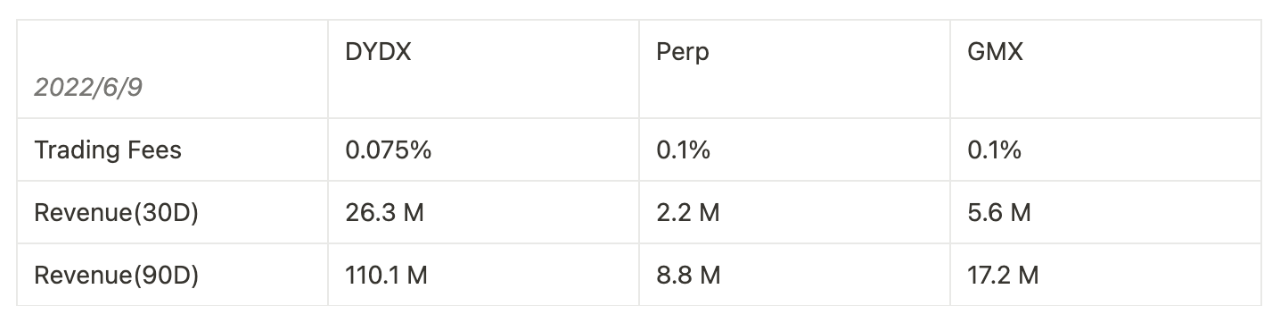

Revenue

- DYDX

- Perp

- GMX

Since DYDX has the advantage of trading mining reward, the best liquidity, and low transaction fees, its revenue far exceeds the other two protocols. Although Perpetual Protocol's TVL is 1/9 of GMX's, its revenue is only 2 times that of GMX, so Perpetual Protocol's capital utilization rate is relatively high.

Summary

Valuation Model

Comparison in Valuation

From the PS point of view, GMX is the lowest but close to DYDX. Since only GMX tokens can realize the value capture of the protocol, only GMX has a price multiplier; GMX's FDV/TVL is far lower than other protocols. Since GMX has 2 million staking rewards distributed through esGMX and Multiplier Points, it will take longer to convert into tradable GMX, so the actual price multiplier of GMX will be lower. Judging from the comprehensive valuation comparison indicators, GMX has the possibility of being undervalued.

The Top-Down Valuation Method

- Logic for growth

- β: CeFi’s frequent crises and the development of Layer 2, the market share of on-chain derivatives is expected to further increase

- α: Arbitrum is expected to issue tokens, accelerating the positive flywheel of GMX

The recent crises of centralized institutions such as Celsius and Babel have caused market liquidity crises and trust issues, and users’ demand for DeFi has further increased. At present, there is still a large gap between the market share of the entire decentralized leveraged trading scene and the centralized exchanges. The market share of the entire decentralized leveraged trading scene is expected to grow further.

Optimism’s issuance of tokens will force competitors to fight back. Before Arbitrum officially issues their tokens, users may interact on Arbitrum for the purpose of hunting airdrops. GMX is currently the product with the highest TVL on Arbitrum, and its security is relatively high, so it can attract the attention of some airdrop hunters. After Arbitrum issues tokens, some of the money that flows in will remain in the ecosystem. GMX will be the first choice for big players to conduct liquidity mining, and with the TVL increasing, the trading cost will fall to attract more trading,which is expected to promote the positive flywheel of GMX.

- Assumptions in valuation

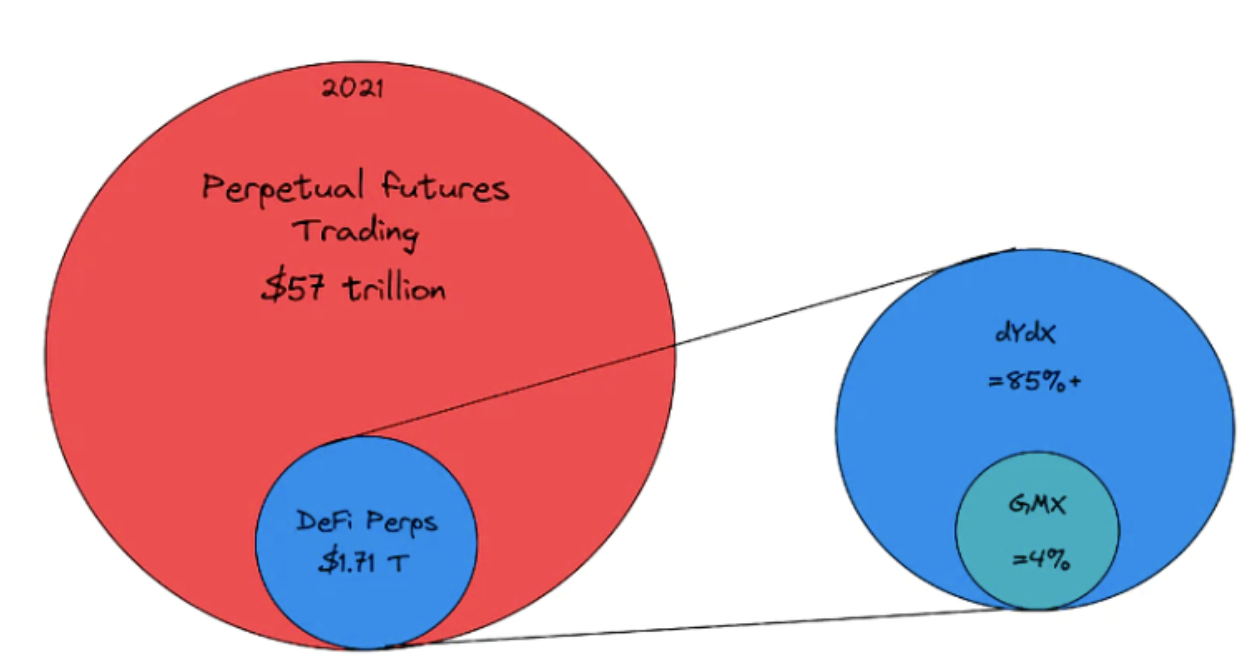

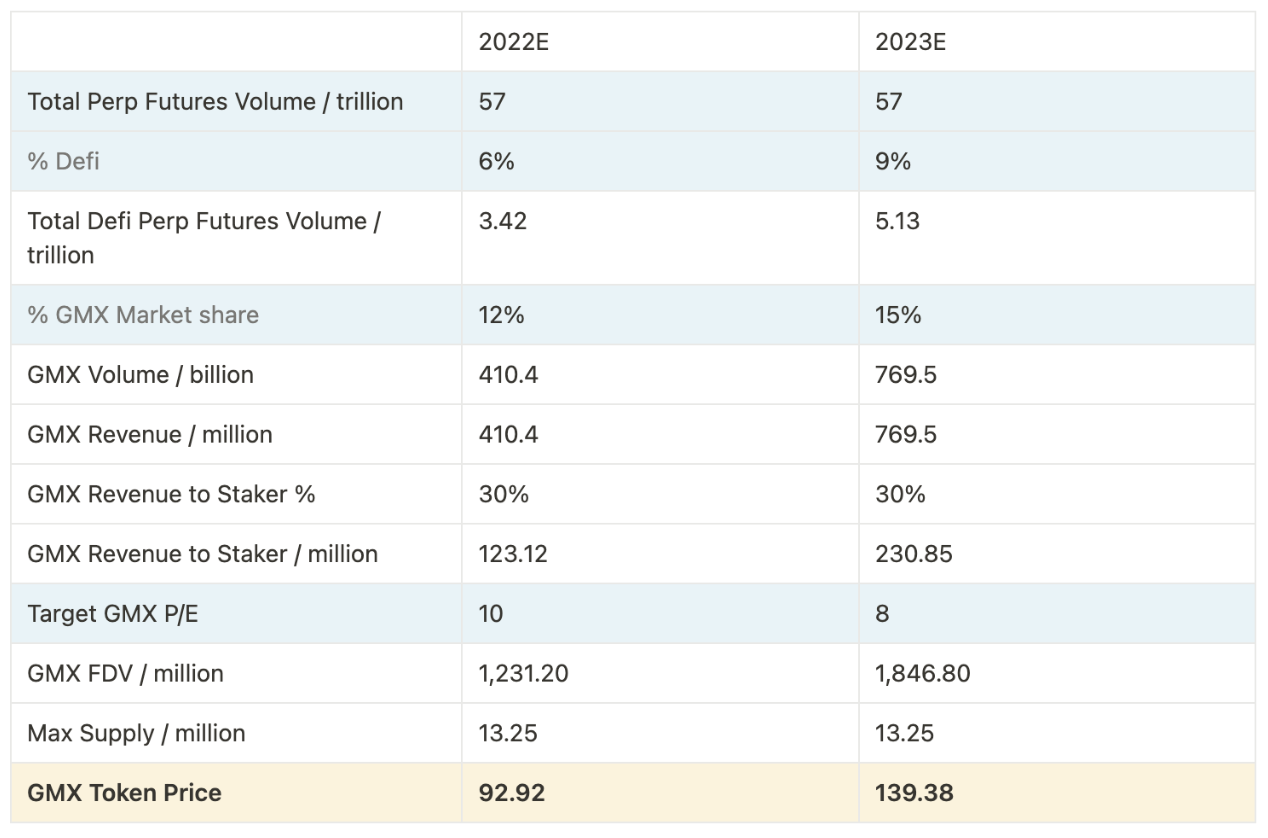

- The crypto market is cyclical and we are currently in a bear market. It is expected that the perpetual trading volume will remain unchanged at 57 trillion in the next two years.

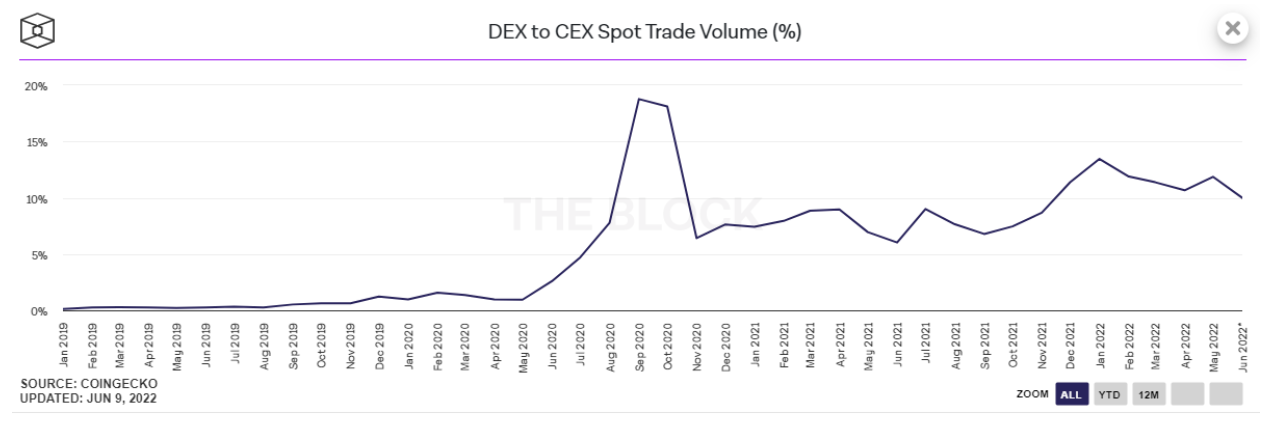

- In 2021, the trading volume of perpetual trading was 57 trillion, while the trading volume of DeFi derivatives was only 1.71 trillion. The penetration rate of DeFi perpetual trading was only 3%, and the ratio of DeFi spot trading volume to CEX trading was maintained at about 10%, so about 9% penetration. It is expected that the penetration rate of DeFi perpetual trading will reach the spot level in the next two years. Penetration is expected to be 6% in 2022 and 9% in 2023

-

- In 2021, GMX accounted for 4% of the market share of DeFi perpetual trading. Since GMX was launched at the end of August, it accounted for less in 2021. According to The Block’s data, GMX currently accounts for about 10% of the market. With the prediction of Arbitrum’s issuance of tokens will promote GMX’s positive flywheel, GMX’s market share will gradually increase. It is estimated that the market share will be 12% in 2022 and 15% in 2023.

- Due to the gradual increase in the industry’s penetration rate and GMX’s market share, the target P/E of GMX will gradually decrease. It is estimated that the P/E in 2022 will be 10, and the P/E in 2023 will be 8

-

Valuation Model

A top-down valuation of GMX based on the above assumptions is expected to have a target price of 92.92 by the end of 2022 and a target price of 139.38 by the end of 2023. The current price of 19.91 is somewhat attractive.

-

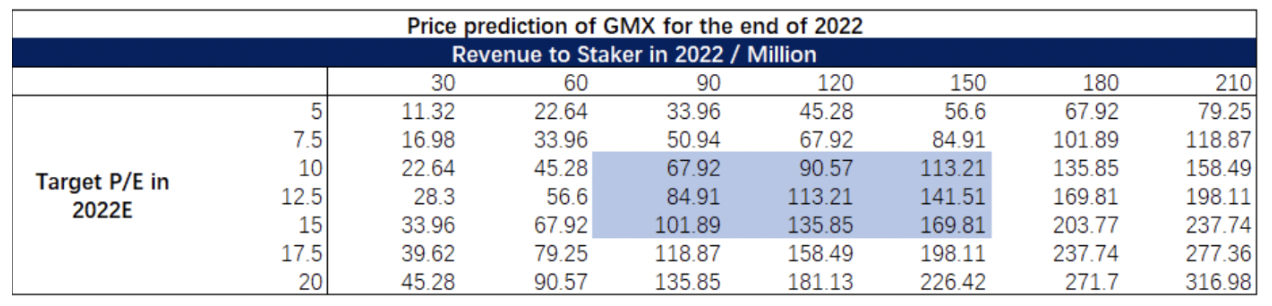

Sensitivity Analysis

By controlling the target P/E and conducting a sensitivity analysis on staker's revenue in 2022, in an extremely pessimistic case, the price of GMX will be 11.32, and the decline from the current 19.19 is limited. The valuation center is between 67.92 and 169.81, which is several times the current price, so the current price of GMX has good odds.

Conclusion

- At present, the penetration rate of DeFi perpetual trading volume is low, and the L2 token issuance rush will likely promote the further penetration of DeFi perpetual products.

- The GMX trading game model is simple, and the slippage of LPs and traders is low. Arbitrum’s token issuance is expected to promote GMX’s positive flywheel and increase its market share.

- The value of the GMX economic model is clearly captured, and the selling pressure of token rewards is small. Most of the tokens are staked, and the stakes are relatively reluctant to sell.

- The valuation of GMX is relatively low in the same field, and there is relatively large space for its price growth.

Join Us Here:

About Us:

Twitter: @RealResearchDAO

Medium: https://medium.com/@RealResearchDAO

Discord: discord.gg/ZSdgM7x6pc