Introduction

Even though this blog post is intended to provide an overview of the M^0 Protocol, it's improbable that sections covering whitepaper details, protocol mechanics, etc. will constitute more than 30% of the content. In this case, comprehending the ambitions of M^0 is infeasible without grasping the fundamental principles of money and the contemporary monetary system — or, to be more exact, the different perspectives on these concepts, particularly the one embraced by Luca Prosperi and his team.

I am not affiliated with the M^0 Protocol nor connected to their team in any possible way. However, I do have considerable experience as a bank consultant (in public-private partnerships, which bear a closer resemblance to the banking system than one might initially think) and as a DeFi researcher and degen. Moreover, I kind of like delving into complex systems with people as the fundamental elements of them - it’s difficult to find a system more intricate and expansive than the one underlying what we refer to as "money”. So, for me, writing this post is more like a brain exercise rather than anything else. I do not possess any kind of formal degree in economics/finance/banking, so the text below could contain every possible flaw - from minor mistakes to totally incorrect interpretations of the fundamental mechanics of the financial world (though I hope it doesn’t).

But before we begin, I’ll drop some key facts about M^0 Protocol

-

M^0 Protocol positions itself as a coordination layer for permissioned institutional actors to generate $M (cryptodollars);

-

the ultimate goal is to replace an archaic, centralized, and closed banking infrastructure with open, decentralized, interoperable money technology;

-

the core team consists of Luca Prosperi (worked at MakerDAO in Lending Oversight), Greg Di Prisco (MakerDAO's former head of business development), and Oliver Schimek (previously CEO at fintech company CrossLend);

-

protocol closed the $22.5m funding round in April 2023.

Following the announcement of M^0 Labs' creation in April 2023, the most prevalent reactions I observed in crypto-related chats were “the description is very shady, I don’t understand what their product is” and “just another stablecoin, boring”. After the whitepaper’s release (a few weeks ago), I didn’t observe any reactions at all - guess it’s because crypto-anarchists are too busy with points farming. Such disregard doesn’t seem right, so let’s fix it!

Hmmm… not so fast. First, let’s deconstruct some of the well-known concepts like “money” and “banks”.

What is money?

What comes to mind when you think about money? A dollar bill? Numbers on your smartphone? USDT in your Binance account? While it's undoubtedly correct to view a dollar bill as "money," this perspective is not the only one, nor is it necessarily the most fruitful. Just as the behavior and fundamental properties of particles in quantum mechanics can significantly vary depending on the context in which they are analyzed or observed, the behavior and fundamental properties of money will depend on the context in which we analyze them as well. Therefore, let's slightly shift our focus and rephrase the initial question to "How can we think about money?”

Utilitarian approach

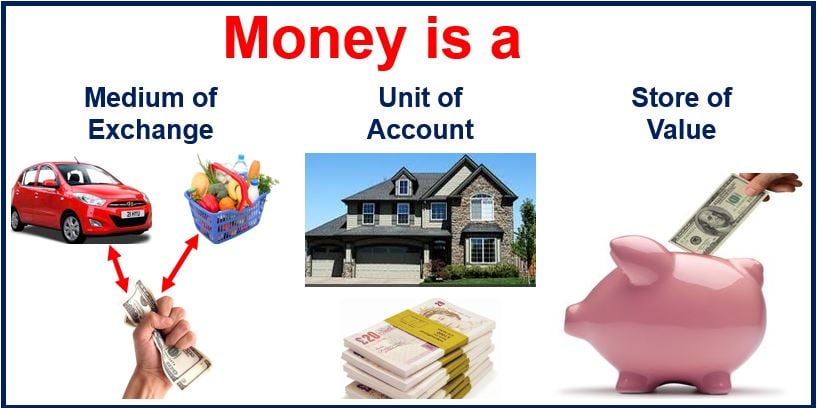

Perhaps the most conventional method to define money is by outlining its functions. According to the International Monetary Fund (IMF), money can serve as a

-

store of value, which means people can save it and use it later — smoothing their purchases over time;

-

unit of account, that is, provide a common base for prices; or

-

medium of exchange, something that people can use to buy and sell from one another.

Wikipedia defines money as any item or verifiable record that is generally accepted as payment for goods and services and repayment of debts, such as taxes, in a particular country or socio-economic context.

This approach, while practical and useful for everyday transactions, does not delve deeply into the essence of what the word “money” represents. Additionally, numerous edge cases exhibit all these characteristics yet may not convincingly be recognized as money. Notable examples include

-

local currencies;

-

local exchange trading systems (LETS);

-

cryptocurrencies.

One might argue that DOGE qualifies as money since it satisfies the aforementioned criteria. Similarly, the credit on your SIM card could be considered money if it can be exchanged for other forms of money or goods. However, it feels like thinking in this direction doesn’t bring us closer to understanding the concept of money but rather blurs its definition. So, let’s change the context.

Money as a representation

Envision yourself touring a museum dedicated to the history of money. Within its halls, you'd encounter every conceivable form of currency that has ever circulated on Earth, ranging from conch shells to some incomprehensible applications on smartphones. Naturally, this would prompt the question: why did people adopt these diverse items as a means of exchange? What is the source of their value? The responses to these inquiries can differ widely

-

the situation with commodity money is quite straightforward - its value comes from the commodity from which it is made (conch shells, barley, etc.);

-

representative money signifies something of value - there was a time when coins or banknotes could be exchanged for a certain amount of a commodity (most often gold) they represented, backed by an institution (usually a government) that guaranteed this exchange;

-

the value of fiat money does not stem from any intrinsic value or convertibility - instead, its value arises from a combination of social consensus and trust in the government (and the rules it sets) that designates the currency as legal tender;

-

the value of banking deposits (digits in your banking account), PayPal accounts, and tokenized dollars is derived from the value of fiat money (though the mechanisms that sustain their value differ from those for a “pure” fiat aka cash) - fundamentally, you must accept that “underlying” fiat money is valuable in the first place;

-

for crypto-backed stablecoins (LUSD, mkUSD, etc.), the baseline once again is the value of fiat money (USD) to which these stablecoins are pegged, but with different mechanisms to maintain the value.

Since the dissolution of the Bretton Woods system in 1971, the world’s major currencies have been fiat money. People are willing to accept them as valuable because they trust that their issuers (governments/central banks) will ensure the acceptance of fiat money for all legal payments within their jurisdiction. We are accustomed to using fiat money in the form of coins or banknotes. Both are pure forms of fiat money: sanctioned by the government, produced by the government, and universal in the sense that for any economic actor, it makes no difference whether their goods/services are paid for with a USD banknote printed in 2010 or 2020.

The situation with banking deposits, PayPal accounts, and other digital forms of fiat money is more nuanced. However, the boundaries of our “money as a representation” perspective are becoming too limiting from this point, so let’s move further and try a different angle.

Money as a product

Today, the most prevalent form of money is digital, a significant shift from the cash-dominated era (banknotes and coins) of 30 years ago. I’m not referring to cryptocurrencies here but to the digits provided to your bank account or mobile application by your bank. While many perceive these as digital versions of fiat money (something that crypto-native chad would call “wrapped fiat”), they are, in fact, derivatives, which are supposed to be hard-pegged to real fiat money. And these derivatives are essentially banking products we’re talking about. Below, I've outlined some key points that I believe are crucial for developing an understanding of "money as a product”, but for more comprehensive explanations, feel free to explore the links provided below

-

banks hold fiat money (primarily in the form of digits in registries) obtained from the government/central banks, their investors, and clients (primarily depositors) - this fiat money, among other assets, constitutes the bank’s assets;

-

in most cases, banks do not transfer fiat money to their clients (cash transfers are an exception) - the digits you or your company see in the bank application, whether they represent your deposit or credit balance, are not the same as fiat money;

-

these digits signify your entitlement to demand a specified amount of fiat money from the bank - from your perspective, it represents a legal right, from the bank's perspective, it's a legal obligation linked to your right;

-

if we were discussing similar obligations of private, unregulated companies (say, companies A and B) as parties involved, we wouldn't consider these obligations as equivalent - depending on how reliable these companies are, we would discount the value of these legal rights;

-

the valuation of our rights to claim fiat money from A and B might be, for instance, $0.98 on 1 USD for low-risk A company and $0.75 on 1 USD for high-risk company - maybe we’d even designate tickers for USD claimable from A and B - aUSD and bUSD;

-

banks are not vastly different from companies A and B in that they possess varying risk profiles, policies, and so on - so why don’t we call legal rights towards them as svbUSD, msUSD, and so forth?

The reason we refer to them as USD and perceive them as fiat money is because, to you as a customer, these legal rights function as fiat money: they are accepted in every store in your country, they are interchangeable with each other and with fiat money, and they are stable enough for our minds to simplify the concept and overlook these nuances. In other words, they’re functionally equivalent to fiat money. The bank's main objective is to ensure its version of USD (its product) is as stable and user-friendly as possible - the better the stability and user experience, the superior the product. In this context, entities like PayPal, Circle’s USDC, and other digital money issuers build upon this foundation - they utilize the bank's products (fiat-based money) to develop even better, albeit conceptually similar, products (e-money).

For those interested in delving deeper into this topic, I recommend the following articles by Luca Prosperi and Brett Scott:

Oh, I almost forgot one important point! The main reason why banks have all these beautiful properties is banking regulation - thousands of rules regarding liquidity requirements, usage of funds, information exchange, and so on. Moreover, banks’ obligations (including our deposits) are regulated and partly guaranteed within a legal framework that is supposed to provide a higher level of security and trust in banks compared to private companies. Thus, trust in digits on your smartphone, as well as trust in the formula 1 USD = 1 msUSD = 1 svbUSD, implies that you also trust the interconnected super-complex system of rules applicable to the banking system. In the last 20 years, we have witnessed some bank failures, raising the question: “Is our trust justified?”. However, we exhausted the “money as a product” perspective, let’s move further!

Money as an infrastructure

First of all, what is infrastructure? As a person who worked as a consultant in PPP projects (basically, infrastructure development), I can assure you that this question is inherently ambiguous, even in the context of tangible constructs. Extending this concept to the digital realm only amplifies its complexity. Yet, we can identify certain universally recognized infrastructural elements across various sectors

-

roads, all kinds of underground pipes, and transport systems stand out as quintessential examples of infrastructure;

-

data centers and cloud computing services are pivotal infrastructural components in the digital domain;

-

Ethereum, alternatives L1s, bridges, and some other protocols are other infrastructural “objects” in the digital domain.

Clearly, these systems need someone to manage them - pipelines require skilled operators, Ethereum relies on a network of nodes, and so forth. Thus, it is reasonable to define infrastructure by not only its "hardware" component (be it a tangible entity or a foundational set of rules and procedures codified) but also its "software" aspect (the personnel or nodes that ensure consistent operation, whether through centralized or decentralized mechanisms). Also, infrastructure is inherently designed to serve extensive groups of individuals or entire nations/economies.

Can we identify any isomorphisms between these systems and monetary systems? In other words, can the monetary system be considered a form of infrastructure, and if so, what are its fundamental components? To me, the existence of such isomorphisms is clear: just as stable systems for generating, transmitting, and storing energy form the backbone of energy infrastructure, stable systems for creating, moving, and safeguarding fiat or bank money make up the money infrastructure. In our existing money infrastructure, you could find analogous to the source of energy (government as the fiat money issuer), power plants (banks, transforming fiat money into end-user products), distribution networks (institutional framework and physical networks that facilitate financial transactions), transmission lines (SWIFT and other networks), and so on.

An interesting question is where to map banking regulations. What is the role of tens of thousands of supranational, national, and local rules adopted at various regulatory levels? In my opinion, these rules form the background for the operation of the monetary system - they act somewhere between the laws of physics and safety standards or operational protocols in the energy infrastructure, defining all possible ways of distribution and storage of money. Unlike the laws of physics, they are not static and can be changed by the agreement of the actors involved. Moreover, they exist in an archaic (almost paper) form, which leads to various interpretations in different situations - from their direct application to incorporation into national legislation.

So, from this perspective, cash in your pockets, digits in your smartphone app, and USDT in your Binance account will be an external manifestation of money, while the money itself would be complex interconnected systems of institutional and individual actors and layers of regulation underlying them.

The development of the M^0 protocol is grounded in the understanding that a good definition of money transcends its basic function as a payment mechanism, and encompasses the complex network of relationships and layers that extend the power of a foundational source of trust to the various instruments utilized daily by individuals and institutions.

What kind of money stablecoins are?

Firstly, it's important to recognize that there is no definitive "right" or "wrong" way to conceptualize money. The various contexts described previously are useful for different reasons. For instance, while the distinction between local community currencies and PayPal's digital money might seem negligible from a utilitarian standpoint, their difference becomes significantly clearer when you think about their underlying value sources.

To bring our discussion into a more tangible realm, let's consider one of the most prevalent offerings in the web3/crypto space: fiat-backed stablecoins. These tokens issued by entities such as Circle, Tether, and others essentially serve as products built upon the financial products offered by banks. Therefore, organizations like Circle and Tether can be seen as operating in the same sphere as PayPal, Venmo, and similar services. This is not to suggest that their offerings are inferior or obsolete - on the contrary, their versions of digital USD tend to be more accessible, functional, and censorship-resistant than many traditional fintech solutions. However, it is crucial to acknowledge that fiat-backed stablecoins are not aimed at overhauling the existing financial infrastructure or fundamentally transforming our monetary system. They’re not going to “fuck the banks”, so to speak.

One might argue, “I got it - fiat-backed stablecoins rely on the existing infrastructure with commercial banks as the key element of it, what is wrong here?”. Let’s get back to the energy infrastructure and imagine a region that has refused to update any components of its energy systems for over 50 years. This region maintains and repairs its existing systems but does not incorporate new techniques, materials, or technologies. Will this antiquated system continue to produce, transmit, and store energy? Certainly, it will. However, will it perform these functions as safely, quickly, and cost-effectively as it might with modern technologies and frameworks? Unlikely.

This analogy prompts a reflection on our current monetary system: might it be similarly outdated? How would we even recognize this? As in the paragraph above, we can juxtapose monetary systems with energy infrastructures. Here, bank failures and financial crises could be likened to power outages and temporary blackouts caused by obsolete energy systems. However, I’ll let Luca describe the problems caused by the use of outdated infrastructure in our monetary system while leaving it to the readers to draw parallels with other types of infrastructure.

Over time, however, the one-size-fits-all established system has begun to exhibit constraints across various dimensions:

Credit underwriting: with the emergence of structured and sophisticated credit, the capability of commercial banks to effectively assess and manage credit for anything beyond the most standard financing needs is questionable, as demonstrated by the inexorable rise of the shadow banking industry

Risk management: the intricacies of today’s financial markets pose significant challenges to managing counterparty risk effectively, often at the expense of the depositors, whose financial security depends on recurrent (yet discretionary) taxpayer-funded government bailouts

Distribution and storage: the necessity of relying on outdated legacy systems, for the distribution and maintenance of private depositors' ledgers is increasingly being questioned—the emergence of Central Bank Digital Currency (CBDC) projects and self-custody solutions are starting to challenge the need for traditional banking infrastructure

Returns: the ability of commercial banks to generate sufficient profits to reward their equity capital providers is under scrutiny, given the challenging macroeconomic environment and the burden of heavy regulatory buffers, as reflected in the depressed price-to-book market multiples for most banks

Technological integration: the incapacity of commercial banks to facilitate the necessary technological integrations in today's digital age, where commerce and data travel at different speeds and machines increasingly interact with other machines, is obvious

The undeniable importance of those limitations, unveiled during the global credit meltdown in the Great Financial Crisis of 2007-2009, and masked by fifteen years of zero-interest-rate policies, has reemerged in 2023 due to a sharp rise in interest rates. This shift has put a vast majority of regional financial institutions at risk, leading to multiple failures, notably including Silicon Valley Bank (SVB) as the most affected. Banking as we know it is fundamentally broken, signaling an imminent period of upheaval and reconstruction, and presenting the opportunity to reimagine and rebuild it anew.

M^0 Protocol’s big idea is not merely to introduce another money-like product (like USDC or USDT) but to fundamentally change the underlying infrastructure that supports these products and, more broadly, money itself. In other words, to say, “fuck you, banks, we don’t need your money,” and to democratize the ability to create money products for anyone possessing the requisite intellect and capital. Now it sounds much cooler than “another stablecoin,” huh?

Other designs for money

Ok, M^0 Protocol aims to establish itself as a Layer-0 for money, creating a basic, universal, and programmable unit of value that serves as the foundation for any form of money products built upon it. Are there other contenders seeking to revolutionize this space? For sure, there are! This is certainly not the first attempt to construct a “new foundation for money” from an infrastructural perspective, so let’s briefly review previous attempts, moving from the most decentralized initiatives to the most centralized

-

Bitcoin - even though BTC evangelists promote BTC as a new foundation of the modern monetary system, I tend to view BTC more as a form of digital gold or a countertrade object (more on this concept you can find here);

-

trust/credit networks, inspired by mutual credit systems, timebanks, and LETS - usually, in these networks, money emanates from mutual IOUs of members within the networks (for more information, check Ripple’s initial ideas, papers from Brett Scott or small projects like Union Finance or Trustlines Network);

-

CBDCs (retail CBDCs) - at this moment, CBDCs represent a shift in power from commercial banks to central banks, while the core ideas and concepts behind CBDCs address some existing issues within the current monetary systems discussed above, they also introduce new challenges (check here).

The M^0 Protocol's approach seems to straddle the line between trust networks and CBDCs. As in the concept of a global mutual credit system fueled by the ideas of new types of money issuers, the successful implementation of M^0 Labs’ ideas implies that we’ll see a whole new cohort of money issuers. At the same time, the source of value for money created within the global mutual credit system is the people and their promises (IOUs), while the M^0 Protocol is going to leverage trust in the USD issuer - government/fed.

So, what is M^0 Protocol about?

M^0 is leveraging trust in the USA and in USD but is not trying to replace it. M^0 is trying to replace banks and outdated regulation frameworks, but not the USD itself. In other words, M^0 is developing an infrastructure for money creation leveraging the ultimate source of trust, which is the USA with fiat USD, with $M (unit of value as convenient as digital money with the risk profile of physical cash) as one of the key elements of this infrastructure. The success of M^0 does not imply that we’ll use $M instead of USDT or USDC, but rather that the issuers of USDT and USDC (or any other e-money products) will leverage M^0 infrastructure to build their products on top of it.

I think now we’re ready to look into M^0 Protocol Whitepaper :)

So… what will be new infrastructure for money creation look like?

If you've delved into the economic analysis of large-scale infrastructure projects, you're likely aware that its value extends beyond the immediate benefits of the product or service it provides, encompassing broader, global impacts. Take, for example, a new train line connecting points A and B, which cuts travel time from 3 hours to 1.5 hours. This efficiency not only benefits daily commuters between A and B, saving them 3 hours each day (which is already impressive and cool), but it also represents significant advantages from the perspective of the state. These include reduced transportation costs, faster delivery of goods and materials, and alleviated pressure on surrounding infrastructure. Furthermore, such infrastructure projects contribute cumulative value to the national economy, which could be seen from analytical reviews but is never visible to an ordinary person whose 3 hours per day were saved by this new train line.

This analogy is applicable to the financial sector as well. In the context of the M^0 Protocol, the immediate benefit might be the introduction of a stable, low-risk cryptodollar $M (which is already impressive and cool). However, the broader, less visible impact of the protocol could be much more impressive. But before delving deeper, let's outline the basic structure of the protocol

-

M^0 protocol is a coordination tool (set of smart-contracts) for actors (actor = address) permissioned by governance: Minters, Validators, and Earners;

-

M is a standard ERC20 token, M^0 protocol goal is to ensure that all M in existence is backed by an equal or greater amount of value Eligible Collateral that is held in an Eligible Custody Solution;

-

Eligible Collateral - assets that can be placed in Eligible Custody Solutions and be used in the generation of M (currently, assets with the lowest risk - short-term US T-Bills), Eligible Custody Solution - a description of entity structures, jurisdictions, contractual agreements, and other details that will suffice for the custody of Eligible Collateral;

-

Minters are those who provide off-chain collateral and mint M, also they must provide information about collateral on-chain and periodically update on-chain numbers about off-chain collateral, potential Minters - financial services providers (such as cryptodollar issuers) off-chain;

-

Validators act as a security layer for protocol - they are entities that likely will have off-chain legal agreements with Minters and have full access to the records and statements of the Minters’ Eligible Custody Solution, they are in charge of checking Minters’ off-chain collateral and its on-chain value, also in some cases they can stop an errant generation of M, potential Validators - auditors off-chain;

-

Earners are able to control whether they earn the Earner Rate (the annualized percentage paid to M in the Earn Mechanism), potential Earners - institutional holders of M, issuers and distributors that maintain M inventory;

-

the description of economic incentives for the mentioned actors, including fees and other payments (“why would they want to use the protocol”) can be found here;

-

there are two utility tokens used in the M^0 Two Token Governor (TTG): POWER (is used to vote on active proposals, can be considered the primary management token) and ZERO (earned by POWER holders for their participation in governance, only vote on important changes), more on this here;

-

ZERO holders at any time may reset the POWER token supply to themselves - you can think about it as a mechanism to ensure credible neutrality of governance.

Those who are interested in more technical details can find them in the Whitepaper here.

What's interesting is that Whitepaper doesn't contain any overcomplicated diagrams or incomprehensible descriptions of the protocol's mechanics – everything is laid out in a simple and straightforward manner and might even seem somewhat naive to some. So one might ask, "Thousands of participants spent years developing Basel I/II/III and other regulations – are they suggesting that a 5-page document and a few thousand lines of code could replace all that?" My response would be - yes, it's possible!

The team has done an exemplary job in deconstructing the existing monetary system (more on DR research than in the Whitepaper itself) and identifying its fundamental properties. It appears that, although we could enumerate thousands of characteristics of the monetary system, only a handful are truly fundamental. Then what about others, non-fundamental, properties (including regulations)? I would argue that these are emergent, meaning they arise from the interactions among the foundational elements of the system (in the existing framework - central bank and commercial banks, in M^0 Protocol - central bank and TTG). This implies that there is zero sense in trying to replicate the emergent features of the legacy monetary system in a new framework with different participants. However, it's conceivable that the new system (TTG) might inadvertently develop features reminiscent of Basel III… though, hopefully, it will not.

So, to summarize, M^0 Protocol is a landscape

-

where key actors (Minters, Validators, Earners) are incentivized to create and maintain stabledollar $M;

-

where the coordination between governing bodies and protocol actors is set up in a balanced long-term sustained way;

-

where building products (like stablecoins) on top of M^0 is mutually beneficial for everyone involved;

-

where every actor within the protocol is performing what he is better suited to perform;

-

where the mentioned processes are based on smart contracts and automated (where it’s possible), so no one can break the rules, break or stop the protocol;

-

which is non-upgradeable and immutable in its core (so nobody can change its fundamentally credibly neutral architecture) and adaptable and mutable on the higher levels (so innovations can occur as fast as possible).

Then, what is the role of $M in this structure?

We refer to M as raw material for value representation, and not a cryptodollar in its own right, because the system relies on permissioned issuers (known as Minters in the protocol) for generation and distribution. These Minters should be compliant with all applicable regulations and may decide to distribute their own product, for example by wrapping the M token in a cryptodollar contract in a way that best meets their requirements. In this capacity, M becomes a monetary building block on top of which novel products can be built.

It’s probable that most end-users will never encounter $M in its pure form (as most of us rarely use cash). But what could be the use-cases for $M besides the obvious ones (fully backed xUSD or wrapped $M)? From my understanding, M^0 allows for the implementation of any financial engineering concept or real-world logic. For instance, we can create a virtual replica of Silicon Valley Bank, which would issue svbUSD - partly collateralized by $M, partly by credits with svbUSD minted “out from thin air” - and then svbUSD will lose its peg (but $M and trust in $M will be ok). Or we can set up 100 bank-like entities leveraging $M and then observe as POWER holders delve into the possibilities of fractional reserve $M minting and advocate for its implementation. Even more fascinating is the potential for the emergence of truly community-powered bank-like structures on top of M^0, where Minter represents the pool of crowdfunded tokenized T-Bills. But feel free to use your imagination :)

Closing thoughts

One of the characteristics of infrastructure projects is that their direct impact on the everyday lives of ordinary people is almost imperceptible. I have participated in the development of water supply networks, waste processing facilities, power lines, and many other projects, and in most cases, none of the end users noticed any difference in the quality of water, waste collection, or energy following the completion of these works. In the event of the M^0 Protocol's success, average users (including crypto-natives) are likely not to notice this achievement. At the same time, should the M^0 Protocol succeed, it is hoped that this success will indirectly advance the entire industry, setting a new standard for the security and reliability of stable digital assets.