At Bacon Protocol, we’re bridging the gap between DeFi and the mortgage market. We believe in the ethos of permissionless access, non-arbitrary, market-driven rates and we’re employing these DeFi-native concepts to innovate in the mortgage industry. One of these tools is our utilization of an Automated Market Maker (AMM) to decide both the interest rates borrowers will pay as well as the interest rates that bHOME holders will earn.

What is an AMM?

The Automated Market Maker (AMM) is a model popularized by decentralized exchanges (DEXs) like Uniswap as a more efficient replacement for traditional order matching and order book systems. AMMs are autonomous protocols that use smart contracts to define the price of digital assets. In AMMs, protocols pool their liquidity into smart contracts in order to create liquidity pools. These liquidity pools are replacements for the traditional buyer and seller markets that have required market makers to help create and solidify markets on centralized exchanges.

In an AMM, providing liquidity for trading pairs is automated by creating permissionless pools for specific pairs - for example ETH/USDC. This allows anyone to provide liquidity for the pool by depositing both of the assets represented in the pool. By using liquidity more efficiently, these pools are able to regulate the asset prices and reduce price volatility.

How does it work?

With no counterparties to execute trades and provide liquidity, AMMs rely on mathematical equations to eliminate discrepancies in the pricing of pooled assets. Uniswap innovated the original equation but since then many other DEXs have tweaked the design and created new relationships better suited to particular assets.

To best understand this, let's use an ETH/USDC liquidity pool example:

- When ETH is purchased, in order to remove ETH from the pool, USDC is added

- This causes the total amount of ETH in the pool to decrease, which causes the price of ETH in the pool to increase to maintain the balancing effect of x*y=k

- On the opposite side, more USDC has been added to the pool, causing the price of USDC to decrease

Where traditional market makers use order books to analyze and regulate prices, AMMs are algorithmically regulated, creating a more capital efficient trading system. More liquidity in a pool makes the pool less sensitive to larger swaps

Bring on the Bacon

This capital efficiency is why we envisioned implementing these concepts in other supply/demand-driven economies like the mortgage market. Bacon Protocol employs a similar AMM as the one above to decide which interest rates borrowers will pay and that bHOME holders will earn. This Bacon AMM creates a supply-demand curve that incentivizes borrowers and liquidity providers to increase participation in the protocol when needed.

The interest rate curve is set by the total amount of liquidity (USDC) in the Pan that can be lent out. When the Pan has excess liquidity, the AMM lowers the rate down the curve to incentivize borrowers to use the protocol to borrow USDC for loans. Similarly, when there is low liquidity in the Pan the AMM moves rates higher up the curve so that loans are made at higher interest rates to borrowers. The new higher interest rates create higher average rates for loans in the pan – which in turn creates higher returns for the pan’s liquidity providers. This encourages more liquidity to enter the protocol, ie. depositing more USDC in exchange for bHOME, which in turn brings the interest rates back down.

To summarize the balancing effect:

- If there is excess liquidity (lots of USDC), the interest rate lowers to incentivize borrowing.

- If there is low liquidity (small amounts of USDC), the interest rate increases to incentivize returns for liquidity providers.

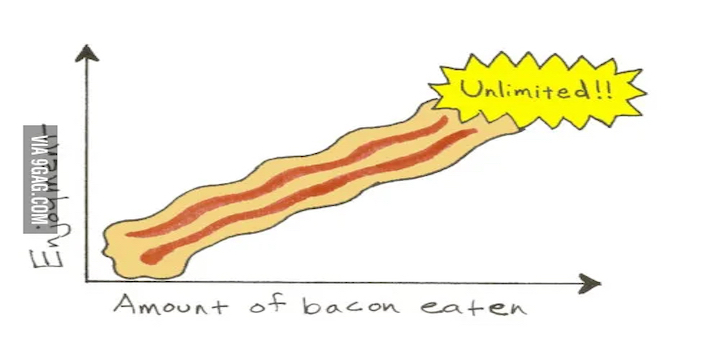

The AMM uses the following function to calculate the rate for a given loan:

- Utilization is the current percentage of the Pan that is lent out. (ie. if the pan has lent out 7.5M out of 10M USDC total, the utilization is 75)

- Base is the minimum interest rate (currently set at 2.0)

- k refers to how quickly rates increase as utilization increases and sets the slope of the demand curve (currently set to 150)

The chart above demonstrates the rate function of the AMM. At 0% utilization (ie. 0% of Pan is lent out), the loan interest rate is at 2%. This rate will stay relatively flat through low utilization levels. At 80% utilization, the interest rate is 4% (close to market rates for 30 year mortgages). At 90% utilization, the rate goes up to 6.5%. Anything above 90% utilization causes an exponential increase in interest rates to entice new liquidity to enter the protocol in order to decrease the pan utilization rate. Ideal utilization rates are below the 80-90% threshold so that bHOME holders have enough liquidity to easily move in and out of positions.

What’s great about the Bacon AMM?

AMMs are one of the most efficient and innovative ways to create equilibrium between supply and demand. They are a crucial piece of infrastructure in the journey from our old mortgage system into the new system we are building.

Some of the biggest advantages of using an AMM in Bacon include:

- Decentralization

- Liquidity is owned by the community rather than one entity such in traditional mortgage markets where access is gated to a small number of qualified investors

- Non-Custodial

- Investors now have sovereign control over investing in mortgages

- Security

- You can invest directly into the Bacon Protocol Pans rather than have your mortgage sold off to various institutions

- Accessibility

- Anyone with a wallet can invest in mortgages with Bacon Protocol

- Liquidity

- Liquid tokens are now available in the mortgage industry

The Bacon protocol’s AMM model continues to bridge the gap between TradFi and DeFi and is a key innovation in offering competitive interest rates for home mortgages while opening access to any investor with a crypto wallet. We hope you try it out for yourself and see how great it really is.

About Bacon Protocol

Bacon Protocol is a decentralized platform for purchasing mortgages. We give consumers access to the same financial products banks, governments, and institutions use to preserve and grow wealth. Using a novel, asset-backed stablecoin, we help homeowners by giving them faster, more flexible, and more competitive loans while adding a new building block to DeFi and bridging the gap between the physical and Web3 worlds.