If you’ve been paying attention to crypto Twitter the last few weeks, you’ve been able to watch how low/no fees drove incredibly high liquidity on Art Gobblers. This liquidity has benefited holders — they can exit immediately, and the floor stays elevated because the next buyer knows they can, too (it feels “less risky”).

Now that the NFT space has entered the post-fee world, the question is: how do we bring this level of liquidity to more collections?

One simple answer is: if you’re long an NFT collection, let others use it to short.

Why shorting

I’ll admit: it seems counterintuitive to let people short your NFT collection if you want it to increase in value. But, what if shorting unlocked the liquidity benefits available to collections like Art Gobblers, raised the floor price, and made selling easier? On top of that, what if you were earning money while helping people short?

It turns out that shorting is an essential part of market making, both for the spot (i.e., buying NFTs on a marketplace like OpenSea) and for derivatives (like call options on Hook). Market makers provide liquidity by making standing buy orders at the current price, purchasing those tokens, and then immediately listing higher. If you’ve ever received a 15-minute offer for immediate liquidity on Opensea with a strangely precise value, it’s probably a systematic market maker trying to provide instant liquidity.

Market makers face a significant risk: if the NFT price collapses while holding these positions, they’ll lose money. NFTs are super volatile, it’s challenging to build uncorrelated portfolios of them, and there are often only a few transactions a day in a collection, forcing market makers to carry this risk for a long time. The net result is that market makers can only provide instant liquidity at a deep discount to the most recent sale unless they have a way to protect their downside while they hold the position. Shorting lets market makers provide radically better pricing and liquidity for a collection. It also helps expand the horizons of derivatives markets.

How can we short NFTs?

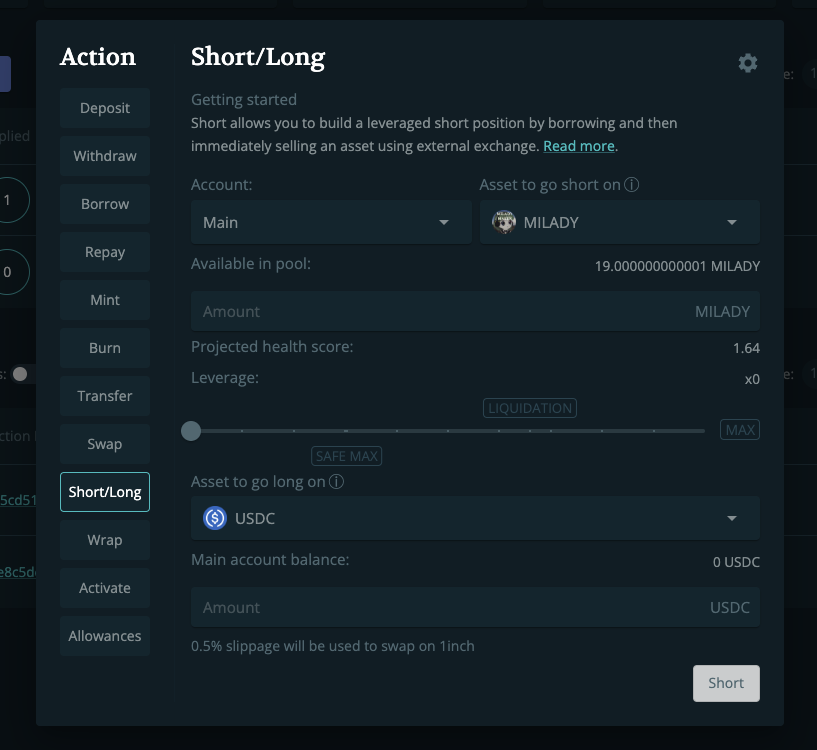

There is no shortage of exotic products to short — perps, put options, CDS — and many of these are coming to NFTs. But, the easiest way to start is to “sell short” by borrowing an NFT and selling it. Because you owe the NFT back to the lender, every time that asset increases in value by a dollar you lose a dollar, and vice versa when it decreases.

Today, you can borrow in two ways. If you’re a major market maker with a big balance sheet, you can sign an off-chain contract with a counterparty — for example, a collection — and borrow a bunch of NFTs from them. If the market maker doesn’t give back the NFT, the collection can sue them in court because there’s an entity to sue. This isn’t very crypto-native.

FloorDAO has innovated in another category…staking NFTs in NFTX vaults, and depositing the resultant ERC-20s into Euler. Anyone can then borrow the ERC-20s, each redeemable for a floor NFT from the collection, and then sell them. FloorDAO gets paid while people do this, and the liquidation mechanism built into Euler makes it low-risk.

Check out this post from Lambert Guillaume on how traders also utilize Euler shorts to hedge options.

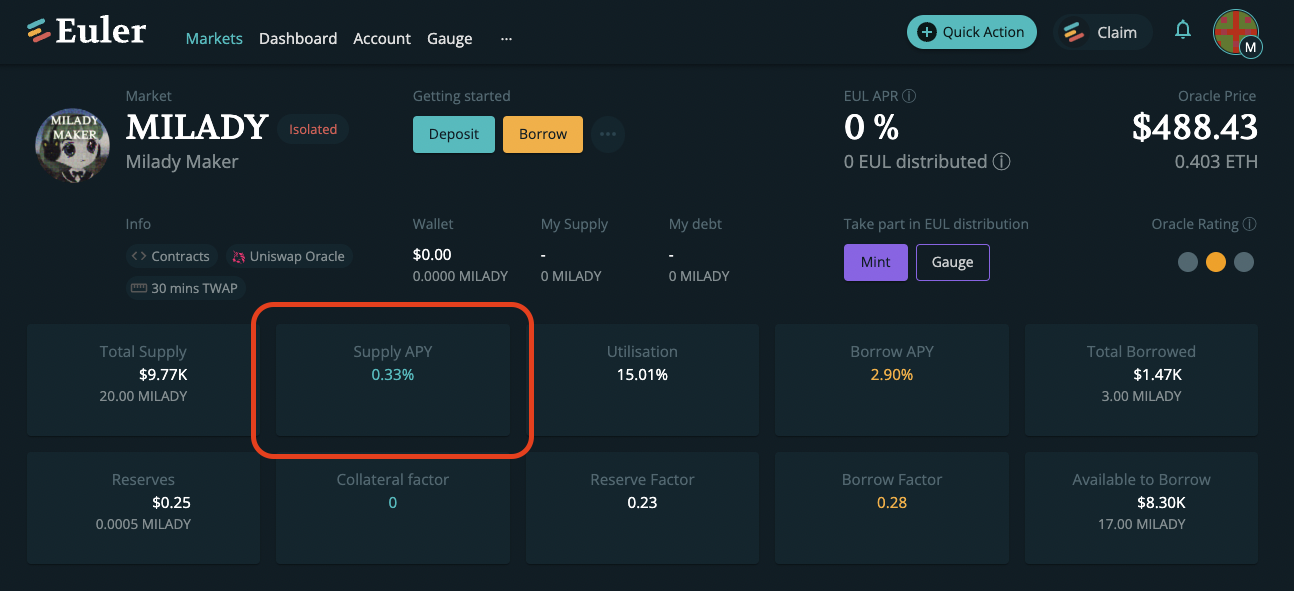

There are currently $36m in NFTs deposited into NFTX. Today, NFTX tokens representing only 20 Miladys and 1 Punk have been deposited into Euler. If a higher % of those were available to short, market makers would have much more liquidity available.

At the end of the day, holding inventory available to short on Euler is much more crypto-native than having market makers work out exclusive side deals with projects — the liquidity is available to everyone, and can happen on-chain. In order to make this possible, we need to reach a tipping point of supply. Everyone should deposit their NFTs into Euler. The number of available collections today is not interesting/expansive enough to build real trading strategies.

For crypto-natives who don’t want to manually do this, deposit money into FloorDAO. You’ll end up long a “basket” of NFTs, and the team inside the DAO manages positions like these for you.

Short NFTs & call options on Hook

Derivatives, like options, are another tool that is more liquid if short positions are available. They allow active traders to construct more complex positions, and in some cases, spend less money to get a position with a similar upside (and greater risk).

Hook’s call options are a specific variant of a European-style option - a trader buys the option from a writer with an agreed-upon strike price, expiration, and underlying NFT. If that NFT sells for more than the strike price on the expiration date, the option holder receives the excess of the selling price above the strike. If it does not, they get nothing and the option is worthless.

Traders love options because it’s a better, more capital-efficient way to get long exposure on an NFT. Traders can make much more money on their best trades by purchasing options instead of the spot asset. Sophisticated individual traders, who are often the most capital constrained, benefit here.

On the other hand, a market maker looking to make options available faces significant risk. They must deposit the NFT into the options contract for the whole duration — potentially a month or more — and lose the ability to sell that asset. If the collection price crashes, there is nothing the trader can do to limit their losses unless the option holder cooperates. To make this work, the option writer must decide how much to short.

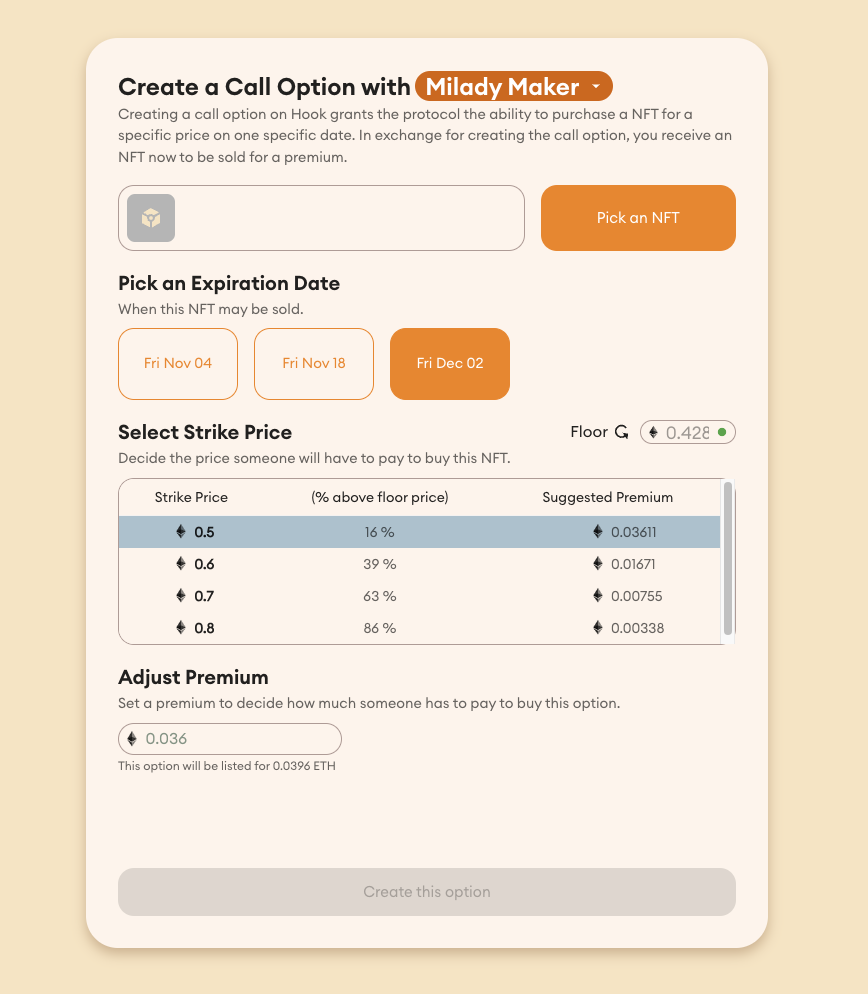

Consider an option writer selling an option on 1 Milady, with a current value of 0.42 ETH. They may want to sell an approximately 20% out-of-the-money option with a strike price of 0.5 ETH. If the writer believes the annualized volatility of a floor Milady is currently 120%, then the Black-Scholes value of the option is about 0.036 ETH.

Black-Scholes also tells us several important things about the value of that option beyond the current price. Several partial derivatives of the formula - colloquially referred to as the greeks - reveal how the value of the option changes as the inputs change. The option’s delta is one of the most interesting greeks because it measures how much the option’s value changes due to the spot price changing. The delta tells us how much more wei the option is worth for every wei the value of the underlying Milady changes. In the case of this option, the delta is about 0.37.

Once the trader sells this option (and banks their 0.036 ETH premium), they need to delta-hedge to ensure they’re covered if the Milady's value decreases. The trader is long 1 milady (deposited in the vault) and has sold an option with 0.37 delta. Because they sold the option (subtracted it from their portfolio), they should subtract the position's delta. Their delta is currently 1 - 0.37 = 0.63. Using Euler, the writer should short that much Milady.

Ideally, the trader will create many of these options, each with a different delta, and come up with a total portfolio delta. They should occasionally “re-hedge”, meaning re-compute their total delta and resize their short position to match.

The details behind “delta hedging” are the trickiest part of this strategy – delta changes with factors like the asset price, strike price, and time elapsed. Most traders likely won’t short 0.63 and will optimize to complete fewer (costly) transactions on-chain. One simple way to hedge is to short 1 milady when the milady price is below the strike price, and cover that short when it passes the strike. This approach is less accurate but is simpler to implement.

These shorts are currently available at 2% annual interest, meaning that throughout the 1-month option, the writer would owe about 0.1% of Milady — about $2 USD. The gas costs to enter the trade, and appropriately re-hedge would be much greater. Currently, gas is pretty cheap, so we estimate that at $40. The option writer makes 0.04 ETH in premium — about $64 today, meaning they’re pocketing about $22.

The writer can also continuously make offers to the holder - giving them exit liquidity to close their position early if they’d prefer.

This trade is also great for everyone else: the Milady lender (currently, FloorDAO), earns yield on their staked Milady. The option buyer gets convex upside exposure and can possibly profit if the Milady moons. And of course, the option writer profits significantly for their efforts, all while taking much less risk than just selling the option.

Shorting helps everyone

Shorting has a bad reputation in NFTs because no one wants to bet against their favorite collection. This criticism misses the point. In practice, holders and creators want traders to be able to short because small short positions create the opportunity for significantly more liquidity in the market. Entering these positions is relatively complicated, and only the number of lent tokens can be shorted, which limits the market impact. By opening up these positions, a small number of traders can create a positive market change for everyone else.

Thanks to @1A1zP1, @NiftyFiftyETH, @justinavery, @aeto, @brianman1, @notrickfox for reviewing this before publishing!