Real estate is one of the largest asset classes worldwide in terms of market capitalization, however, real estate ownership is not open to all members of society. Many low-income households can never afford to buy real estate. To receive a loan, buyers must have a positive credit score, a steady and well-paid job, or a collateral of other assets.

This article covers the following topics:

- Problems with Real Property

- What can one do with real-estate?

- A peek into the different actors in the ecosystem

- Real Estate & the Blockchain use case

- Challenges & the Way Forward for Home DAO

- Pictorial representation of Home DAO’s features & tokens utility

- Objective

1. Problems with Real Property

A major problem with the Real estate market today is that all the relevant information is scarce or abstracted away even in this information age. This along with outdated ways of handling information by the government and Central authorities, many a times seen in physical registers and cupboards has hampered innovation and created a great void for the end users in this area. Lot of intermediaries and brokers have stepped up to fill this void and have taken a cut of the pie form the rightful owners in each and every property trade happening in the world. Paying up or compensating these intermediaries or brokers to get help and access to relevant real estate information has become a norm.

Even after having access to right information, potential home buyers, sellers or investors have to go through a chain of brokers to make the decisions of their own choice. Since this market is very regulated, this chain of brokers also include central authorities including notaries and banks for fulfilment. This often results is excess kyc, aml and cascading fees raising the bar for such trades unnecessarily high. The Central Authorities like notaries maintaining the Property registers also charge a huge percentage of the trade. Moreover for financing needs, one has to pay not only interest rates to the bank, but also high fees for administering the loans.

It is ridiculous that about more than 10% of the value of the trade is often lost, each time a real estate transaction takes place benefitting everyone in the middle except the real concerned buying and selling end users or investors. The more the number of middleman, the more expensive and in-efficient a trade becomes.

These problems need a greater reform across nation states in the world. The following problems are very obvious:

- Un-informed decisions by buyers, sellers & investors due to lack of transparency and information.

- Expensive & Inefficient trades due to a chain of brokers which also includes government bodies.

- Very slow and cumbersome process driven by banks, Property Registrars or Notaries.

- A very high entry barrier for investing in real estate markets. This has apparently become an investment tool only for huge institutions and the super rich.

- **Very limited access to international investors & property markets **due to very strict, complex & different financial and security regulations across different nation states.

The existing conventional currencies, monetary policies, innovation and the blockchain solutions still suffer a number of issues which are not limited to the following:

- “the impossible trinity” i.e. the trade-off between (i) autonomous monetary policy, (ii) exchange rate stability, and (iii) capital mobility.

- **Fungibility vs privacy **for asset backed tokens.

- **Tangible Intrinsic value **in some cases, however greater adoption usually minimises this socio-economic and ethical concern.

- No pre-specified socially optimal “lender-of-last resort” rules in a smart contract. Lender-of-last resort refers to a safety-net institution, usually provided by central banks, to reduce the risk of a lack of liquidity of financial systems as a result of financial panics and bank runs.

- Still very high entry barriers and lotteries to get in for a select richer few.

- **Centrally Governed & Central points of failure **specially when off-chain data is required and oracles are needed.

2. What can one do with real-estate?

The real estate life cycle begins with procuring land or property and then building and improvements. It is registered for the first time by a governing Central Authority and then the ownership keeps transferring. Real estate can be Residential, Commercial, Industrial, Land, One may choose to do any or more of the following:

- Buy to live or invest in it

- Sell to raise money or change homes

- Lease to raise money from it

- Put it in the Will for inheritance

- Charity or gift it

All of the above basically requires a transaction of sorts at the end of the day with conditions or contracts which may be special to the scenario. These transactions in turn need brokers, lawyers and Central authorities with outdated technologies which make them cumbersome and slow.

This results in multifold costs which is proportional to the number of intermediaries in between as everyone needs a cut.* *The illiquid nature completely limits & cripples the potential of real estate and any innovation in this area, making them non-bankable. One classic example of a complete waste of money and other resources is where a property is rendered economically useless for a long time, each time a generation changes because a property needs to be divided according to an inheritance law or a will. Today no practical way exists to accomplish this efficiently, often resulting into years of legal battles. After a long wait, funds are distributed to the inheritors by auctioning the real-estate. All these inefficiencies result in waste of money and time over the years for people involved in it.

3. A peek into the different actors in the ecosystem

- Bob owns a real estate with a loan from the bank. Bob needs to payback the loan i.e. the principal, interest and fees to the bank

- Bob owns real-estate without any active loans from the bank. Bob has no instant need for any paybacks but lives in the same home and needs to raise money.

- Bob needs a new home for his family to live in by applying for a bank loan. Bob needs a first time new home.

- Bob wants to sell his home to move into a new home. Bob needs a different home.

- Bob wants to sell his home to raise money. Bob needs money.

- Bob wants to invest small or large amounts of money in the real estate market. Bob has investment needs.

- Bob wants to invest in the foreign real estate market as that will do much better than his own country. Bob has investment needs.

- Bob wants to setup inheritance & other ownership rights to his property. Bob has complex contactual needs.

- Bob is broker or real estate agent. Bob is basically a middleman.

- Central notary.

- Govt Registry. A Central authority registrar.

4. Real Estate & the Blockchain use case

A real estate property is an immovable asset, registered on a Central register. The property is transferred from one owner to the other through a registry which is maintained by a central authority. This is similar to owning assets on a blockchain where ownership rights are transferred on chain through cryptography without actually moving the assets. The obvious difference is the Central authority. This makes the blockchain a text book case to be used for this to be transparent, secure, easy and most importantly efficient in terms of money and time eliminating most “just for a cut” middleman.

Home is one of the most basic needs of mankind. Having a place to live is one of the most essential things in life. You need food and water to survive, you need clothes to be dressed modestly and you need a home to have a roof on top of your heads, be it as a tenant or an owner. Food and clothes are still relatively easy to procure and use as they are something you can quickly transact, move and resell or even re-share if you have to give out to charity. The complexity lies with the real estate or a physical place to live in. You cannot carry a real-estate home on your shoulders. Your ownership is maintained through a proof of some document which points to a record on the Central registry. A transaction does not result in one taking the home from one place to another, rather it simply is a change on ownership on an address where you have signed.

“Asset tokens are to financial markets what social media was to the publishing industry” — Voshmgir, Shermin

Blockchain is the textbook use case for evolution and a solution to this where change in ownership is decentralised on the chain, secured by cryptography. One of the main difference with the traditional legacy systems is that blockchain registry would be decentralised, hence making it transparent, efficient and saving so much money & other resources.

5. Challenges & the Way Forward for Home DAO

In order for pave the way forward for the future to have an open trade culture of buying, selling and investing in real-estate, one of the most important hurdles to overcome is the plethora of non-digital & non-decentralised records of ownership of real estate. More and more real estate properties need to be tokenised until it becomes a norm.

Driving tokenisation of real-estate is essential for adoption.

The legal aspect of the challenge may be solved if we are able to retrospectively and in parallel maintain all the Central Authority registers and regulations till we reach adoption threshold. A better way to overcome this may be by digitalising the property using special investment vehicles which other players in the area have tried successfully.

Many countries are already looking into registering land titles on some kind of distributed ledger, and many more are following. A fast-growing ecosystem of service providers offering fractional ownership solutions and other tokenized real estate services is evolving, such as “Atlant,” “IHT Real Estate Protocol,” “LATOKEN,” “Max Property Group,” “Meridio,” “BitRent,” “Etherty,” “Caviar,” “Propy,” “PropertyShare,” “Rentberry,” “Treehouse,” or “Trust.”

Home DAO plans to overcome these challenge by starting & not limiting to do the following :

- Providing incentives to Tokenise real estate. Home DAO plans to provide a framework for it. This may apply to 100% of the properties in the world and targets all people who own any property in the world.

- Make all the transactions of transfer of property simple, efficient and cost-effective by removing all unnecessary middleman. Most people in this world are living in one form of the property or another and at some point in life need to make a transaction for themselves or their family.

- Provide easy real estate investment opportunities by launching country specific home tokens backed by real estate investments.

Other Incentives for owners tokenising the real-estate:

- Upfront & free instant cash benefits.

- Bankability of your real estate gives you all the future benefits and new market opportunities related to trades, loans, security, configuration, no selling costs, notary brokerage 8% costs when you sell or write a will.

Other Incentives for Investors:

- Investors will get a certain percentage of the NFT shares of the properties they finance for tokenisation.

- Investors will also get free Home tokens at face value with respect to the real estate’s country.

- Will have the ability to invest/trade in any real estate market of any nation state in the world. This will be enabled be a novelle real estate token model.

Other Incentives for Sellers:

- Sellers will avoid all the administration & notary fees etc

- Sellers will get an opportunity to freely use the tokenised property platform exposing them to many different kinds from investors from around the world. This may be enabled by provided free home tokens as incentives to first time sellers using the Home DAO’s platform. (Home DAO tokens may be needed to be staked to use the platform)

In principal home DAO’s goal is to :

- Disrupt Real estate transactions

- *Disrupt Real estate investment needs & the process itself around the world by making it as simple as a DEX transaction or a FOREX transaction, by leveraging country specific home tokens backed by real estate and other bag of assets.This may be supported by “proof of provenance” as successfully established by DIGIX for gold backed stable coins. *https://digix.global/whitepaper.pdf#/

High Level Perspective

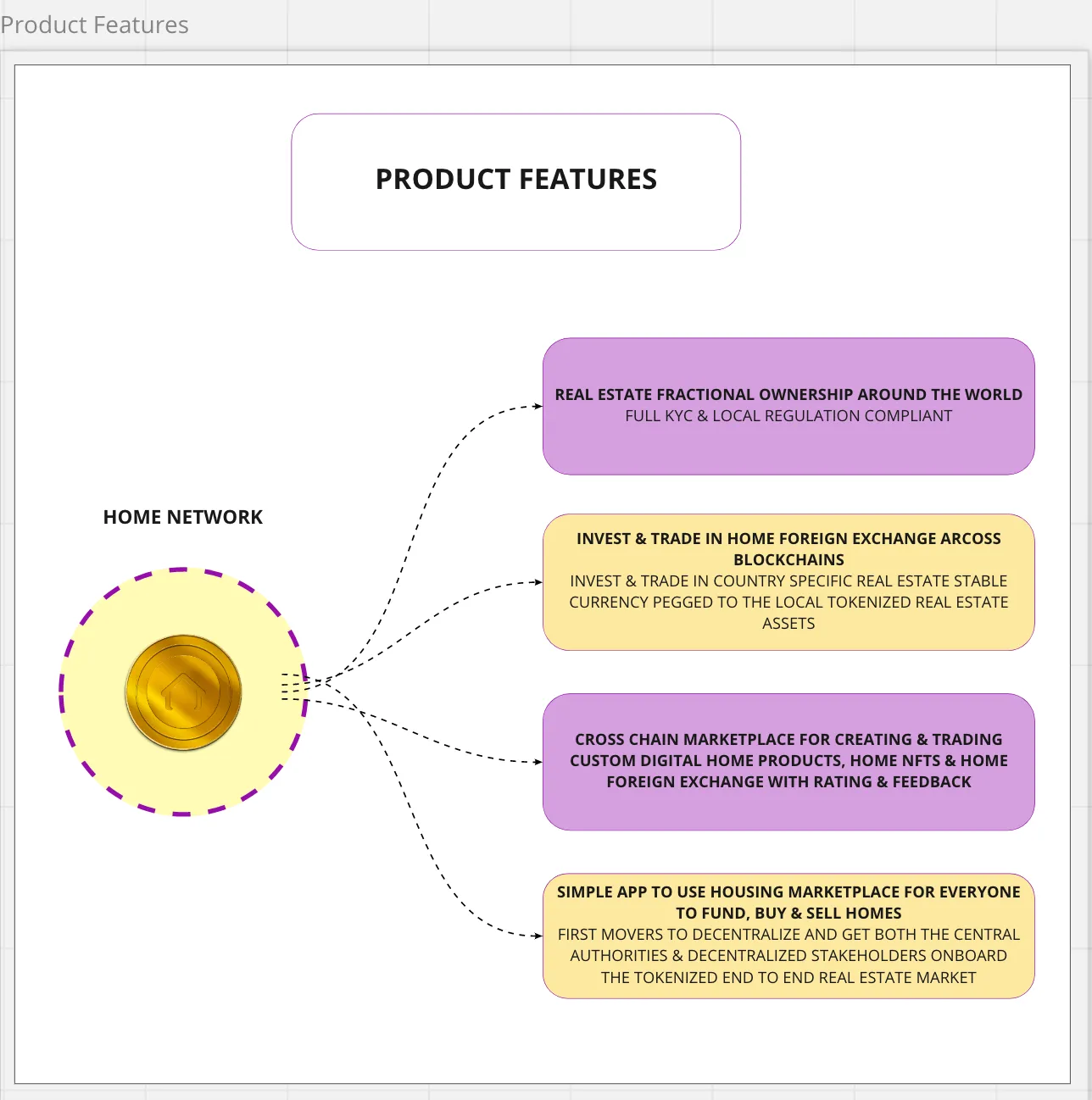

6. Pictorial representation of Home DAO’s features & tokens utility

Home DAO Product Features

Home DAO Token utility

7. Objective

Real estate transactions need to be efficient, painless and simple. It should be as easy as enabling a digital payment from one wallet to another based on if certain legal and contractual conditions are met. Solving these basic issues will create endless opportunities in the real estate market and ease for the general population and the economy.

The investment opportunities, services and products which could spawn out of innovation in this space by making real estate market bankable and easy to avail is only limited by our imagination

The objective of Home DAO’s initiative is to make things simple for us all collectively when it comes to one of the most basic needs of humankind, besides having food and clothing i.e. having a roof on your head or a home for your family. This is specially possible at such a time when public awareness and adoption is rising rapidly and people are in a situation to make more responsible and conscious decisions.

This initiative aims to solve the inherent problems of real estate un-bankability by leveraging the open blockchain technology, web3 token economy and NFTs to not only just tokenise real-estate, but also collectively make evolutionary changes to transactions related to real-estate by making them transparent, secure, cheaper, highly efficient and configurable.

Furthermore configurable contracts and transactions open the doors to empower people to setup special contracts and conditions needed for societies of today. Some simple examples can be next generation investment products, ethical crowd financing, divisions, unions, wills & inheritance, gifts etc.

It is a collective socio-economic journey and the future looks brighter.