Frax is a unique stablecoin project, that has released the FRAX and Frax Price Index (FPI) stablecoin and aims to be a decentralized alternative to centralized counterparts such as USDC and USDT. Its uniqueness comes from using fractional collateralization in order to back one unit of the token. In order to ensure deep liquidity, organic adoption, capital efficiency and longevity the team has built a suite of products such as FraxFerry, FraxSwap and FraxLend.

Frax was launched on the Ethereum mainnet in December 2020 after being announced in May 2019. Within an hour of launch, the project attracted a TVL of $43M. It was founded by Sam Kazemian, Travis Moore and Jason Huan who all attended the University of California. Travis serves as the Chief Technology Officer. He previously worked at Anthem as a Senior Business Information Analyst and graduated with a Bachelor of Science in Biochemistry, Neuroscience and Cellular & Molecular Biology. Jason More founded the Blockchain Club at UCLA and was a course instructor at the same institution before co-founding Frax Finance. Sam double majored in philosophy and neuroscience. Together with Theodor, he founded Everipedia which was a wiki-based online encyclopedia.

In this piece we will look into:

-

Fundamentals: FRAX, FPI, FraxFerry, FraxLend & FraxSwap

-

Tokenomics

-

Competitor Analysis

-

Coming Catalysts and Risks

Fundamentals

FRAX

Frax is a stablecoin protocol that contains two main products; FRAX and FPI (Frax Price Index). FRAX is a fractional algorithmic stablecoin that is pegged to the US dollar, meaning it can be minted using an exogenous asset (USDC) and an endogenous asset (FXS) that will be burned. Frax Shares (FXS) is the non-stable governance token for the protocol. Holders of FXS are able to earn a share of protocol fees.

The price stability of FRAX is kept in check through a minting and redeeming process. In order to mint $1 of FRAX a user needs to deposit assets through a protocol-maintained collateral ratio. The collateral ratio is set by the protocol during times of FRAX expansion and contraction. In the contraction phase, the collateral ratio increases to ensure that market confidence in the stablecoin is increased.

If the collateral ratio is at 100%, then an asset's value that is deposited is used to mint $1 of FRAX. In an instant where the protocol is in a fractionalized state, then FXS is used to top up the value that goes into the protocol to mint the stablecoin. The stablecoin’s stability mechanism is powered by Algorithmic Market Operations (AMOs) controller. In Frax v2, other AMOs which help Frax manage liquidity efficiently while generating revenue was created:

-

Lending AMO: it lends out FRAX to DeFi lending protocols.

-

Liquidity AMO: deploys FRAX into liquidity pools to earn swap fees.

-

Curve AMO: deploys FRAX and USDC into Curve liquidity in order to increase the protocol’s protocol-owned liquidity.

-

Investor AMO: idle FRAX is deposited to yearn yield in protocols like Compound and Aave.

In a scenario where the collateral ratio is 95%, $0.95 of the collateral is utilized while the remaining $0.04 of value consists of burned FXS. The price stability system presents an opportunity for arbitrageurs in case the market value of FRAX goes below $1. They will buy it from the open market and redeem it for $1 of value from the protocol. The collateralization ratio is set using the Proportional-Integral-Derivative(PID) Controller which incentivizes arbitrageurs to maintain the FRAX peg.

Frax Price Index (FPI)

This is a stablecoin that is linked to the US Consumer Price Index (CPI). This is the first stablecoin that is pegged to a basket of real-world consumer items. The system is governed by Frax Price Index Share (FPIS) token. A Chainlink oracle is used to commit the 12-month inflation rate that is reported by the US government on-chain. The redemption price of FPI grows or decreases with the reported inflation rate and the peg calculation rate is updated in line with the monthly CPI data. This initiative to launch FPI may be used to gauge if a protocol’s value accrual is growing in step with inflation. FPI is different from FRAX since it uses 100% collateral ratio.

The protocol has launched products such as Fraxlend, FraxSwap and FraxFerry that have created a flywheel in order to deepen the liquidity of its stablecoin and ensure ecosystem growth. They have enabled the protocol to be more hands-on in their monetary policy affairs, unlike other stablecoin projects.

FraxFerry

This is a bridge that is used to transfer Frax tokens to other chains. The motivation behind this launch was due to the numerous bridge hacks that have occurred and cost users over $2B.

The benefits of using FraxFerry:

-

Infinite mints cannot occur as risk is capped by token amounts in bridge contracts

-

Bad batches can be caught and stopped as slower transactions have been implemented.

Some risks of the bridge include:

-

Any reorg from the source chain.

-

Optimistic rollups conducting rollbacks

-

Centralization of the bridge mechanics.

FraxSwap

Innovation and pushing the boundaries in DeFi is nothing new to Frax as it went ahead and built Fraxswap. This is the first constant-product automated market maker with an embedded time-weighted average market maker (TWAMM) enabling large trades to be conducted over long periods of time in a trustless manner. It is based on Uniswap V2 constant product pools.

The TWAMM implementation is a more gas-efficient way for minimal slippage trades. Other protocols may leverage FraxSwap in either selling or buying governance tokens and conducting token swaps between DAOs.

FraxLend

This product allows the protocol to lend FRAX as users deposit one type of crypto to borrow another. During its launch, Fraxlend supported two types of rate calculators namely; TIme-Weighted Variable Rate Calculator and Linear Rate Calculator. From Frax Finance docs, we can tell the difference between the two as the former calculates interest rates based on the amount of assets borrowed while the latter calculates interest rates purely as a function of utilization.

Frax Ether

Ahead of withdrawals being ready, liquid staking derivatives(LSDs) has become the talk of the town. Frax entered this foray by launching Frax Ether which contains frxETH(Frax Ether) and sfrxETH (Staked Frax Ether).

frxETH: an Ethereum-pegged stablecoin that aims at replacing wrapped ETH. When 1 ETH is deposited into the protocol 0.9 goes to spin up validators while 0.1 goes to the Curve pool for peg liquidity purposes.

sfrxETH: this is the interest-bearing version of staked frxETH.

Through this initiative, Frax is able to bring ETH into its own ecosystem while growing its revenue-earning opportunities. Who knows? Maybe frxETH may be used as an endogenous asset backing FRAX. According to Sam, frxETH captures the market demand for spot ETH which is something rETH or stETH haven’t been able to do.

Liquid staking abstracts the complexities of running a validator and meeting the minimum requirement of 32 ETH. This assists as many small ETH holders to participate in securing the network while earning yield. The protocol takes a 10% fee from the yield earned on Frax while 80% of the fees go to FXS stakers.

Protocol Metrics

Frax protocol has released fee-generating products with healthy balance sheets and TVLs. FraxLend has $234M in TVL with a total supply value of $63M.The product has a pair count of 16 with 573 users.

Since inception, the five AMOs have earned Frax Finance a total of $43M in accrued profit. Frax currently has the 4th largest pool on Curve with a TVL of $453M while the FraxBP has $751M in TVL. It uses the Curve emissions that it earns to incentivize more LPs leading to deeper liquidity for the stablecoin.

frxETH has grown to a TVL of $141M and a total supply of 95,025 frxETH. Currently, the reserves stand at 53% of the Curve pool with a 7.72% APR. The active validators have reached 2,240 in number earning an average of 11 ETH/day. frxETH related balance sheet stands at +60 ETH (~$90,000).

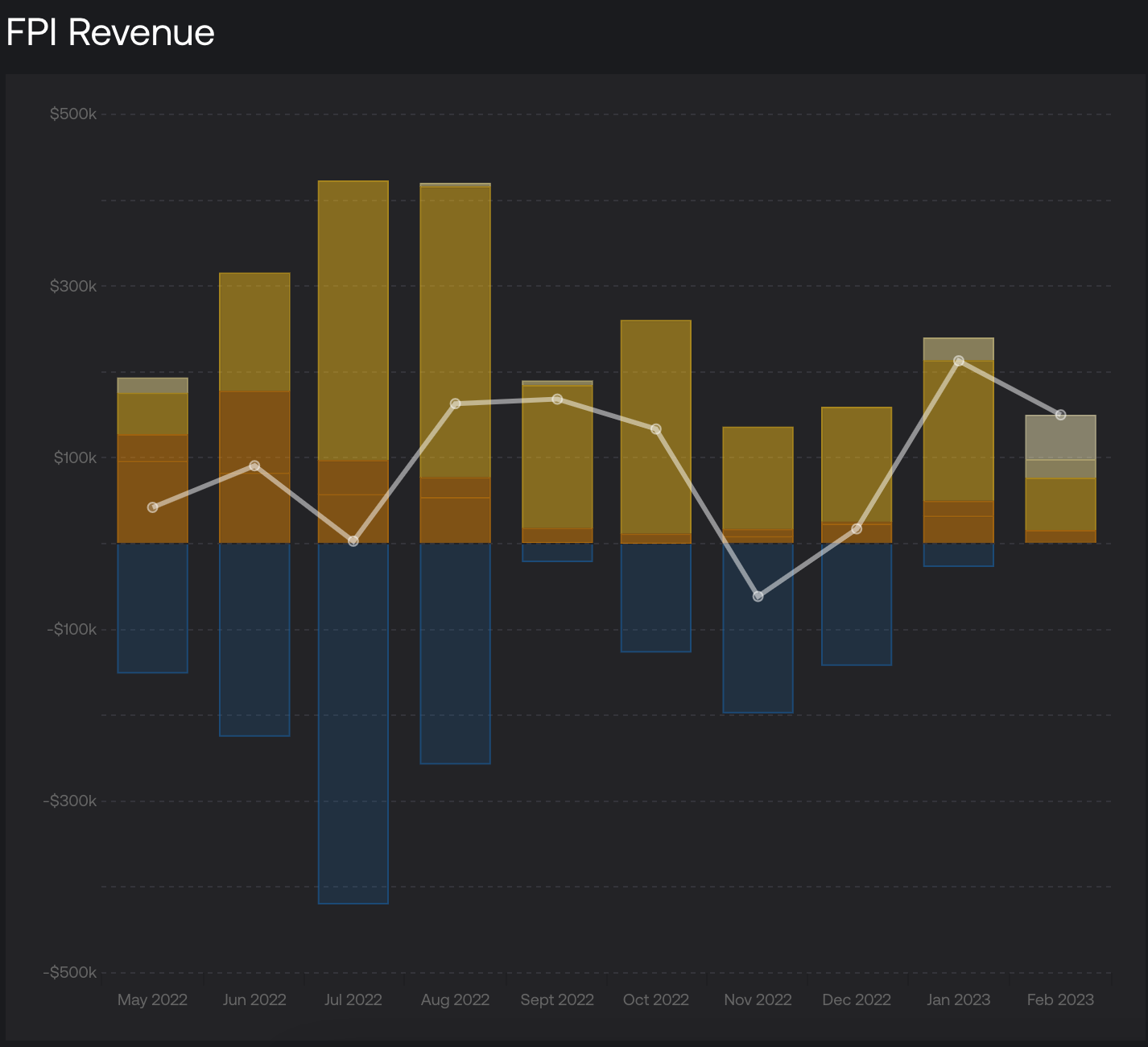

Except for the month of November, FPI has been posting profits with the highest income being recorded in January 2023 earning the protocol profit of slightly over $200,000. It has a healthy balance sheet of $4.5M with the FPI/FRAX pair on Curve having an APR of 3.48%.

Token Economy

Competitor analysis

In the analysis above, DAI is the only decentralized stablecoin. Others like FEI and RAI are also in the same category as FRAX. With this categorization in mind, FEI faced a hack in 2022 which set back investor confidence. RAI, an ETH-only backed non-US pegged stablecoin hasn't been able to catch the eye of the masses.

***Biggest catalysts in coming months***

BAMM launch: In one of the latest episodes of Empire by Blockworks, Sam alluded to working on a BAMM, a borrow AMM, with the aim of building a platform that will have spot liquidity and users can borrow without using an oracle. This will enable stablecoins in Frax’s ecosystem to capture the longtail market. Much hasn’t been said about this but be on the lookout for it this year.

Governance diversification: Although the protocol is governed by veFXS holders, decisions made are only executed by a 3 of 5 multisig which consists of the co-founders and Jason Moore. This is a huge centralization risk for a stablecoin protocol since community members have to assume that the multisig will act in a manner that is most beneficial to the protocol. In order to address this, the project is working on a new 6 of 11 multisig. The implementation of this design is that 6 of the signers are smart contract signers that function as one and are controlled by veFXS holders while the rest will be human. In order for governance to be effected the requirement is that a minimum of 6 signers will be involved. This means that the core team cannot execute any governance transactions. This new governance module brings about trust minimization, therefore, decentralizing the project further.

The success of the Shanghai hard fork: We briefly spoke about the launch of liquid staking through frxETH and sfrxETH. One of the potential biggest liquidity drivers for the protocol will be when the Shanghai hard fork will be successfully implemented. Already Frax contains the fastest-growing liquid staking derivatives. A successful hard fork will increase market confidence in the protocol hence growing its userbase and liquidity. Sam has spoken about taking in more exogenous collateral moving forward. I suspect this may lead the protocol’s stablecoin to have exposure to ETH through frxETH.

Federal Reserve master account: The protocol is currently interested in applying for a Fed master account which will enable it to offer risk-free returns to holders of its stablecoin. If this attempt is successful it will drive a huge amount of capital into the protocol. Frax will be able to generate more fees from this endeavor.

Biggest risks in coming months**

Competition: Curve and Aave are launching their own stablecoins,crvUSD and GHO. This may reduce the market capitalization for FRAX since both protocols have established deep moats within their sectors (Stablecoin AMM and lending respectively). CurveDAO may be incentivized to direct emissions toward their own pool though Frax protocol holds 32% of the total gauge weight vote. Frax is responsible for 50% of the amount bribed to CVX lockers. The launch of crvUSD may reduce the revenue earned by FraxBP and Frax3crv pools which generate the 5th and 6th most revenue of all Curve pools. From this risk assessment by Blockworks, Curve may reduce its exposure to Frax since it holds 21% of assets on Curve.

Regulation: The usage of USDC as collateral in the protocol brings about regulation exposure risks. With the current DeFi crackdown we’re witnessing, centralized stablecoin issuers may face legal enforcement pressure to reduce their exposure to DeFi. Undercollateralization of FRAX may happen when such a policy is thoroughly enforced and a bank run is inevitable.